yahoo Press

European direct lenders mull software deals as AI shapes sector

Images

1 / 4

2 / 4

3 / 4

4 / 4

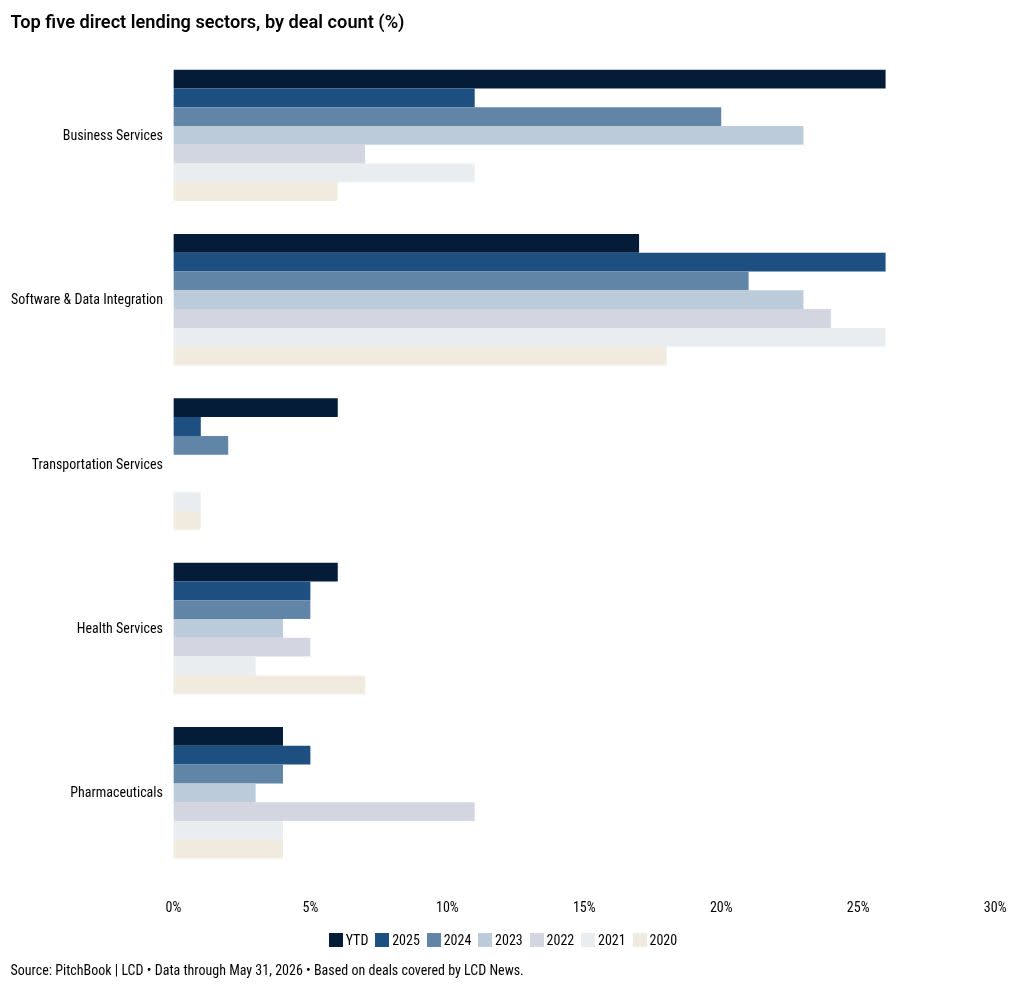

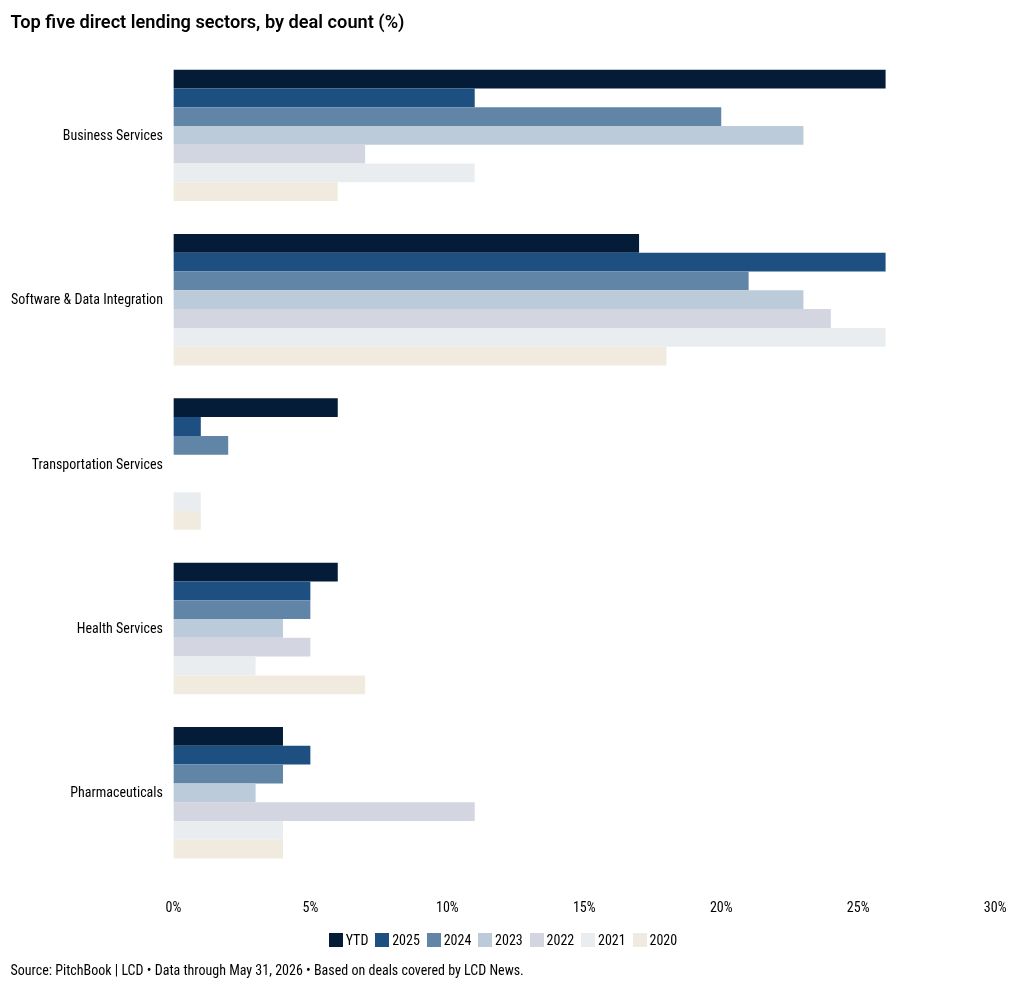

The conventional read on European private credit is that software, the defining sector of the 2021-2022 market boom, has fallen out of favour. The sector has not been abandoned so much as re-examined, however — with a fault-line now separating financeable and unfinanceable software companies, according to their exposure to artificial intelligence. The shift in sentiment here has been sharp, and some market participants argue that it’s been overdone. “Some investment managers are going to zero on their investing in software assets right now,” said Andrew Cleland-Bogle, partner at Bridgepoint Credit, speaking on a panel at the SuperReturn event in Berlin earlier this month. “I personally think that’s a huge mistake,” Cleland-Bogle said, adding that good opportunities exist in all market conditions, and that many software businesses stand to benefit disproportionately from the very technological shift that has spooked investors. “Emotion creates opportunities, and I think we’re seeing that in the market right now.” Price discovery Market participants also say the retreat from software looks less like panic than price discovery. “The issue with software transactions is not that these are all of a sudden bad deals,” said Mark Fine, partner at McDermott Will & Schulte. “It’s just a question of, do we get an EV multiple of 15-18, or 10-12?” Fine notes that lenders are not fleeing the sector over AI, and that their hesitation is about what multiples are being paid — not whether the business is financeable. “It has become quite binary as to whether the deal is financeable or not,” he added. During the boom years for private credit, software’s reputation as a COVID-resilient sector pushed multiples to levels that left some capital structures over-leveraged against inflated valuations. “Lenders are more focused on underwriting software deals correctly, as well as making sure churn rates aren’t high, and that customer concentration is not super-high,” Fine said. “They are going through situations with a fine-tooth comb,” he noted, while adding that provided a business shows the ability to turn profitable with genuine cash conversion, lenders will do the deal. Cegid is a good example of this dynamic. The French group — a maker of finance and HR software, and a well-regarded credit in the syndicated market since 2016 — had lined up a bank bridge loan to fund its acquisition of the fintech Shine. The plan to take that bridge out in the syndicated loan market cooled amid the broad software sell-off early this year, so direct lenders stepped