yahoo Press

Technical tidal wave drives European loan spreads to nine-year tights

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

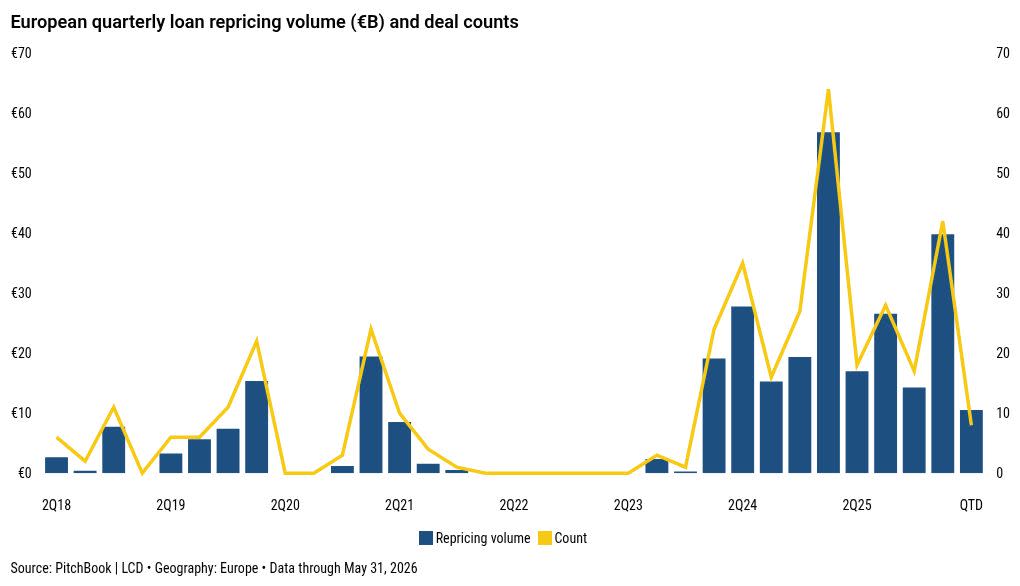

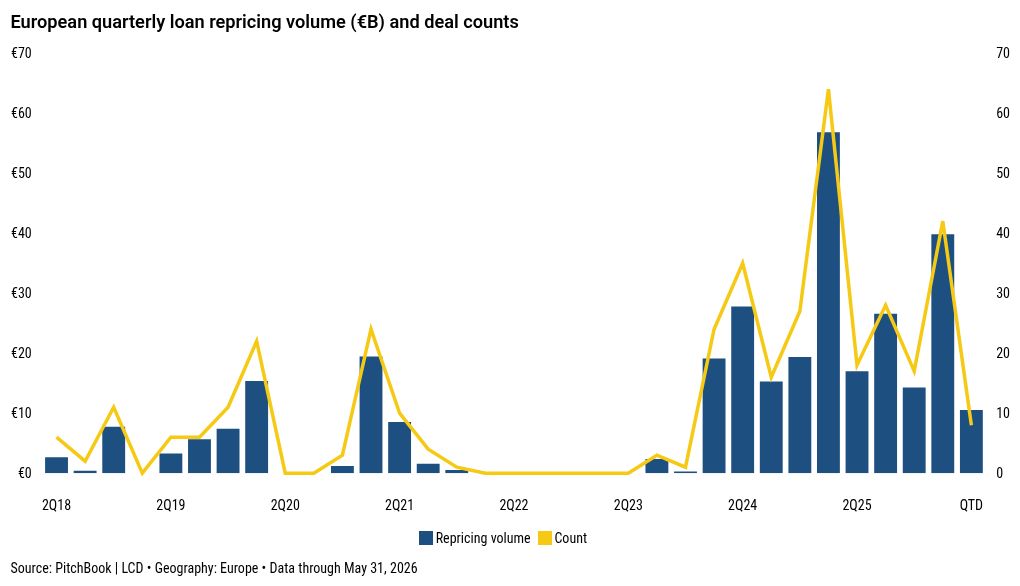

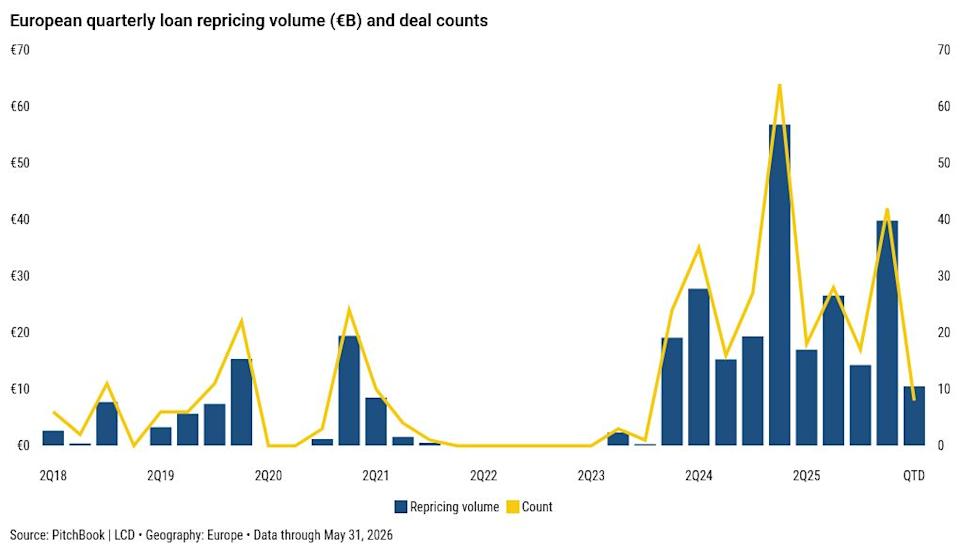

European loan spreads have hit their tightest levels since 2017 as record CLO demand has outpaced supply. Borrowers have taken full advantage, cutting the cost of their debt aggressively as repriced and new-money spreads converge. With new-issue supply expected to stay thin ahead of the late-summer break, there are signs that pricing is testing the limits of investor tolerance. The limits of the repricing wave were illustrated recently when CVC-backed Mehilainen repriced its €1.86 billion term loan at E+300 — a 50 bps cut, but short of the E+275 that some B2/B rated borrowers have attempted. Initial talk of E+300-325 was revised tighter to E+275-300, before the market settled at the wide end of the revised talk. “Fifty basis points on a good day, 25 bps on a bad day,” as one banker put it. The pattern is consistent across the late spring wave. The wave accelerated in the final week of May as B/B2 rated borrowers such as Colosseum Dental hit the E+300 benchmark. In contrast to January, when borrowers could slice large chunks from their margins, there is now little room to push beyond that level. So far in this wave, Ivirma is the only B2 rated name to print at E+275, matching the January tight set by Nord Anglia. Roll rates Demand has held firm regardless. In the case of Mehilainen, roll rates were reported at around 99%, with non-rollers largely limited to those unable to participate. Spare paper was allocated to new accounts and those willing to roll at E+275, sources added. In the extension of Refresco’s euro term loan to July 2032, which priced at E+275, no loose paper was reported at all. A supply imbalance in European loans is nothing new. Net institutional supply on a rolling six-month basis has been negative every month since the autumn of 2021. But the imbalance this year has been particularly severe, with a supply shortage of €22 billion in each of February and March. “There are a huge number of warehouses chasing paper, and the primary isn’t supplying what the market needs,” said one manager. The demand side continues to grow. Year-to-date CLO issuance of €26.4 billion is running fractionally ahead of the same period last year. The number of CLO managers pricing new deals has expanded from 20 in the final quarter of 2023 to 34 in the first quarter of 2026. “We are caught in a technical tidal wave that you cannot escape from,” said a second investor. Repricing has driven spread convergence across deal vintages. Across the 50 repricing transactions completed this year, the average starting margin was 361 bps. This is consistent with the 2021-2022 post-Covid vintage that still makes up 35-45% of the performing European Leveraged Loan Index. After repricing, margins have fallen to an average of 307 bps, matching the clearing level for new money from regular-way B2 rated names. Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe The new-issue market tells the same story. Trench Group recently wrapped a €1.4 billion recap at E+300, from initial talk of E+325-350. The deal refinances a €500 million term loan and helps fund a dividend of up to €1 billion. In early June, Smiths Detection completed a first-time buyout that included a €560 million tranche clearing tight of talk at E+300/par. In other recent deals, Socotec and Alvest both completed fungible add-ons at 100.25. Above-par prints are costly for CLOs, which are structured to build towards par, as buying above this level locks in an immediate markdown. The secondary market demonstrates this technical resilience, though this year’s path has been bumpy. The ELLI average bid fell 78 bps through January as repricing risk weighed on secondary prices. Software-related losses added a further 65 bps through February, a move that European high-yield, with little Software exposure, largely avoided. The war in late February and the closure of the Strait of Hormuz drove a third leg down, taking the index to a trough of 94.44 on March 9 — 2.22 points below where it had opened the year. The recovery was swift. By the end of April, the index had reclaimed 1.32 points. By mid-May, it was back near January levels. Diversity requirements The scarcity of new supply is also making it harder for CLO managers to meet diversity requirements. Total year-to-date activity of €101.63 billion is running behind last year’s €113.97 billion at the same point, and the composition of that activity tells the real story. Repricings account for €41.70 billion, and extensions and refinancings a further €40.59 billion. Non-refinancing new-money supply totals just €19.34 billion, down from €21.89 billion at the same point in 2025, a 12% decline. This is reflected in the structure of the ELLI itself. The index has grown from €234.5 billion at end-2020 to €352 billion as of May 2026, but the number of issuers has held broadly steady at 316-320 over the same period. CLO managers are competing for a larger pool of debt spread across broadly the same number of names. “In many ways we seem to have a repeat of last year,” said one investor. At the start of each year the market anticipated a recovery in M&A volumes that would bring new supply. Last year that expectation was derailed by US tariffs. This year, disruption first came from the Software sell-off driven by AI concerns, and then from the outbreak of war in the Persian Gulf. In both cases, the supply that banks and managers had hoped for failed to materialise. Prospects for new money ahead of the August break are limited. Debt backing the carveout of BP Castrol is in early birds, but underwritten fixtures such as Inpost, Recordati and DSM-Firmenich’s Animal Nutrition & Health business are not expected until the autumn. Further big-ticket supply is on the horizon. Iliad has arranged a €6.5 billion package to support its part of the acquisition of SFR from Altice France, and Ryan, a US-based tax advisory firm, is mandating banks for a debut euro term loan. Like Saint Augustine’s prayer, the market may receive the supply it needs — but not yet and certainly not before the August break. Pockets of value The search for pockets of value has sent managers back to parts of the