yahoo Press

Eurazeo raises $4.5B as European private credit capital pools at the top

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

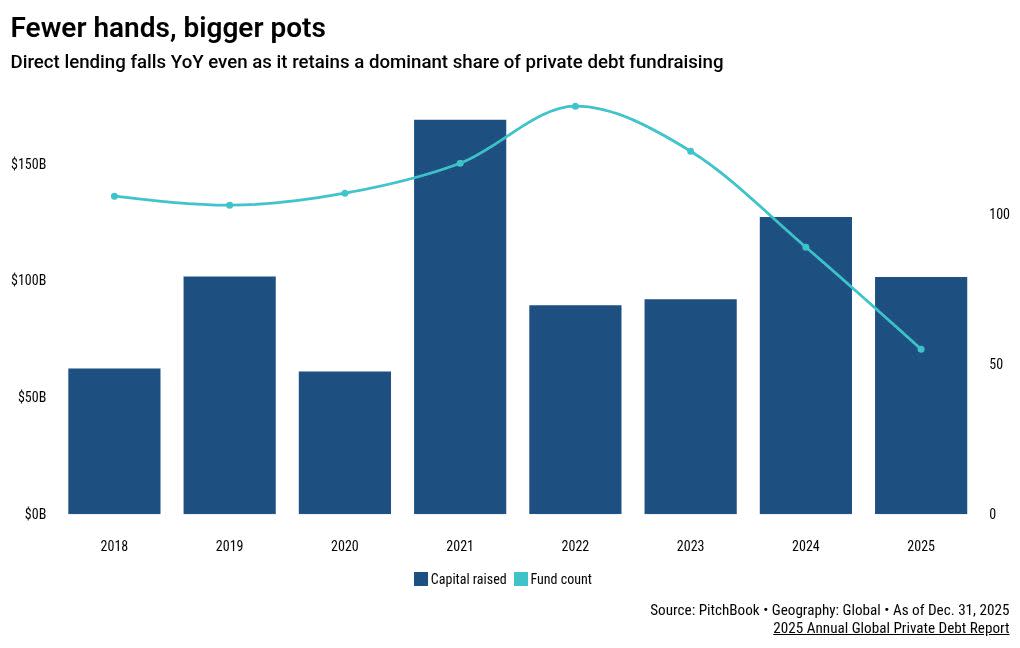

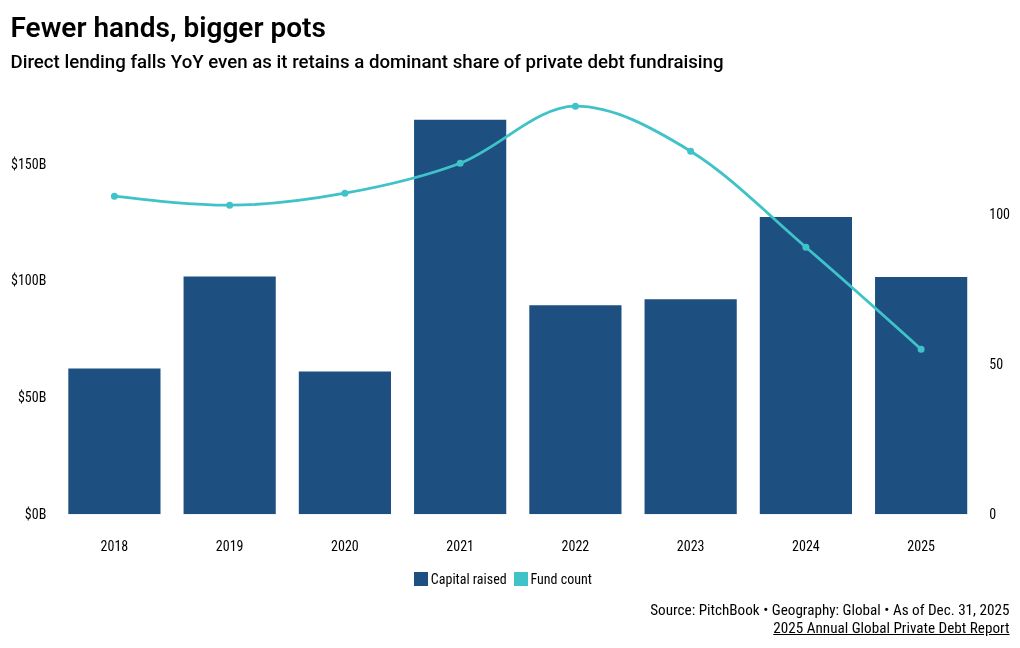

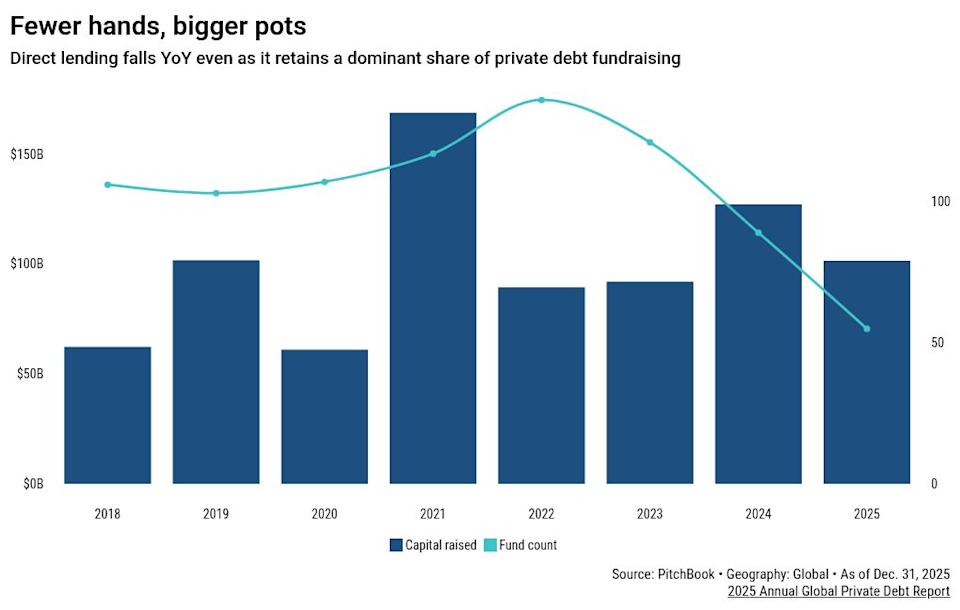

French asset manager Eurazeo has closed its biggest direct lending fund yet at €3.9 billion (about $4.5 billion), beating its target by almost a third—making it one of a handful of European credit managers raising capital in a tough market. Eurazeo Private Debt VII, which focuses on lending to lower mid-market companies across Europe, attracted total commitments of €5.5 billion, including separately managed accounts and private wealth capital. International investors account for more than 60% of commitments, with North American and Asian LPs among the most active, the firm said. The close comes at a difficult moment for global private debt fundraising. PitchBook’s 2025 Annual Global Private Debt Report shows that 55 direct lending funds reached a final close in 2025, raising a combined $101.7 billion—a year-on-year decline in both fund count and capital raised, even as direct lending retained its dominant share of private debt fundraising. This article appeared as part of The Europe Pitch newsletter. Sign up here More broadly, private debt saw its third consecutive year of declining fund count, even as total capital raised held broadly steady at around $221 billion. Furthermore, 93% of all private debt capital raised in 2025 went to experienced managers—those on their fourth fund or later—a record share. The same report also showed that European private debt funds raised $79.4 billion in 2025—but strip out the two largest closes, by Ares Management and CVC Capital Partners, and the region’s share of global fundraising falls back in line with historical norms, according to PitchBook data. For Eurazeo, EPD VII represents a significant step up, being roughly 1.7x the size of its 2023 predecessor, in line with the average step-up of 1.5x recorded across European mid-market fund closes in Q1 2026, according to PitchBook’s Q1 2026 European PE Breakdown. The fund is already 65% deployed across more than 70 companies; however, the broader private credit deployment environment is more complicated. PitchBook LCD data shows that spreads on European direct lending deals have barely moved, averaging 509 basis points in the 12 months to April 2026—slightly below the full-year 2025 reading of 522 bps—even as US spreads have widened by 50-100bps. Tighter pricing reflects intense competition, with larger direct lenders pushed down the size ladder as a resurgent, broadly syndicated loan market takes back large-cap deals. This article originally appeared on PitchBook News

Comments

You must be logged in to comment.