in instead with a €1.1 billion private credit loan led by Arcmont and Ares that closed in June and funded the deal. Time factor In Germany, an M&A adviser said caution on software has spread to existing portfolios, where sponsors can no longer exit at a higher multiple than they paid. “That’s why many software deals are struggling to trade,” the adviser added. On AI, the threat is widely seen as real but slow-moving. Lenders that have grown comfortable with exposed assets have done so with the view that AI will erode margins over a six-to-seven-year horizon rather than a two-to-three-year outlook — which is long enough to make a five-year loan defensible, one debt adviser noted. Quality street Mattis Poetter, partner and chief investment officer at Arcmont Asset Management, stresses that not all software businesses are the same when it comes to credit quality. At one end of the spectrum sit systems of record, enterprise resource planning (ERP), accounting and human-resources software services that are embedded deep within customers’ operations. “Such businesses have long carried very low customer churn,” Poetter said, adding that replacing them is costly, disruptive and risky. “If you’re providing the system of record and you’re extremely entrenched, it’s much harder to disrupt.” At the other end are ‘point solutions’ that sit on top of ERP and data-service businesses. Poetter said such operations historically generated much higher churn and were easier to grow and scale, but are now the firms most exposed to AI-native challengers. “It’s much easier for a new AI seller to rebuild and provide a very good product,” he notes. Poetter says the greatest risk lies elsewhere, however — in the shape of white-collar business-process outsourcers and specialised service providers with limited competitive moats, where AI can already automate much of the workflow. The risk to quality software, market participants said, is margin compression rather than obsolescence. Enterprises will not switch core operating systems for a modest cost saving when the security risks, need for retraining and operational disruption make such change a non-starter, market participants note. “The more relevant question is who captures the efficiency gains that AI delivers, and whether it’s the company or its customers,” said a source. Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe Fewer competitors The re-sorting of the market is meanwhile thinning the field of lenders that are willing to write software cheques. Several market participants said some managers accumulated heavy software exposure during the 2021-2022 market boom, without developing a framework to distinguish the stronger businesses from weaker ones. Now that scrutiny has