yahoo Press

PE firms want software deals, but lenders don't want to fund them

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

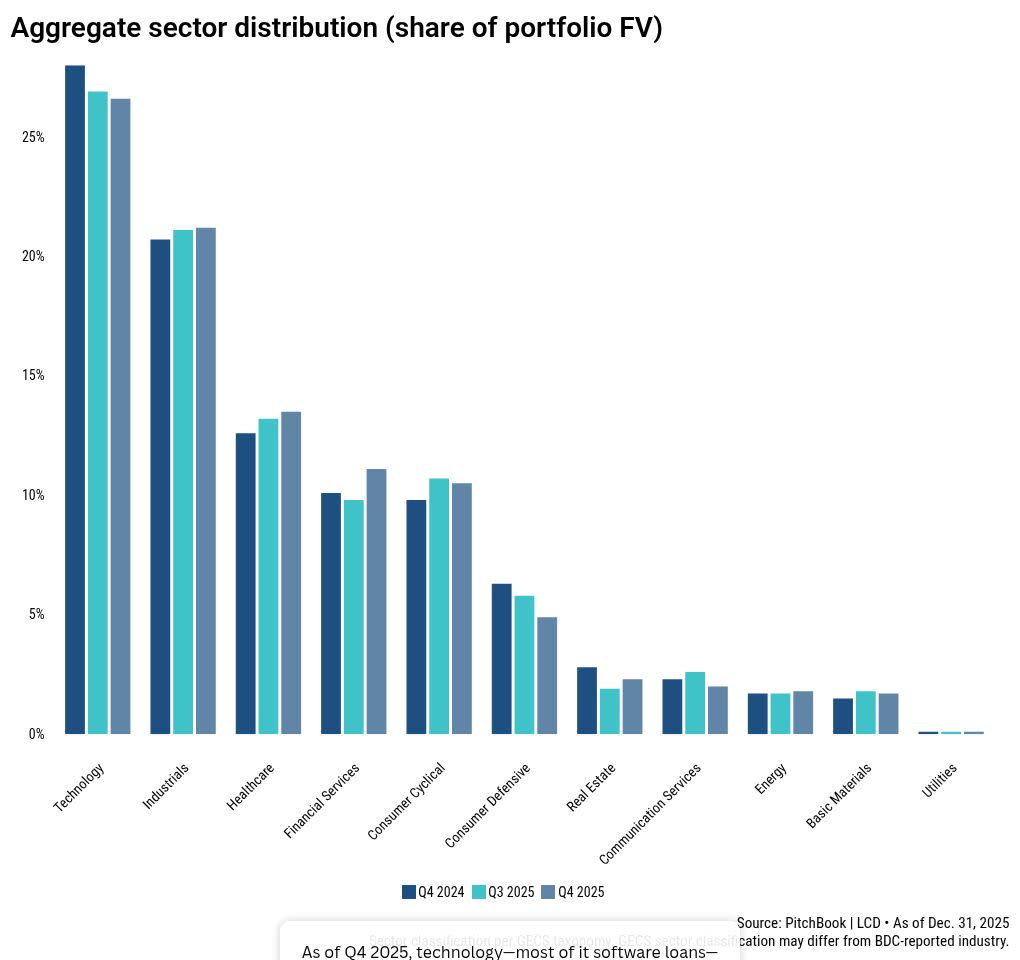

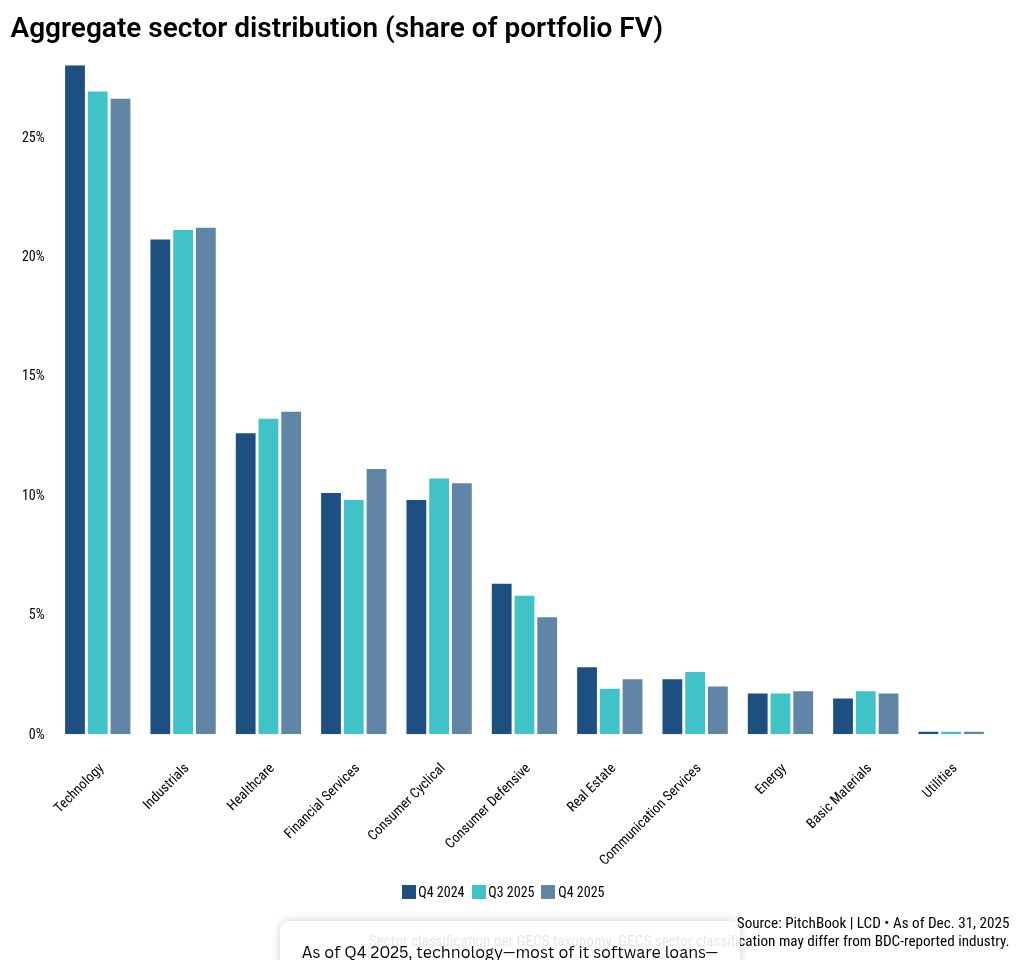

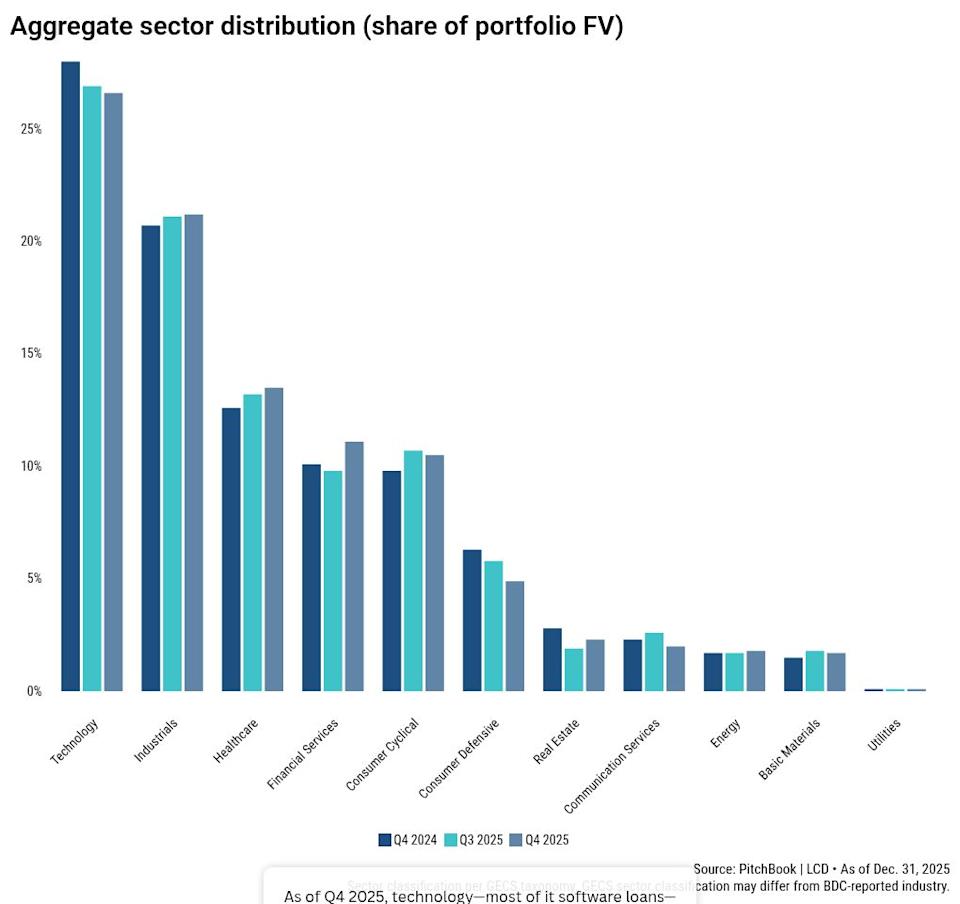

Private equity dealmakers chasing software deals have found themselves running into a wall: Industry linchpins that had long been their go-to lenders for financing have gone quiet. The pullback from software lending, triggered by the threat of AI’s ability to upend businesses, spans across the private credit market, but some big managers have been particularly reluctant to add new software exposure, several industry sources told PitchBook. While some PE managers want to push ahead and buy companies they believe will thrive in the era of AI, their calls for term sheets are being turned down, causing frustration at the sudden retreat of longtime partners. “For some of these deals, lenders just say, ‘Don’t even think about it. We have too much software exposure. We are not going to fund another software buyout,” said one M&A lawyer, adding that they are working on two deals where the parties have completed due diligence, but no committed lender has been found. The squeeze signals a notable shift for a sector that has long been the driving force behind leveraged buyout activity. Roughly $17 billion worth of US software buyouts were closed or announced during the first five months of this year, according to PitchBook data. That figure is about half of last year’s pace and represents only 17% of the $99.2 billion recorded in the same period in 2022, which was the highest total in a decade. Deal count fell to 216, the second-lowest total for the first five months of a year since 2020, trailing only 2023. That contrasts with the accelerated pace seen in growth equity deals, where PE firms take minority stakes in businesses and typically do not require debt financing. PE firms inked 138 such deals through May this year—up roughly 30% from last year, though total deal value came in at just $2.74 billion. Blue Owl Capital, Blackstone, Apollo Global