yahoo Press

PE pivots as platform buyouts in software fall to decade low

Images

1 / 4

2 / 4

3 / 4

4 / 4

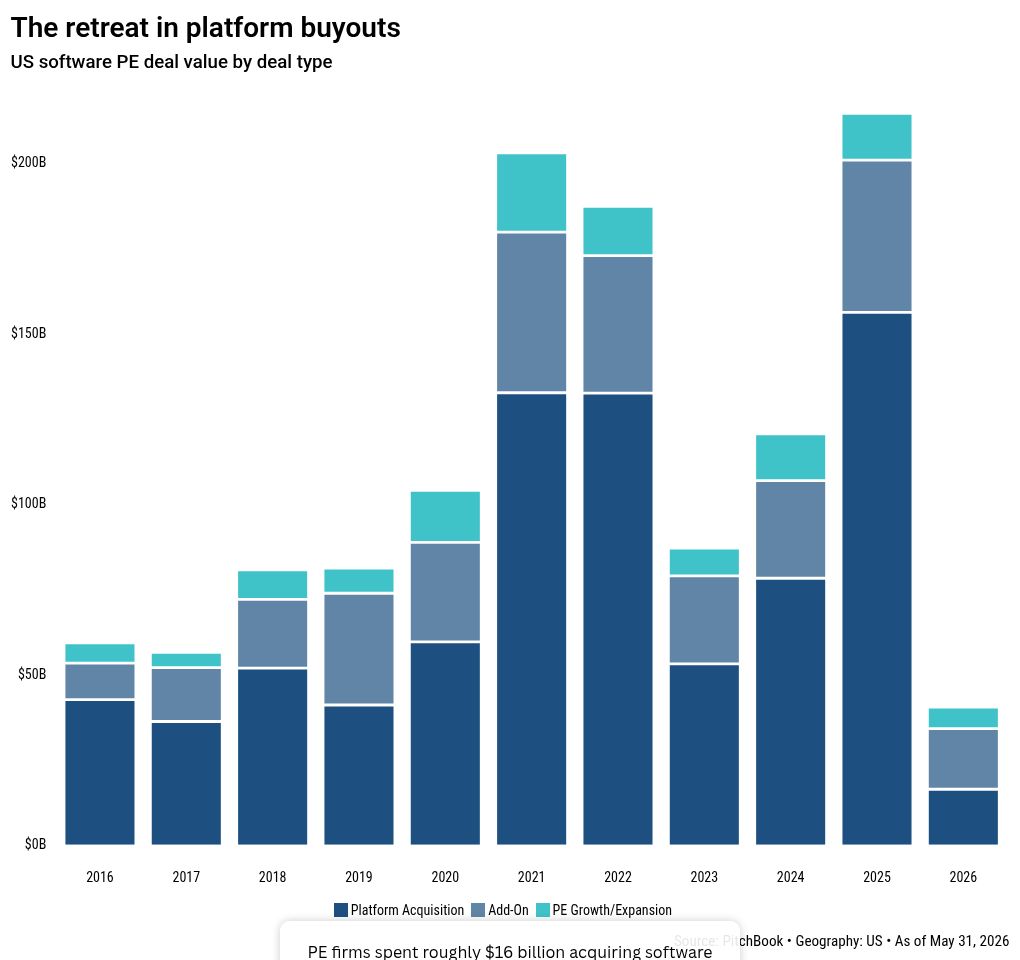

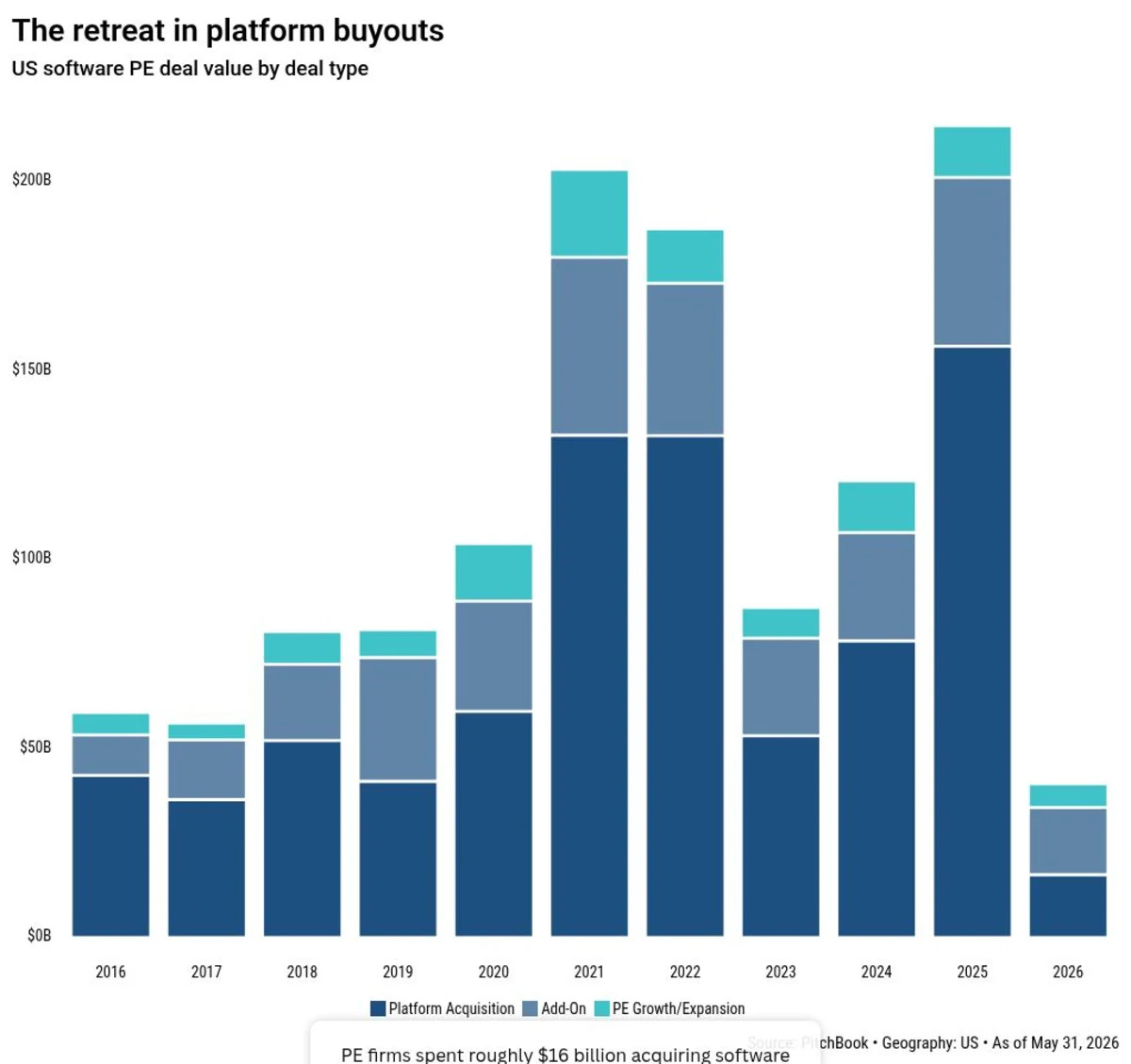

Private equity's buying spree in software slowed to a trickle in 2026. But a closer read on the market reveals that dealmaking isn't dead—it's just getting done in different ways. Big-ticket buyouts have fallen out of favor, while tuck-ins and growth equity deals have stepped in to fill the gap for managers still looking to deploy their war chests. A less accommodating credit market, the threat of AI disrupting revenue models, and a sharp valuation reset dented platform acquisitions, driving US deal value in software to just $16.24 billion during the first five months of this year—a pace that would put 2026's full-year tally at roughly a quarter of 2025's record $156 billion, according to PitchBook data. While platform buyouts have pulled back across the broader LBO market, the retreat has been particularly stark in software. Platform deals accounted for 41% of overall PE deal value in software, the lowest share in at least a decade and a 30-percentage-point decline from a year earlier. By contrast, US PE overall saw its share of platform LBOs slip from 21% at year-end 2025 to around 19% through May, a more modest decline, according to PitchBook's 2026 US Private Equity Outlook: Midyear Update. Running counter to that decline, add-ons and growth equity deals—which typically require smaller equity check sizes and less debt—held far better. Add-ons, totaling roughly $18 billion, expanded their share of total software deal value to about 45% over the same period, more than doubling their share from last year. Growth equity deal value rose slightly. Fears that AI could easily commoditize some software applications and erode their pricing power—the so-called SaaS-pocalypse—have put pressure on valuations and sapped investor appetite. In addition, a recent high-profile software restructuring deepened that caution. A creditor group led by Blackstone took control of software maker Medallia this month after its PE sponsor Thoma Bravo declined to put in more cash against nearly $3 billion