yahoo Press

Leveraged loan issuers increase amend-and-extend deals to take out credit facilities

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

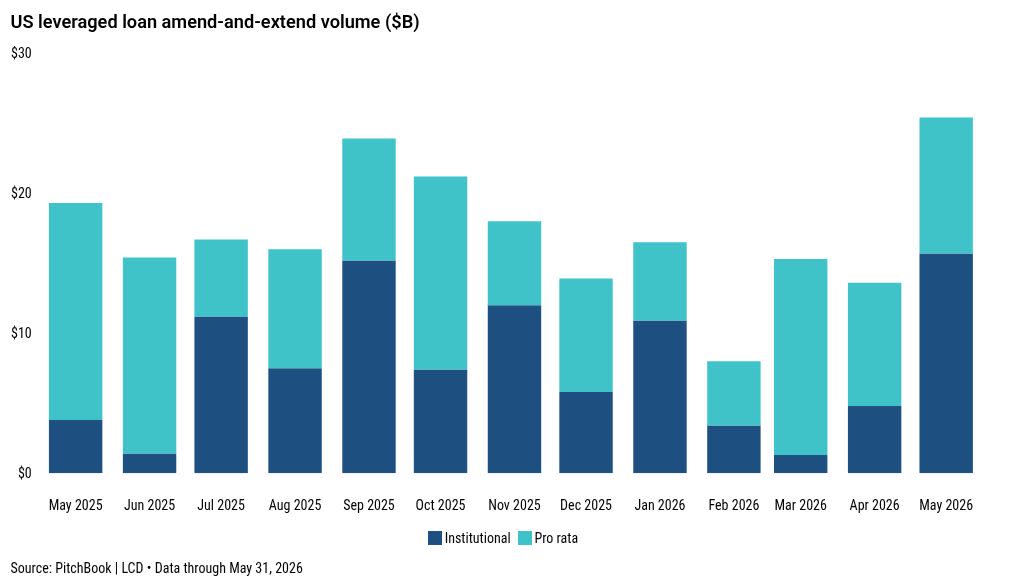

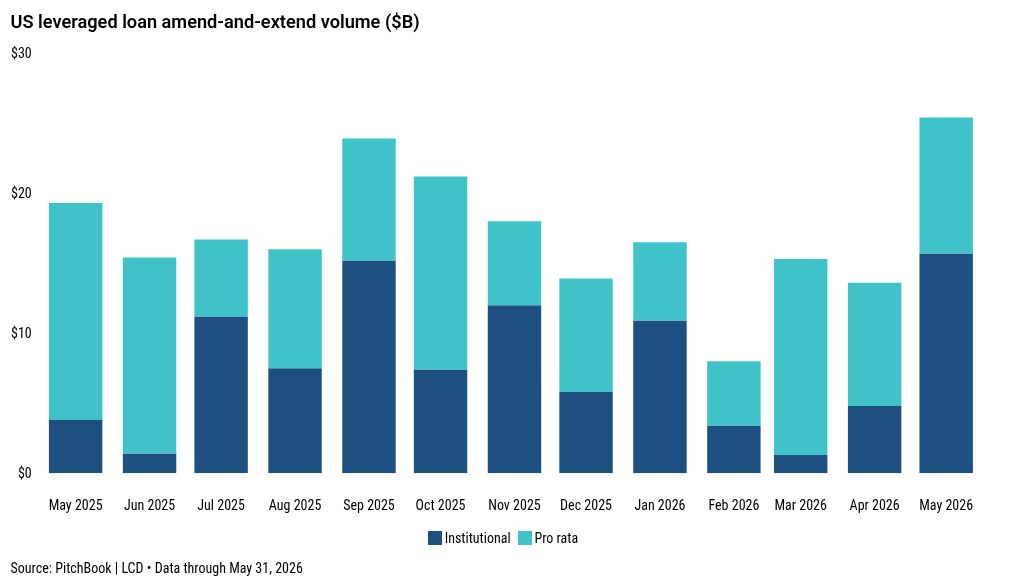

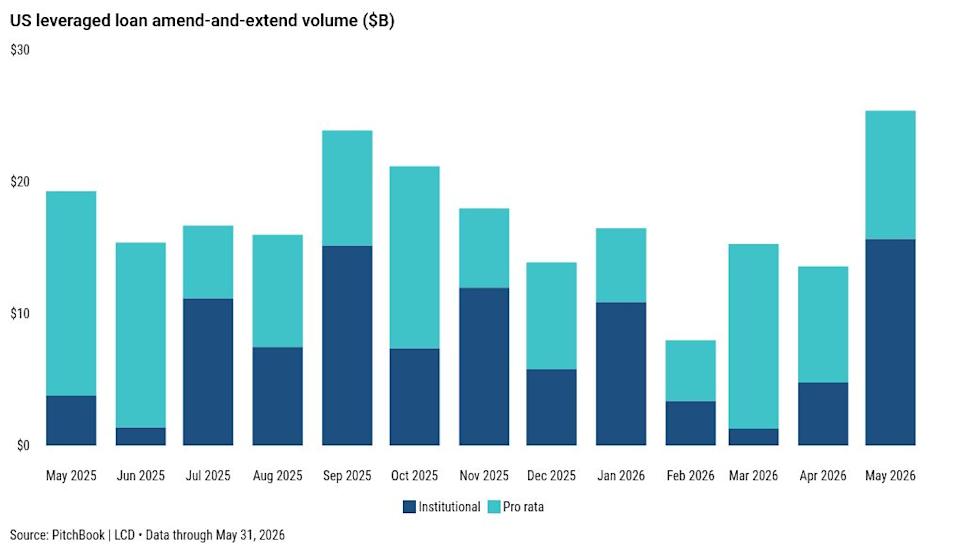

Amend-and-extend loan volume jumped to $25.4 billion in May, a high for any month since June 2024, according to LCD. May’s amend-and-extend activity came via 19 transactions, up from 18 transactions (for $13.6 billion) in April. Nearly $79 billion of volume this year is up from roughly $68 billion through the first five months of 2025. Borrowers continued to seek amendments, as opposed to refinancings, to take out credit facilities. The average yield to maturity for refinancing institutional term loans via syndication currently stands at 6.7% for 2026, which is lower than 7.4% in 2025 and the 8.6% in 2024, but still elevated from all the years spanning 2011-2022. Year-to-date, the distribution between institutional A-and-E issuance ($36.2 billion) and pro rata issuance ($42.7 billion) has been fairly balanced. May’s A-and-E activity was concentrated in institutional deals ($15.7 billion, versus $9.7 billion in pro rata volume). Note that pro rata debt typically entails amortizing TLAs and/or revolving credit facilities and is traditionally syndicated to finance companies and banks. Institutional debt consists of term loans structured specifically for institutional investors, including CLOs. The Oil & Gas sector tops A-and-E volume in the YTD, at 16%, followed by Retail and Services & Leasing at 9% each. Technology (excluding software) and Manufacturing & Machinery each account for 8%, while Chemicals and Food and Beverage both account for 6%. Building Materials, Healthcare, and Software and Data round out the top ten at 5% apiece. While there is heightened urgency to address near-term maturities, LCD data show that the companies being given breathing room are, by and large, not immediate default candidates. Roughly 