Management and BlackRock’s HPS Investment Partners are the types of lenders that have scaled back new loan originations in software, according to an investment banker who focuses on deals in the technology industry. Apollo has taken a cautious view on software since well before the AI-triggered anxiety roiled the SaaS market. At the Bloomberg Invest summit in March, CEO Marc Rowan publicly warned peers who appeared to have only recently woken up to AI risk: “If 30% of your portfolio is in one industry and that one industry is being impacted by technology, you have not been a good risk manager,” he said, according to Business Insider. Likewise, Blue Owl’s co-head of tech investing Erik Bissonnette said at a May earnings call that the firm anticipates “tempered” software deal activity “as the market recalibrates to current dynamics.” The firm also highlighted the opportunity to “revisit adjacent technology areas” that have always been in focus for it, such as digital infrastructure and life sciences, where it expects to “generate attractive, less correlated returns over time.” Apollo, HPS and Blue Owl declined to comment. Blackstone didn’t immediately reply to a request for comment. PitchBook LCD reported in February that the majority of the firm’s software loans were in areas more insulated from AI risk. Higher borrowing costs Sponsors hungry for financing can still find it, from a select group of private credit funds and commercial banks that remain active in the market. Borrowing costs have inevitably climbed because of a shrinking pool of available lenders. Existing lenders have also grown more cautious, tightening due diligence and structuring deals with stricter terms and lower leverage. Credit spreads on the best software deals had been hovering around 400 to 450 basis points over the benchmark rate. Now lenders are pricing those same deals at 550 to 650 basis points, according to people familiar with the market. In some cases, spreads have blown out to 800 basis points. The widening spreads are also reshaping how deals are financed. Debt now often accounts for 40% to 45% of the purchase price