yahoo Press

Russia Turns Asia’s Oil Shock Into an Indonesian Opening

Images

1 / 4

2 / 4

3 / 4

4 / 4

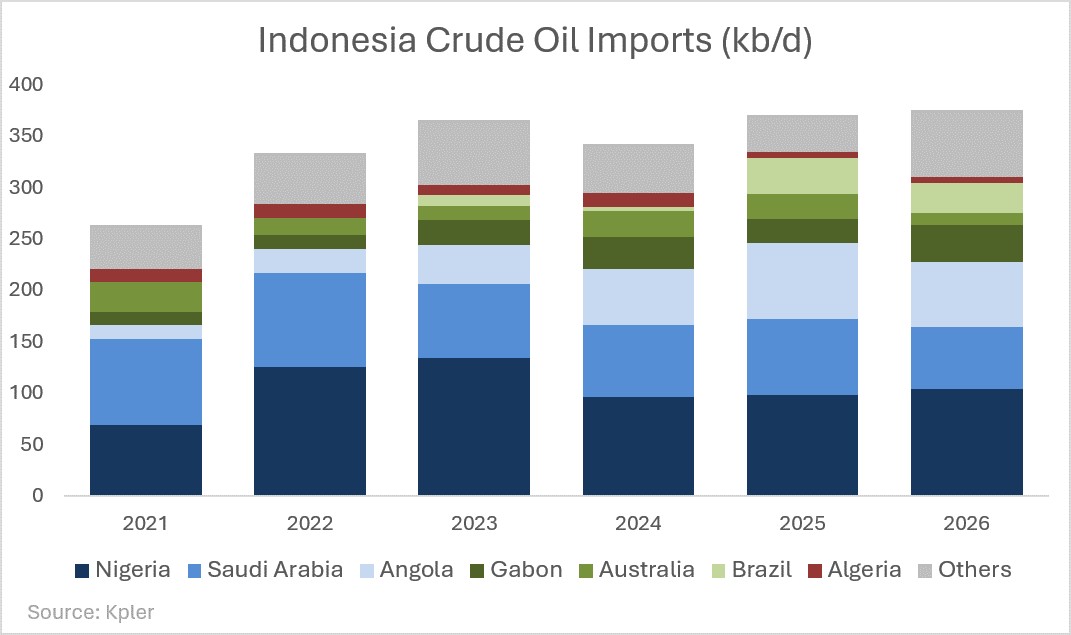

Russia has emerged as one of the clearest commercial beneficiaries of the US-Israel war with Iran. Before March 2026, buying Russian crude was widely treated as a sanctions risk that only Chinese and, to a lesser extent, Indian private companies could comfortably absorb. The first US waiver for Russian barrels, announced on March 12, changed that calculation. It showed that, during a major Middle Eastern supply disruption, Asia could not balance its oil market without Russian crude, and even Washington was aware of the that. Successive waiver extensions kept Russian oil trade legal across parts of Asia and encouraged regional buyers to view Moscow not only as an emergency supplier, but as a tool of energy security. In this context, the emerging oil relationship between Russia and Indonesia is one of the clearest examples. Relations between Moscow and Jakarta have deepened since Prabowo Subianto was elected president in early 2024. Indonesia became a full member of BRICS in January 2025 and subsequently signed a free-trade agreement with the Eurasian Economic Union. Energy cooperation now appears to be moving from diplomatic declarations toward a more formal trading structure, especially in the hydrocarbons area. Indonesia has a strong economic reason to diversify. Crude output was around 577,000 b/d in May 2026, below the 610,000 b/d government target and down from roughly 1.5 million b/d in the 1990s as mature fields declined. That is insufficient for a refining system with 1.2 million b/d of nameplate capacity and actual runs near 950,000 b/d at roughly 80% utilization. Indonesia therefore faces a crude deficit even before accounting for the limitations of the barrels it produces (some local crude is too light for domestic plants). Indonesia exported around 40,000 b/d last year, mostly to Thailand. But an even bigger imbalance is in refined products: total petroleum demand is around 1.6 million b/d, well above domestic refinery throughput, forcing Indonesia to import both crude and refined products. Indonesia bought about 370,000 b/d of crude on average in 2025 and 2026, led by West African producers - Nigeria at around 100,000 b/d, followed by Angola, Gabon – as well as Saudi Arabia and Brazil. Purchases mostly boil down to medium-sweet grades such as Escravos, Nemba or Gabonese blends, alongside Saudi medium-sour barrels. The mix reflects refiners' need for lighter products. Gasoline is where the supply deficit is most pronounced. Demand is running at around 690,000 barrels a day, of which as much as 60% is covered by imports. Average gasoline imports reached about 430,000 barrels a day in 2025, exposing a structural shortage of domestic production. Diesel is less constrained because Indonesia operates a biodiesel mandate and ultimately plans to eliminate conventional diesel imports. For now, however, it still buys diesel overseas. Russia has become the major supplier since the waiver on its oil and oil products was issued in March, with sporadic cargoes rising during the latest crisis and reaching 26,000 b/d in April 2026. Russia therefore, has already offered Indonesia more than one type of supply. However, only two vessels carrying Russian crude reached Indonesia in the past six months. Each transported about 700,000 barrels from Sakhalin-2, one loading in late December 2025 and the other in January 2026. Both carried Sakhalin Blend, a light, sweet crude with an API of about 45 degrees and low sulphur content, making it a good fit for gasoline-oriented refining. The more consequential development came after Prabowo's visit to Moscow in mid-April. Russia reportedly committed to supplying Indonesia with 100 million barrels of oil (potentially including both crude and refined fuels) at a preferential price, with a further 50 million barrels available if required. Jakarta then created a legal route. A late-April regulation authorized public service agencies to import crude, fuels and LPG under intergovernmental cooperation or direct agreements. On June 8, Indonesia's energy minister assigned Lemigas, an agency under the energy ministry, full responsibility for carrying out crude imports, including potential purchases from Russia. The arrangement could shield state-owned Pertamina from direct commercial ties with sanctioned Russian companies. The company depends on international bond financing and is sensitive to any action that could breach bond-related sanctions obligations. Routing purchases through Lemigas would shift trade toward a government-to-government structure, which