yahoo Press

PE-backed companies are losing their direct lending dominance

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

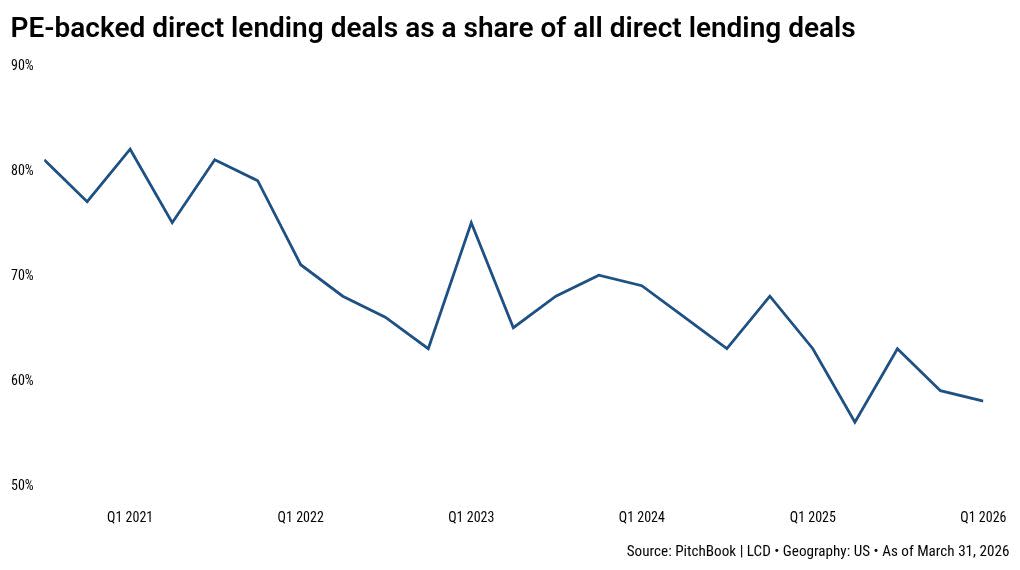

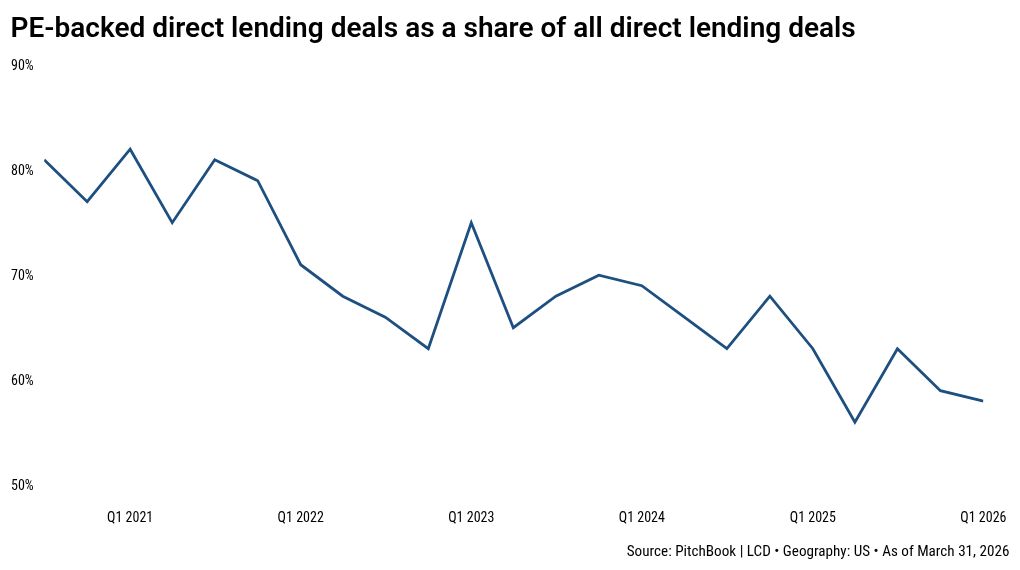

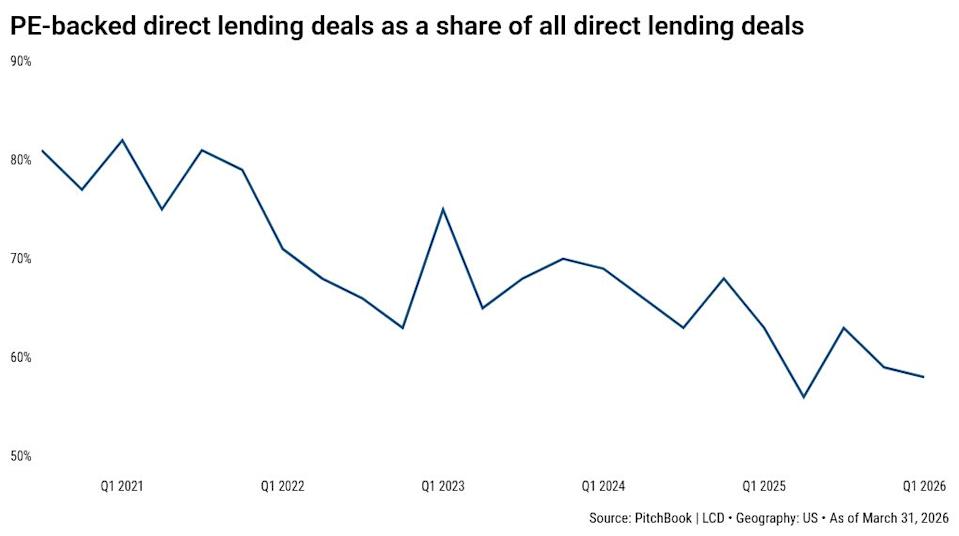

The massive growth of the US direct lending market was driven by one group of borrowers: PE-owned businesses. Their market share, however, has been shrinking for years. PE-backed companies accounted for roughly 6 in 10 US direct-lending deals in Q1, according to PitchBook LCD data, down from more than 8 in 10 during the post-pandemic deal boom. For a market built around sponsor finance, the shift reads as if lenders are increasingly backing founder- and management-owned businesses, pulling away from PE middlemen and their problems since interest rates went up in 2022. But the details live in the fine print. Looking at cumulative value rather than loan count shows a changing mix of deals getting done, not necessarily a collapse in lenders’ appetite for sponsor-backed credit. “The 60% right now is really being driven, not because there’s a lot of activity in non-sponsored—it’s because there’s not enough activity in sponsored,” said Dianna Carr-Coletta, managing director in the private credit team at $1.5 trillion asset manager PGIM. That distinction matters. In the PitchBook LCD data, PE-backed borrowers accounted for 121 direct-lending deals in the first quarter, or 57.9% of the total captured in the dataset. US direct-lending deal count across all types of borrowers fell to 209 in Q1 from 226 a year earlier, but estimated volume rose to $73.5 billion total from $58.2 billion. Loans used to finance leveraged buyouts, which are directly tied to dealmaking by PE sponsors, dropped to 53 from 63 while estimated volume climbed to $23.3 billion from $17.4 billion. That suggests the market was not shutting off sponsor financing, instead doing fewer transactions, some of them larger, while the buyout engine runs below speed. The sponsor slowdown has been building for years. Buyout firms are still contending with a backlog of aging portfolio companies, slower exits and limited distributions to investors. In the US, the share of PE-backed companies held for more than seven years is reaching levels last seen around the time of the global financial crisis, according to PitchBook’s latest Quantitative Perspectives report. This has weighed on new LBO formation, the engine that