71% of the amendments completed in 2026 were rated B-minus or higher at the issuer level. However, that’s down from the 77% in 2025 and 84% in 2024. In 2026, sponsored transactions account for 40% while non-sponsored deals make up 60% of the A-and-E total. The sponsored share has ticked back up from 38% in 2025, moving closer to the elevated levels during the unusual spike in sponsored issuance in 2023-2024, and running above the decade’s average of roughly 38%. In 2025, sponsored and non-sponsored companies with pro rata loans were focused on extending 2026 and 2027 maturities — extending $37.6 billion of debt due in 2027 and $36.7 billion due in 2026, along with $13.8 billion due in 2028. So far this year, borrowers have extended $20.2 billion of pro rata facilities due 2027, $11.1 billion due in 2029 and $5.3 billion due in 2028. On the institutional side, activity in 2025 was concentrated in 2028 maturities, with borrowers extending $53.8 billion coming due that year, along with $12.7 billion of institutional loans coming due in 2027. So far this year, borrowers have extended $17.2 billion of institutional facilities due 2028 and $12.6 billion due 2029. Within the institutional segment, the Software sector has seen notable A-and-E activity year-to-date, with transactions including Conga, Gen Digital, Yahoo/Verizon Media, Optiv Security, and Athenahealth. Turning to the maturity wall, the amount outstanding in the leveraged loan market per the Morningstar LSTA US Leveraged Loan Index was $1.55 trillion at the end of May. Loan volume maturing through the end of 2027 narrowed to $36.5 billion by the end of May, from $61.9 billion at the end of 2025. The amount of loans coming due in 2029 and beyond, however, grew by $89.5 billion from the end of 2025 through the end of May. Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe General_4530/Getty Images This article originally appeared on PitchBook News General_4530/Getty Images

Comments

You must be logged in to comment.