would not provide a total sanctions immunity, but targeting an Indonesian state agency could carry a greater diplomatic cost for Washington. Payments remain a major obstacle: US-dollar settlement is unlikely to work, and most commercial banks may avoid the risk. Yet recent comments by Indonesia's Energy Minister Bahlil Lahadalia may offer a clue to how the two sides could structure the relationship. Lahadalia said Russia had expressed a willingness to help Indonesia construct several important pieces of infrastructure, that could mean storage or marine terminals. Or it could also breathe new life into the proposed 300,000 b/d Tuban refinery project. Rosneft has partnered with Pertamina since 2016, but the $24 billion project remains stalled, and by mid-2026, full construction had not begun with Rosneft's final investment decision still pending. Government-to-government trade could theoretically support barter arrangements, exchanging oil for infrastructure-related expenses and reducing direct monetary settlement. A key question is which Russian grades would define potential Indonesian imports. Loading capacity should not be a major constraint, as most Russian seaborne crude is currently sold on the spot market and can be redirected relatively easily. ESPO from Kozmino is the most likely option. The voyage takes only around 12 days, while the grade's 35 degrees API gravity and low sulphur content closely match Indonesia's existing import crude mix. Kozmino's roughly 1 million b/d loading capacity also allows cargoes currently directed mainly for China to be redistributed, potentially tightening the spot market and supporting higher differentials. Sokol from Sakhalin-1 is another strong candidate. It is similarly light and sweet, at around 40 degrees API and 0.2% sulphur, although loadings are much smaller at roughly 200,000 b/d. Indonesia would still need medium-sour barrels, as it has been importing some volumes of Saudi Arabia's flagship Arab Light grade. With Saudi crude relatively expensive, Urals from Primorsk and Ust-Luga could offer a cheaper substitute for it, even after a voyage of around 40 days. Distance is a bigger problem. A voyage from Sakhalin to Indonesia can take around 15 days under normal conditions, although the two recent cargoes took about 42 days. From Primorsk, the journey is closer to 45 to 50 days. Those routes make sense during an emergency, which helps explain why Russian diesel from Primorsk has reached Indonesia in recent months. Their longer-term viability will depend on discounts, freight costs, and any additional benefits Moscow offers, including storage, refinery, or terminal investment. The Middle Eastern crisis has therefore done more than temporarily boost Russian exports. It has encouraged Asian governments to reconsider what buying Russian oil represents. The Philippines began importing Russian crude under the US waiver in March 2026, after state oil company Petron agreed to purchase 2.5 million barrels in the country's first such deal since 2021. Manila has already received three cargoes across March and May and is reportedly discussing how to formalize the trade through a government-to-government framework similar to the model being considered by Indonesia. Vietnam has also reportedly been in talks with Moscow since March over the potential start of Russian oil imports. What began as an exceptional response to a supply shock is becoming a test of whether sanctions policy can coexist with the energy-security needs of large importing economies. Indonesia's case matters because it is neither a traditional Russian client nor a market able to absorb unlimited legal and financial risk alone. But the shift is already clear: in Southeast Asia, Russian oil is increasingly being treated not as a prohibited commodity, but as an instrument of national energy security. By Natalia Katona for Oilprice.com More Top Reads From Oilprice.com China's Teapot Refineries Cut Operations to Their Lowest Level Since 2017 Adani Targets 10 GW Nuclear Power Capacity in India by 2035 VLCC Earnings Near $470,000 a Day as Hormuz Hopes Drive Tanker Frenzy Oilprice Intelligence brings you the signals before they become front-page news. This is the same expert analysis read by veteran traders and political advisors. Get it free, twice a week, and you'll always know why the market is moving before everyone else. You get the geopolitical intelligence, the hidden inventory data, and the market whispers that move billions - and we'll send you $389 in premium energy intelligence, on us, just for subscribing. Join 400,000+ readers today. Get access immediately by clicking here.

Comments

You must be logged in to comment.