yahoo Press

LULU Stock Falls After Lululemon Cuts Annual Guidance

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

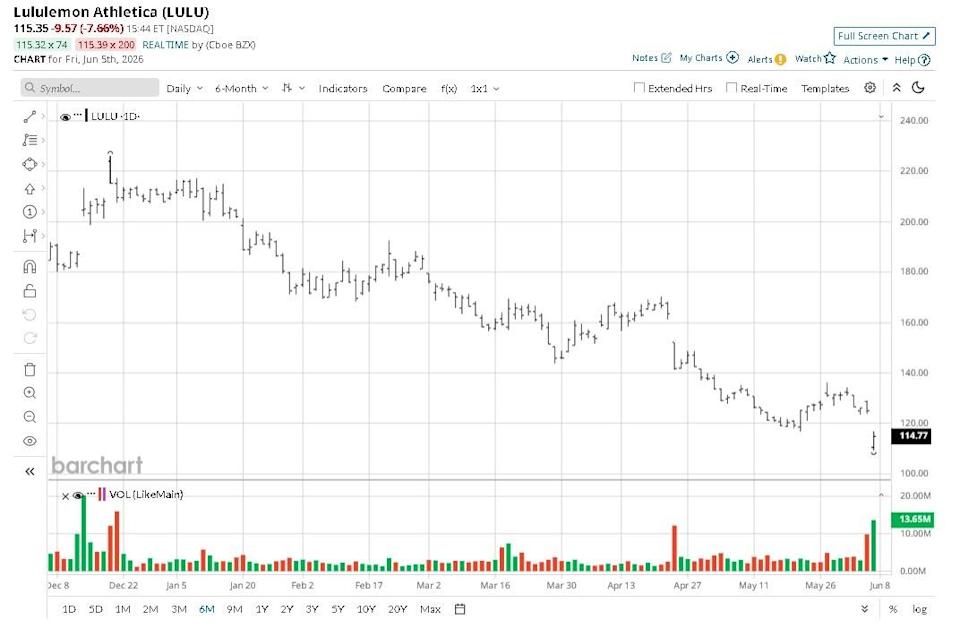

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Lululemon Athletica (LULU) stock tumbled on Friday after the athletic apparel retailer reported a better-than-expected Q1 but lowered its full-year guidance. In the earnings release, management said the firm’s core North American market is contracting, with mounting reliance on discounting beginning to erode the premium brand image. Dear Micron Stock Fans, Mark Your Calendars for June 24 Has Micron Stock Peaked Here? Its Future Valuation Metric May Surprise the Market Why 1 Veteran Analyst Doubled Her Micron Stock Price Target for 2026 Markets move fast. Keep up by reading our FREE midday Barchart Brief newsletter for exclusive charts, analysis, and headlines. Versus the start of this year, Lululemon shares are now down about 45%. Vancouver-headquartered Lululemon Athletica reduced its fiscal 2026 outlook to $11.07 billion in revenue on $11.05 in earnings per share (EPS). On the earnings call, interim chief executive Meghan Frank cited negative media commentary and product launches that failed to resonate with shoppers for the disappointing guidance. On June 5, investors bailed on LULU shares also because the company’s gross margins contracted 410 basis points in the first quarter to 54.2%, largely reflecting tariff-related pressures. Lululemon’s proxy contest with founder Chip Wilson also weighed materially on Q1 sales, Frank added. Note that LULU now sits handily below its major moving averages (MAs), with an RSI in the late 20s indicating intense selling pressure, unlikely to subside without a meaningful catalyst. Following the quarterly release, Freedom Broker analyst Georgy Vashchenko upgraded Lululemon shares to “Hold”, but slashed his price target aggressively from $320 to $139 only. In his research note, Vashchenko admitted that the investment thesis has materially deteriorated as he downwardly revised profit and revenue estimates to align with management’s lowered guidance. Investors should also note that Barchart currently holds a “100% SELL” opinion on LULU, which reinforces that technical momentum favors continued weakness ahead. In short, the company’s Q1 print suggests it’s trapped in a phase where fundamentals continue to deteriorate amid fierce competition and weakening pricing power. And it’s not like Lululemon pays a dividend to incentivize ownership despite weakening financials. Heading into Friday, Wall Street had a consensus “Hold” rating on LULU stock with a mean price target of about $177. However, it’s fair to assume that downward revisions similar to Freedom Broker’s will follow after the Canadian firm’s broadly disappointing commentary on the earnings call last night. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.