yahoo Press

Barclays Just Upgraded Oscar Health Stock. Here's Why.

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

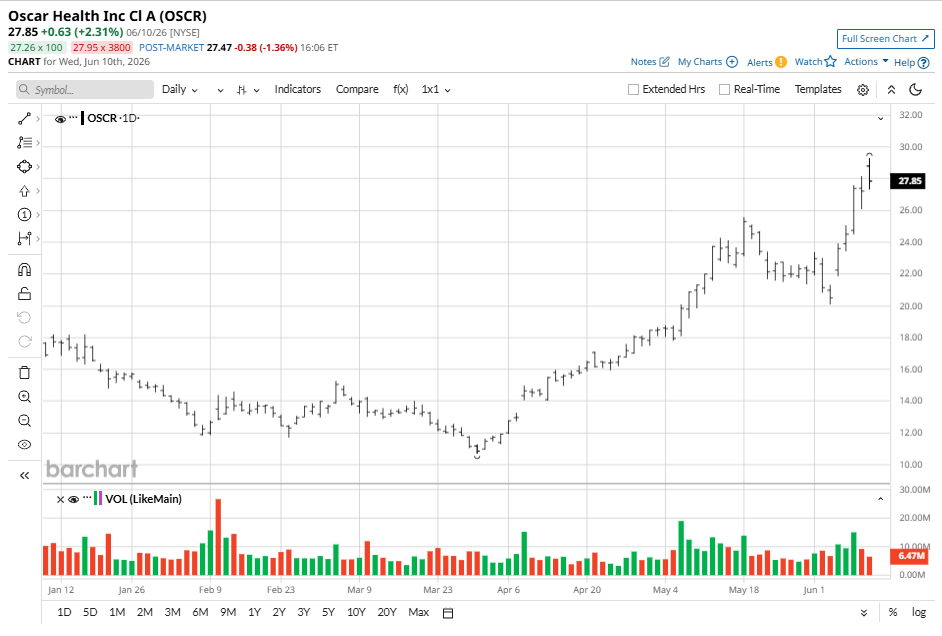

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Oscar Health (OSCR) stock is pushing higher on Wednesday after Barclays’ senior analyst Andrew Mok issued a bullish note in favor of the health insurance company. In his research note, Mok upgraded OSCR to “Overweight” and raised his price objective to $35, indicating potential for another 25% rally from current levels. Dear Marvell Technology Stock Fans, Mark Your Calendars for June 22 Quantum Computing Looks Like Nvidia in 2019. This Could Be the Generational Buy of the Decade. Oracle Earnings Could Reveal a Massive $100 Billion Spending Surge. Here Is Why You Should Still Buy ORCL Stock. Our exclusive Barchart Brief newsletter is your FREE midday guide to what's moving stocks, sectors, and investor sentiment - delivered right when you need the info most. Subscribe today! Barclays’ bullish call is particularly significant given Oscar Health shares are already up an exciting 160% versus their low in late March. Mok’s constructive view is rooted in a valuation disconnect between OSCR stock and its peers. The company offers “single-line exposure” to the high-growth Individual Affordable Care Act (ACA) marketplace; yet it’s trading at just 11.5x earnings — roughly half the multiple on Alignment Health Care. However, “as investor preferences potentially shift toward the AC, we believe a narrowing of this valuation gap is warranted,” the Barclays analyst told clients. Note that Barchart also currently holds an “88% BUY” opinion on Oscar Health, reinforcing that the technical momentum is increasingly turning in its favor for the back half of 2026. According to Andrew Mok, Wall Street’s longer-term estimates for Oscar Health stock are too conservative. Analysts' consensus for the firm’s 2028 earnings per share (EPS) implies a meager 3% EBIT margin currently, a substantial 200 basis points below management’s own long-term target of 5%. This leaves significant room for upward revisions as the year unfolds, the Barclays analyst wrote. All in all, with proactive repricing strategies taking hold across the industry and early data hinting at highly favorable market health risks, Mok expects margin to recover sharply, potentially driving OSCR higher over time. Investors should note, however, that not all analysts are as bullish on Oscar Health as Barclays for the next 12 months. According to Barchart, the consensus rating on OSCR shares is “Hold," with the mean price target of just over $22 indicating a potential downside of about 20% from current levels. And the NYSE-listed firm doesn’t currently pay a dividend to appear any more attractive as a long-term holding, either. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.