yahoo Press

HPE Stock Alert: Hewlett Packard Skyrockets Following Q2 Results

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

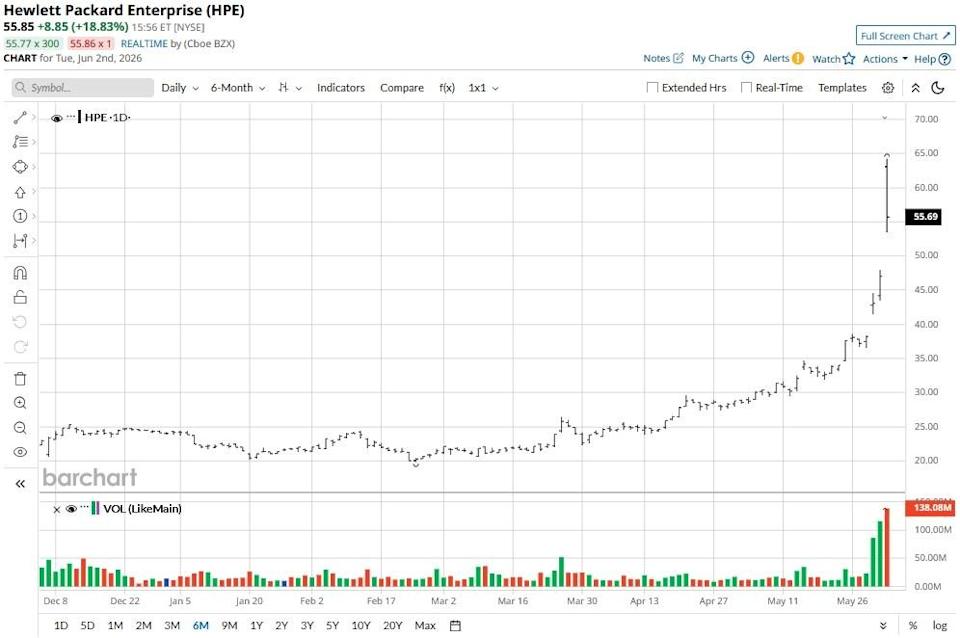

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Investors are cheering Hewlett Packard Enterprise (HPE) this morning after the AI server specialist posted record financials for its Q2 and issued upbeat guidance for the full year. Including post-earnings gains, HPE stock is up a remarkable 180% versus its year-to-date low, but Ananda Baruah, a senior Loop Capital analyst, believes it’s not out of room to run just yet. Investors Bearish on Oracle Ahead of Earnings - Unusually Heavy ORCL Put Options Trading Salesforce vs. ServiceNow: 1 AI Giant Is Leaving the Other Behind Microsoft Stock Is Up Nearly 30% From Its March Lows, But You Shouldn’t Sell MSFT Just Yet Our exclusive Barchart Brief newsletter is your FREE midday guide to what's moving stocks, sectors, and investor sentiment - delivered right when you need the info most. Subscribe today! On Tuesday, he upgraded Hewlett Packard Enterprise to “Buy” and raised the price target to $75, signaling potential upside of another 37% from current levels. In its recently concluded quarter, Hewlett Packard Enterprise earned $0.79 on a per-share basis and generated $10.68 billion in revenue, both handily above Street estimates. Citing AI-driven networking demand, the company raised its full-year guidance for revenue growth as well to at least 29%, which formed the basis of Loop Capital’s bullish call on HPE shares. According to Ananda Baruah, “Agentic and Inferencing adoption” is helping drive both sales and margin upside for HPE; the firm’s gross margin (adjusted) increased by 750 bps year-over-year to 36.9%. A 1.03% dividend yield on Hewlett Packard shares makes them even more attractive for income-focused investors. Baruah is convinced that “commercial inference investment” is currently in its early innings only, offering HPE’s server business a three-to-five year runway for sustained, AI-driven growth. He also expects the company’s recent Juniper Networks acquisition to supercharge its networking scale and deepen its exposure to AI‑driven data‑center spend. What’s also worth mentioning is that HPE shares are trading at about 22x forward earnings at the time of writing. So they’re much cheaper to own than Dell (DELL) at nearly 35x. Barchart also currently holds a “100% Buy” opinion on Hewlett Packard Enterprise, reinforcing that the technical momentum favors continued upside ahead. Heading into Tuesday, Wall Street analysts had a consensus “Moderate Buy” rating on Hewlett Packard stock, with price targets going as high as $40. However, it’s reasonable to expect upward revisions in the days ahead now that HPE has posted a blockbuster Q2 and issued impressive future guidance. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.