in debt the company could no longer service. Thoma Bravo, which took Medallia private for $6.4 billion in 2021, is expected to lose as much as $5.1 billion, according to reports. The collapse illustrated how quickly a debt load—seemingly manageable in the near-zero-interest-rate era—could become unbearable as the market shifted, wiping out a sponsor's equity overnight. "It's a bit like getting punched in the gut," said Craig Muir, head of software, data and analytics at investment bank Solomon Partners. "You lose your breath for a period of time and are cautious about going back into the fray, so you just wait. But people are starting to understand that business must go on, and we need to build and buy capabilities, so let's start to lean into some of these opportunities while others are still cautious." With lower risk appetites, many PE firms backed away from large buyouts and instead focused on acquiring tuck-ins, minority positions or smaller platforms, he added. That sentiment is showing up in the shrinking deal size of platform buyouts: Only seven software platform deals have cleared $100 million in 2026 to date. It is a sharp contrast from last year's boom, when the 10 largest platform deals each topped $2 billion, led by the high-profile $55 billion buyout of video game maker Electronic Arts—the largest LBO ever inked. The largest software platform acquired so far this year was Onestream Software, a financial software maker that embeds AI to automate financial planning and analysis reporting. Hg took the company private for $6.4 billion—and even there, Hg split its equity check with General Atlantic and growth equity firm Tidemark, which joined as minority investors. Other anchor deals closed at lower price tags. The second-largest was Sirion, an AI contract software maker, acquired at an enterprise value of roughly $1 billion. The PE backer was an emerging manager—Austin-based Haveli Investments—an uncommon sight in a sector long dominated by big-name managers. Founded by Vista co-founder Brian Sheth, Haveli closed its debut buyout fund at $4.5 billion last July. This article originally appeared on PitchBook News

Comments

You must be logged in to comment.