yahoo Press

US 30-Year Yield Hits Highest Since 2007 as Selloff Deepens

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

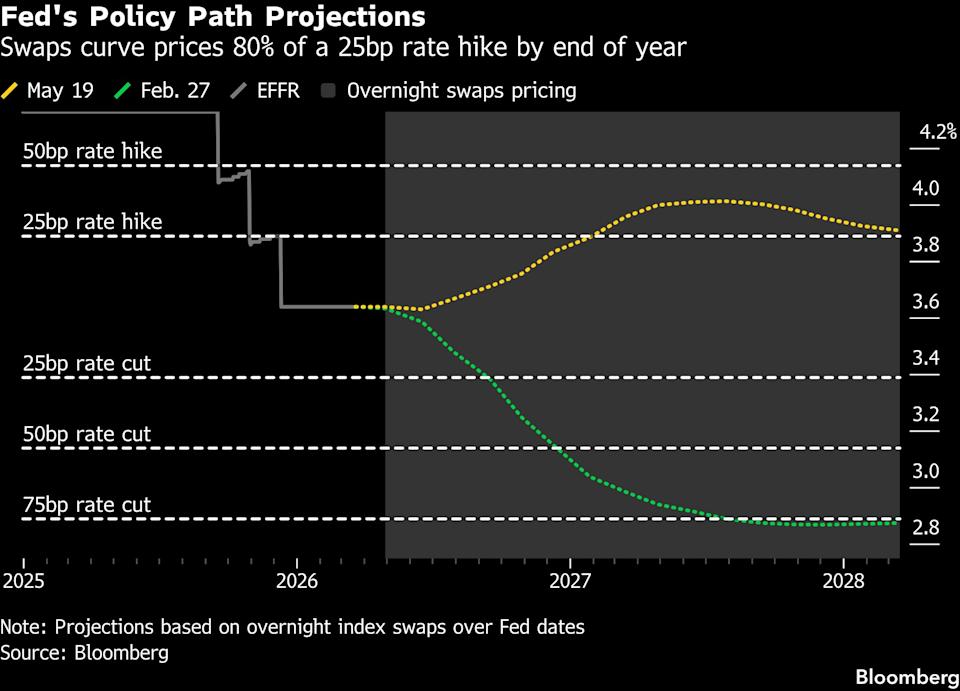

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. (Bloomberg) -- Yields on the US Treasury’s longest-dated bond rose to the highest level in almost two decades as investor concerns mount that accelerating inflation will force central bankers to raise interest rates. Most Read from Bloomberg US Lawmakers Plan New $130 Fee for Electric Vehicle Owners NATO Is Starting to Consider Hormuz Mission to Protect Ships US 30-Year Yield Hits Highest Since 2007 as Selloff Deepens Billionaire Rinehart Bets $100 Million on US Defense Stocks Hasbro Cancels Dungeons & Dragons Game From ‘Star Wars’ Veteran The 30-year yield rose as much as seven basis points to 5.20% on Tuesday, a level last seen in 2007, on the eve of the global financial crisis. Bond markets across Europe and Japan also fell, while the selloff spilled over into US equity markets. Yields on government bonds have surged globally in recent weeks as a jump in energy prices caused by the Iran war adds to inflation fears, pushing traders to bet the Federal Reserve will hike rates as soon as this year. Mounting deficits are also prompting investors to demand greater compensation to own longer-maturity debt. “The bond market is pricing in a higher-for-longer rate policy, most visible in the long end of the curve where duration sensitivity is the greatest,” said Liz Templeton, a senior product manager at Morningstar. That reflects “ongoing uncertainty around Fed policy, energy-driven cost pressures, and heavier Treasury issuance.” Persistently higher yields threaten to slow the US economy, which has so far proved resilient, and lift borrowing costs for US home buyers and corporations. That prospect is fueling speculation about a policy response by US officials, who already have shifted debt issuance toward shorter-dated maturities. Worryingly for bondholders, Tuesday’s selloff was not driven by a surge in oil prices — which crept lower on the day — or any individual catalyst. That speaks to a broader nervousness in the market as investors reappraise the clearing price for debt. US 10-year Treasury yields rose as much as 10 basis points to 4.69%, the highest since early 2025, before the move pared to around 4.66%. Heavy trading in Treasury futures helped drive the move, particularly in contracts tied to five- and 10-year notes. Investors placed several sizable block trades as yields kept rising, and trading volume in the 10-year futures contract during the morning session in New York was nearly twice the recent average. The shift in market sentiment will soon confront incoming Federal Reserve Chair Kevin Warsh. Traders anticipate the Fed’s next move will be a rate increase, potentially as soon as the end of this year. When the Iran war began in late February, they anticipated as many as three Fed cuts in 2026. “The market has swung to a clear hiking bias,” said Benjamin Schroeder, a senior rates strategist at ING. That’s because investors are “worried about energy price pressures morphing into something more than just a short-lived inflationary episode.” Line in the Sand The 5% level for 30-year US yields has been considered a “line in the sand” that would spark dip-buying by some investors. The recent moves are challenging that assumption, potentially signaling a new era for the $31 trillion Treasury market, widely considered the premier safe asset and a barometer for borrowing costs around the world. Barclays Plc and Citigroup Inc. strategists have warned clients that yields may breach 5.5%, levels last seen in 2004. And the head of BlackRock’s research unit is recommending investors reduce their exposure to developed-market government bonds — including Treasuries — in favor of equities. “With debt rising faster than growth, worsening inflation profiles, and no political will for fiscal reform, there is little reason to reach for the long end,” said Ajay Rajadhyaksha, Barclays Plc’s global chairman of research. A similar dynamic is playing out globally, with yields on 30-year UK gilts approaching 6% and Germany’s long-term borrowing rate trading at a 2011 high. In the US, it’s already feeding through to government financing costs. A mid-May auction of 30-year Treasuries was the first since 2007 to result in an interest rate of at least 5%. Investor demand was unremarkable, even at that level. US Treasury Secretary Scott Bessent has committed to bringing down borrowing costs at a time when investor concerns over the debt level persist. The median budget deficit estimate of primary dealers of US Treasury securities released earlier this month showed a $1.95 trillion gap for the year ending in September and further widening to $2 trillion in 2027. “Yields are not just pricing inflation volatility, but increasingly the return of fiscal risk,” said Laura Cooper, global investment strategist and head of macro credit at Nuveen. “There is limited capacity for bond markets to absorb the spending at current yield levels without demanding additional compensation.” It also might cause investors in other asset classes to rethink their allocations, insofar as they can earn a higher return by investing in government bonds. The S&P 500 stock index has soared over 7% this year, weathering the selloff in most bond markets. On Tuesday, the Russell 2000 Index, comprised of smaller companies that typically carry higher debt loads and are less profitable than their larger counterparts, was down about 1% by the end of the trading session, widening its three-day decline to 4%. The S&P 500 and Nasdaq 100 indexes also fell. “The ability of US equities to withstand the current bearish move in Treasuries is the true litmus test of the bond selloff,” said Ian Lyngen, head of US interest-rate strategy at BMO Capital Markets in New York. “We suspect that if and when 30-year rates manage to reach 5.25% in the next few weeks, there will be a more durable pullback in equity valuations.” What Bloomberg Strategists say... “On a day where oil prices are lower on Mideast peace negotiation hopes, it’s notable that US Treasuries are selling off. It’s an indication that confusion over policy and inflation outcomes will keep bonds under pressure, particularly via inflation expectations.” — Edward Harrison, Macro Strategist, Markets Live For the full analysis, click here. --With assistance from Michael MacKenzie and Edward Bolingbroke. (Updates prices, adds context from sixth paragraph.) Most Read from Bloomberg Businessweek College Kids Don’t Want Your AI The AI Boom Is a Dilemma for Retail Investors Elon Musk Really Needs Starship to Work This Time Behind the Claude Frenzy That Ate Up All the Mac Minis Can AI Drug Development Live Up to the Hype? ©2026 Bloomberg L.P.

Comments

You must be logged in to comment.