yahoo Press

MU Stock Rises as Micron Teams Up With Anthropic on AI Infrastructure

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

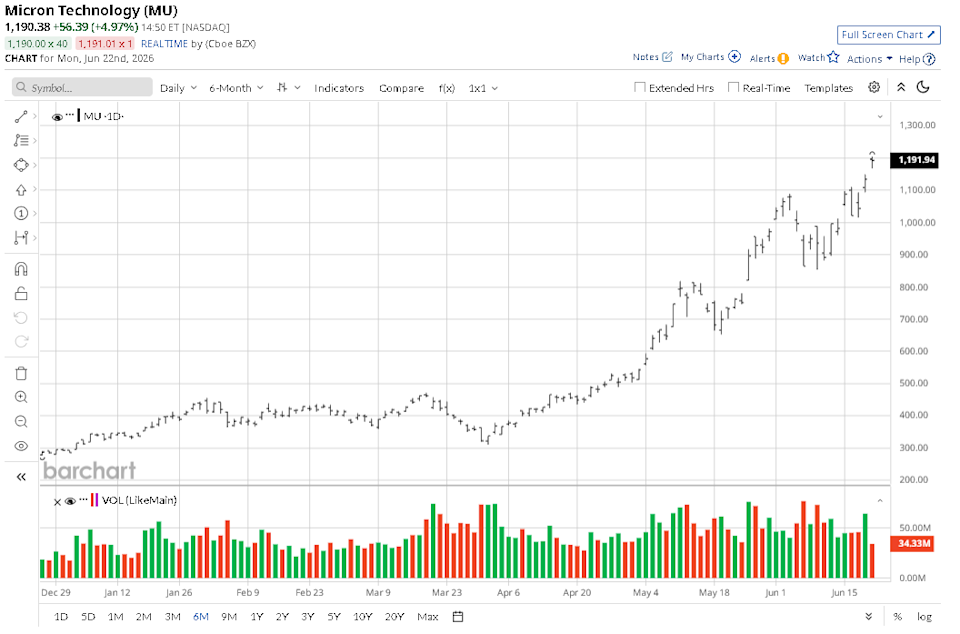

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Micron (MU) extended gains on June 22 after announcing a strategic partnership with Anthropic aimed at co-designing and securing hardware infrastructure for massive AI workloads. As investors cheered the Anthropic news, MU’s relative strength index (RSI) looks poised to climb into the early 70s, indicating overbought conditions that often trigger a selloff. Dear Microsoft Stock Fans, Mark Your Calendars for June 30 Micron Technology Earnings: Bull Put Spread Trade D-Wave Just Unveiled a Major Quantum Breakthrough. QBTS Stock Looks Ready for Another Surge. Stop Missing Market Moves: Get the FREE Barchart Brief – your midday dose of stock movers, trending sectors, and actionable trade ideas, delivered right to your inbox. Sign Up Now! Micron stock has been nothing short of a blockbuster investment in 2026, currently up roughly 300% versus the start of this year. The landmark agreement with Anthropic is highly bullish for MU shares because it reinforces the chipmaker’s role at the bedrock of next-generation artificial intelligence infrastructure. Under the multi-year deal, Micron is making a strategic investment in Anthropic’s Series H funding round, while simultaneously locking in a massive commitment to supply high-performance memory and storage architecture. This includes specialized hardware essential for training and serving Anthropic’s flagship Claude models. On Monday, co-founder Tom Brown emphasized that advanced memory is the primary bottleneck in scaling AI, making Micron’s High-Bandwidth Memory (HBM) and DRAM indispensable for Anthropic’s future roadmap. In short, the team-up gives MU multi‑year, visibility‑rich demand for HBM — the highest‑margin product in its portfolio. Micron is scheduled to report its fiscal Q3 earnings on June 24, which are broadly expected to drive its stock price even higher in the near term. Consensus is for the multinational to post record-breaking numbers, with revenue expected to come in at about $35 billion on a more than 10x increase in adjusted earnings per share (EPS) to $20.81. Ahead of the quarterly print, Bernstein analysts led by Mark Li reiterated their “Outperform” rating on Micron shares and more than doubled their price target to $1,300. In his research note, Li argued that a prolonged DRAM shortage and rising pricing premiums will drive MU’s profit margins to an unprecedented peak. Other Wall Street analysts seem to agree with Li’s bullish stance, especially since MU stock is still trading at a rather attractive 19x forward earnings multiple. The consensus rating on Micron Technology remains at “Strong Buy,” with price targets as high as $1,750 indicating potential upside of a whopping 45% from here. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.