yahoo Press

McDonald’s Is Down 4% and Starbucks Is Up 25% in 2026. The Better Dividend Stock Might Surprise You.

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

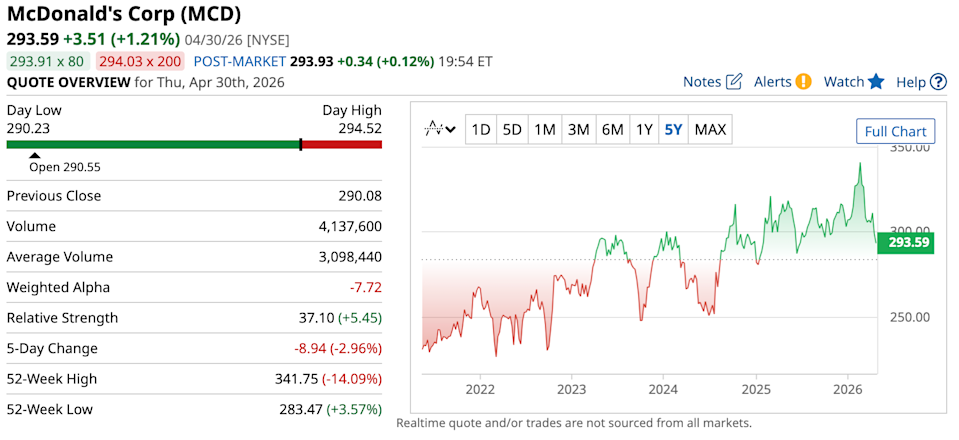

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Fast food is no longer just an occasional stop. For many of us, it's become part of our weekly routine, or for some like me, the morning routine- and it says a lot about how consumer habits have changed. People may cut back in some areas, but convenience matters. A quick meal, a familiar face, or a good cup of coffee to grab during a busy day can become surprisingly sticky. For investors, that makes certain food and beverage brands worth watching as they're not just selling products… they're selling a routine. And that's what makes McDonald’s and Starbucks worth putting side by side. Both are global brands that have found a place in consumers’ everyday lives, but the way they turn that demand into business results is not the same. So, which name looks more compelling buy today? Get exclusive insights with the FREE Barchart Brief newsletter. Subscribe now for quick, incisive midday market analysis you won't find anywhere else. The first is McDonald’s, easily one of the most recognizable restaurant brands in the world. It is best known for its chicken, sandwiches, burgers and arguably the best fast-food fries around. But aside from its menu, the company’s strength is consistency, with a franchise model that includes more than 45,000 locations worldwide. McDonald’s stock recently closed at $293.59, and it's down about 4% year to date. Then we've got Starbucks, one of the most famous coffee brands in the world, with over 41,000 stores. Best known for its coffee, the company aims to serve its customers’ habits by offering lattes, espressos, and other drinks- effectively integrating its business into people’s daily routines. Starbucks stock is up about 25% year to date and at the time of writing, it trades at about $105. So far, starbucks looks like it's got momentum, but does that make it the better buy, or is there more to this comparison? Let’s find out. McDonald’s is built around scale. The company has tens of thousands of franchisees that handle the day to day restaurant work while the McDonalds (corporate) collects rent, royalties, and other fees. The model is the single biggest reason McDonald’s has remained profitable in practivally every market worldwide. Meanwhile, Starbucks is more directly tied to the customer experience. It oversees its own company-operated stores, including control over its pricing, design, and other related operational needs. That comes with more exposure to labor, rent, and store-level costs. Put simply, these quick-service restaurants are not the same. McDonald’s is more franchise-centered, while Starbucks owns most of its stores and looks more like a premium coffee brand built around habit and loyalty. Now here’s their latest quarterly financial performance: Metric McDonald’s Starbucks Sales $7.01 billion $9.5 billion Net Income $2.16 billion $510.9 million Operating Cash Flow (FY 2025) $10.55 billion $4.7 billion Forward P/E (GAAP) 22.09x 51.84x Based on the figures, Starbucks had higher sales, coming in at $9.5 billion, compared with $7.01 billion for McDonald’s. Meanwhile, McDonald's is the more profitable of the two, reporting $2.16 billion in net income, compared with Starbucks’ $510.9 million. McDonald's also has better operating cash flow at $10.55 billion, compared with $4.7 billion for Starbucks. This matters because it shows how much money the business has to fund growth, pay dividends, and handle tougher periods. Valuation is another win for McDonald’s. Its forward P/E (GAAP) sits at 22.09x, above the sector average of 16.9x. Starbucks, meanwhile, trades at 51.84x, suggesting that it's more expensive, at least at current levels. Regardless, while Starbucks is bringing in more revenue, McDonald’s is generally better as far as the numbers go. Having a good earnings print is one thing, but being able to pay the shareholders is another. McDonald’s is just one year away from being a Dividend King, having raised its dividends for 49 consecutive years. It pays a forward annual dividend of $7.44, translating to a yield of around 2.5%. It also has a dividend payout ratio of about 60.5%, which is close to balancing company reinvestment and shareholder value. Meanwhile, Starbucks only started paying dividends in 2010. Today, it pays $2.48 per share, translating to a yield of approximately 2.35%, and a dividend payout ratio of 122.44%. This means Starbucks is currently paying out more than it earns, making the dividend look less comfortable than McDonald’s. While both companies offer similar yields, McDonald’s has a stronger dividend profile based on its history and payout ratio. The question is: does Wall Street have the same opinion as the figures? Analysts are bullish on McDonald’s, with 36 rating the stock a “Moderate Buy” and giving it a score of 3.97 out of 5. Meanwhile, the target prices suggest there's as much as 29.4% upside over the next year. Wall Street is also positive on Starbucks, with 38 analysts rating the stock a “Moderate Buy” and giving it a score of 3.63 out of 5, just slightly below McDonald’s. There could also be as much as 23.4% upside if the stock reaches its high target price. These two companies are among the largest and most recognized brands in the food and beverage industry. But for the sake of investing, the data shows that McDonald’s is the better pick even amid its slow performance since the year started. It has stronger cash generation, better valuation, a stronger track record, and analyst backing, giving it a clear edge in this comparison. For income-focused investors, it is worth noting that the dividend yields are nearly similar. Still, McDonald’s offers greater dividend stability, given its more balanced dividend payout ratio. Still, Starbucks could also be a good addition to one’s portfolio, especially for investors with a higher investment risk appetite. On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.