historically kept direct-lending pipelines full. Financing data tells the story more directly. Only 44% of US direct-lending loans backed leveraged buyouts in 2025, down from 61% in 2021, according to PitchBook LCD’s 2026 US Credit Markets Outlook. In Q1, LBO financing slowed to its weakest pace since Q3 2023, even as refinancings, dividend recapitalizations and add-on acquisitions kept private credit capital moving. For direct lenders, that creates a numerator problem. Sponsor-backed deal count has fallen because sponsors are not bringing enough new transactions to market. At the same time, the denominator is expanding as lenders look more seriously at non-sponsored borrowers. Non-sponsored lending remains small compared with sponsor finance, but it is becoming more mainstream. Family-owned and founder-led companies have historically relied on commercial banks. Now, some are turning to private credit as lenders try to diversify origination away from PE sponsors. Carr-Coletta said PGIM’s middle-market direct-lending strategy is currently about 75% sponsor-backed and 25% non-sponsored. Over time, she said, the non-sponsored share could rise toward 35% or 40%. But that shift is likely to be gradual. The obstacle is origination. Sponsor-backed lending is efficient because PE firms are repeat borrowers. A sponsor may bring the same lender multiple deals across its portfolio companies and funds. Non-sponsored lending is more fragmented. It requires direct relationships with private businesses that may borrow episodically and have no standing relationship with private credit managers. There has been a wave of partnerships in recent years to combine a bank’s relationships with an asset manager’s financial firepower. Citi and Apollo Global Management announced a $25 billion private credit and direct-lending program in 2024 designed to serve corporate and sponsor clients. Citi later followed with a €15 billion partnership with BlackRock’s HPS Investment Partners across Europe, the Middle East and Africa. And PNC and TCW launched a $2.5 billion platform targeting both sponsored and non-sponsored middle-market companies. Wells Fargo has also built a private-credit partnership with Centerbridge Partners through its Overland platform. The shift does not mean private credit has outgrown private equity. But it is a sign of the direction of travel. This article originally appeared on PitchBook News

Comments

You must be logged in to comment.