yahoo Press

52% of American investors fear IRS tax penalty as April 15 deadline hits

Images

1 / 4

2 / 4

3 / 4

4 / 4

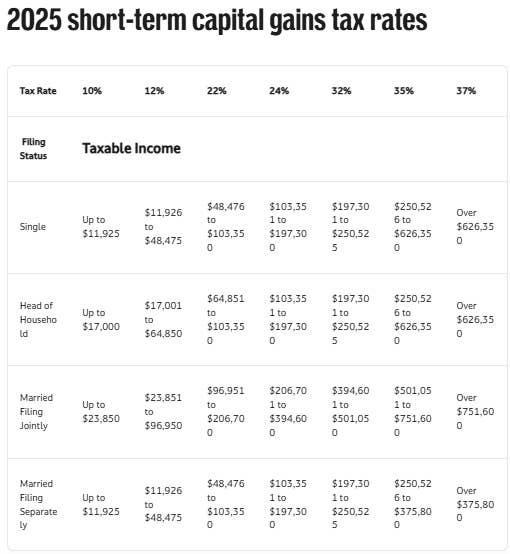

The deadline for Americans to file their federal tax returns for the year 2025 ends today on Apr. 15, 2026, and there is a fear among Americans that they could file their returns incorrectly and invite penalties from the Internal Revenue Service (IRS). Another common concern among some Americans is that they could fail to pay their taxes by the deadline and will have to pay late fees later. However, the IRS allows taxpayers to request an extension to file their tax returns to Oct. 15, 2026 to avoid any penalties. But note that the extension is only for filing the return, not paying the tax. The deadline for paying taxes remains the same: Apr. 15. If you fail to file your return by the due date (including extension), you invite a penalty of 5% of the tax due. The penalty accrues up to a maximum of 25%. Related: New IRS Form 1099-DA may trigger inflated tax payments As per a research conducted by Censuswide, 52.05% of crypto investors in the U.S. are worried about filing their crypto taxes incorrectly this year and receiving an IRS penalty. Only 24.68% of the respondents said they weren't worried about incorrectly filing their taxes and receiving penalty. The research was conducted among a sample of 1,001 crypto investors in the U.S. during Jan. 26-27, 2026. It's a legitimate concern because cryptocurrencies are still a new asset category and most people don't know how to pay their taxes on crypto. IRS reveals key details on U.S. tax refunds Crypto tax expert warns traders to 'fix your past' ahead of new IRS rule Coinbase executives warn IRS tax form 1099-DA causes confusion According to Notice 2014–21, the IRS treats crypto as property, which means when you buy, sell, or exchange cryptocurrencies like Bitcoin (BTC) or Ethereum (ETH), it's a taxable event and invites a capital gain tax. Short-term gains on crypto assets held for less than a year are taxed in the range of 10% to 37%, depending on income level. Long-term gains on crypto assets held for more than a year attract 0%, 15%, or 20% taxes, depending on income level. But you don't have to pay any tax if you simply buy and hold cryptocurrency. It becomes a taxable event only when you sell or trade it, which helps you realize a gain on the transaction. For instance, if you bought Bitcoin for $10,000 and sold it for $12,000, you have realized a gain of $2,000. The $2,000 gain here is a taxable event. American crypto investors are required to pay their crypto gains taxes and file their returns for the year 2025 by Apr. 15, 2026. Crypto brokers are issuing a new tax document called the Form 1099-DA to their users. But there is a catch. In its current form, the form reports a crypto investor's gross proceeds only, not the original purchase price or cost basis. Let's understand it in simple terms. Capital gains taxes are calculated by subtracting an asset’s cost basis from its sale proceeds. But the Form 1099-DA only mentions gross proceeds, leaving the responsibility of calculating the cost basis to the investor. In the example above, the broker would only mention the Bitcoin gross proceeds of $12,000 and it is your responsibility to report the cost basis of $10,000 to the IRS. This way, only the $2,000 worth of Bitcoin gain is taxed as capital gain. But if you fail to report the Bitcoin cost basis of $10,000, the IRS could tax the entire amount of $12,000 as gain. The full basis reporting is expected to come into effect in 2027. Until then, the crypto investors themselves are expected to track their digital asset transactions and report original cost basis prices for fair taxation. As reported earlier, Coinbase's VP of tax Lawrence Zlatkin expressed his concern about "complicated" tax rules for crypto users. He criticized the requirement to report every small transaction, including stablecoin holdings and gas fees. Billionaire Tim Draper doubles down on bold Bitcoin target Cathie Wood has brutal response to 50% Bitcoin crash Major gold holder launches self-custody wallet Andrew Duca, founder of the crypto tax platform, Awaken Tax, told TheStreet Roundtable in emailed comments that crypto investors behind on their taxes need not panic but they need to act. "The longer you wait, the harder it’s going to be.” He warned investors to not rely on gross proceeds reported by crypto brokers in Form 1099-DA, or else they could end up overpaying their taxes. Instead, they should connect every crypto exchange and wallet they have used and correctly calculate the cost basis of their crypto holdings, he advised. He also advised crypto investors to take advantage of losses from selling or trading cryptocurrencies to offset capital gains. "If losses exceed gains, you can deduct up to $3,000 against ordinary income annually, with remaining losses carried forward indefinitely." Duca also said it's best to voluntarily report your crypto taxes to the IRS. "The IRS's Criminal Investigation division is going after crypto cases more and more," he added and warned the consequences of voluntarily coming forward rather than being caught out are far less. The IRS is clamping down on crypto tax evasion and investors should be compliant and act now, he added. This story was originally published by TheStreet on Apr 15, 2026, where it first appeared in the MARKETS section. Add TheStreet as a Preferred Source by clicking here.

Comments

You must be logged in to comment.