intensified, those lenders are retreating. Furthermore, investment committees have turned markedly more reluctant on technology and software after the market wobble early this year, one debt adviser said. For lenders with genuine software expertise, that retreat represents an opportunity in that there’ll be fewer rivals chasing the assets they understand best, and an easier case to make to the institutional investors that dominate European private credit. “It’s much easier for lenders to have that conversation and convince investors there’s a big differentiation within software, and what’s a tier-one asset,” said Andrew Hamilton, director of debt advisory at Carlsquare. That selectivity is slowing deals down — but in a specific way, with some investors considering the plausibility of replicating certain individual software models with the latest AI tools. “People are getting more creative in considering the downside risks from AI, and are more willing to do their own research to validate assumptions around resilience — as well as understanding how software is actually being used by clients and its integration with essential workflows,” Hamilton said. Meanwhile, the volatility seen in the software sector this year has scrambled the wider definition of what investors consider to be a good strategy. A purely SaaS-focused fund, for example, now faces “a massive hit on book values,” a partner at a German private equity firm noted, making diversified mandates far more attractive for investors. “Who would have bet on software companies being out of favour this year? Nobody,” said the partner. Real deal Among managers still willing to underwrite the sector, appetite is shifting toward software that’s embedded in the real economy. Europe’s edge may lie less in building AI than in deploying it, market participants suggest. Foundational models are largely a US story, but rolling them out across the continent’s fragmented languages, regulation and vast base of smaller companies represents a durable growth opportunity in technical services and consulting, and — in time — a new seam of businesses for private credit to finance. Cleland-Bogle at Bridgepoint said he is seeing the most attractive opportunities in businesses where AI acts as an enabler rather than a threat, such as critical B2B, healthcare and industrial companies, where the technology can drive better margins and efficiency. “You just have to be able to find those opportunities,” he said. “And right now you’re seeing them at more normalised valuations, moderate leverage and attractive yields.” Featured image by BlackJack3D/Getty Images. This article originally appeared on PitchBook News Featured image by BlackJack3D/Getty Images.

Comments

You must be logged in to comment.