on buyout deals—down from a standard 60% in prior years, said Paul Braswell, an M&A counsel at Texas-based FBFK Law, where he advises both sides of the deal table. To bridge the gap, some PE firms have financed the remainder in a three-way split: A buyer would write an equity check, ask the seller to reinvest a slice of its proceeds back into the business and invite its LPs to contribute cash in the form of preferred equity investments. The pullback has opened the door for smaller managers to win deals that might once have gone to larger lenders. Jeffrey Diehl, managing partner and head of investments at Adams Street Partners, said that the competition for new lending business has noticeably eased across the board, with the strain of software lending only part of the story. “Reducing new deal commitments is a prudent way to ensure BDCs have ample liquidity,” he said. “But sponsors need lenders when they need them, so being inactive for any reason could hurt a lender’s standing and market share with sponsors.” Diehl said Adams Street has been “active and eager” to finance sponsor-backed deals. He did not say if the firm was eager to back software deals specifically. Lenders that are said to have remained active in software lending include Barings and venture debt lender Hercules Capital, according to the banker and the private credit lawyer. However, some existing lenders have become more selective, requiring the borrower to be EBITDA-positive, effectively shutting the door on unprofitable SaaS companies seeking financing, a business that had once thrived in the private credit market, the people said. The pressure that has chilled software lending is not coming from individual investors alone; institutional LPs have also fretted over their managers’ software exposure. Some private credit fund managers have been “roasted” by LPs who have seen that a new software loan was being made. “LPs will get very upset and call their investment staff that they are not happy with it,” said a private credit lawyer. This article originally appeared on PitchBook News

Comments

You must be logged in to comment.