market previously shunned. Trade disruption has slowed the entry of lower-cost Chinese products into Europe, giving a lift to domestic chemical producers, now the best-performing sector in the ELLI so far this year. “I wouldn’t say all of a sudden that everyone is uber constructive on chemical producers, but they are doing well enough for the time being,” said one manager. Much of the sell-off in Software names has also been reversed as managers sort out those credits whose business model is deeply embedded in client organisations from those that are more “nice to have” and so more vulnerable to displacement by AI. Names like Unit4 and SUSE, for example, are both now wrapped around par from quotes in the mid-90s in February. Business software group Think Cell, in contrast, is marked in the mid-80s, from the mid-90s in January, despite otherwise solid numbers. Sponsor Cinven continues to take advantage of the group’s depressed secondary price, offering to buy back a €20 million chunk of the group’s debt. Technical ceiling Signs that the market may be approaching its technical ceiling are emerging. In its European CLO Weekly published on June 8, BofA Securities noted that pressure is building on CLO weighted average spreads, with the median WAS for reinvestment-period European CLOs declining to inside 360 bps. This is down from above 400 bps in late 2023 and early 2024, before the repricing waves of the last two years. CLO liabilities have followed loan spreads lower, though not to the same extent. New-issue triple-A spreads are stuck in the high-120 bps area, and WACC for top-tier managers is running in the high-180 bps range. With loan spreads compressing faster than funding costs, the spread available to equity is narrowing. Yet managers continue to roll. “There is an argument that you should roll then sell, but it is extremely difficult to replace a high-quality asset at an acceptable price,” said one manager, adding that shedding repriced assets would quickly erode portfolio quality. Ineos Group’s refinancing illustrates the higher-yielding opportunities available to managers looking to rebuild WAS and barbell their portfolios. The European tranche, guided at E+500/96.5-97, suggests an all-in spread of 5.875% over four years for a B+/B2 (neg/neg) rating profile, a level that provides some relief amid a market otherwise grinding tighter. Bifurcation remains a feature of the market. Roughly 11% of the index was quoted below 90 at the end of May, down from 17% at the end of February, but still elevated. Defaults are ticking up and a growing list of credits remains troubled. Building Materials is among the sectors still under stress, even as Chemicals has recovered. How the consumer fares in the second half is a key question, and one that the standoff in the Persian Gulf makes harder to answer. “The longer the conflict goes on, the more uncertainty it is going to create,” said one manager. “How the consumer and discretionary sectors react is going to be quite difficult to call.” Featured image by Photolibrary/Getty Images This article originally appeared on PitchBook News Featured image by Photolibrary/Getty Images

Comments

You must be logged in to comment.