yahoo Press

As market enters post SaaS-pocalypse thaw, leveraged loan repricing window opens (for some borrowers)

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

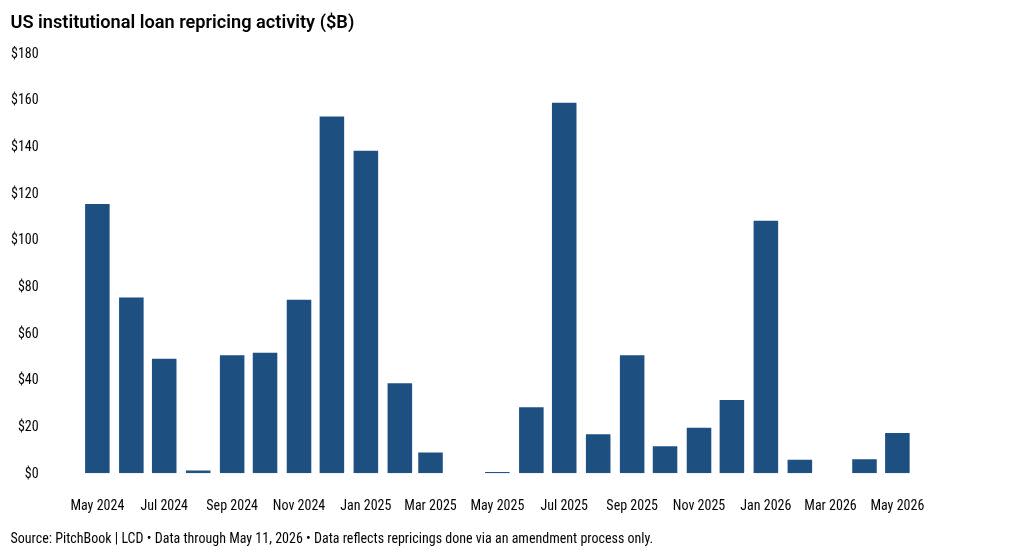

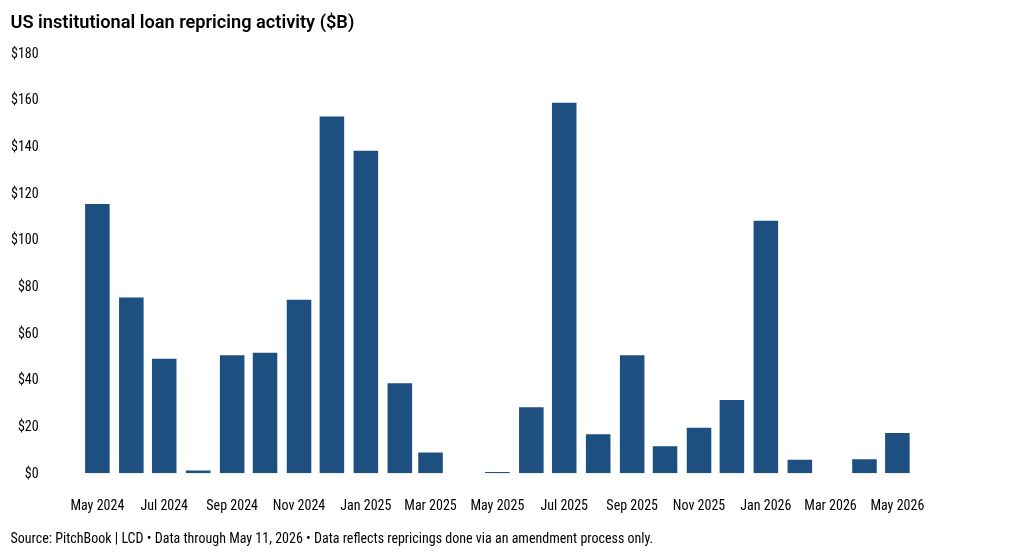

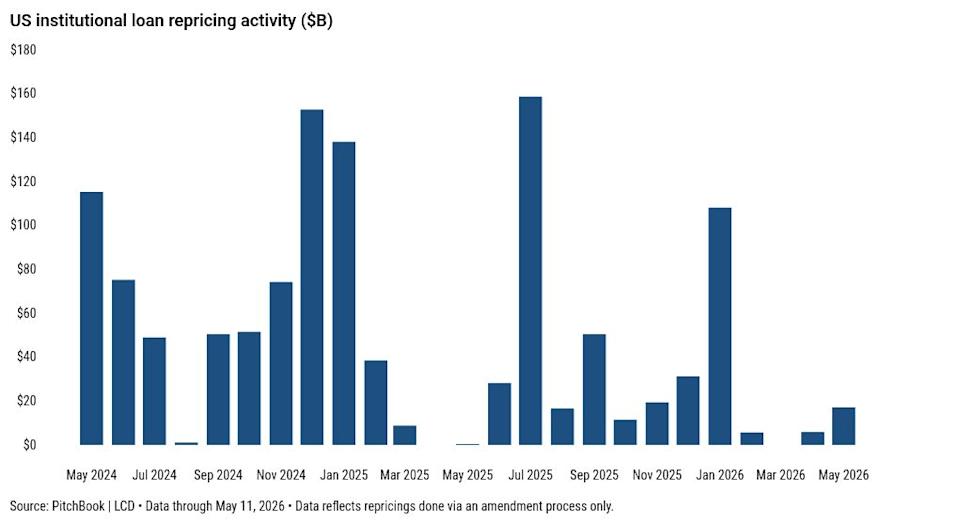

The repricing market is open again, but not for everyone. Double-B rated borrowers are leading the charge, with their share of loans priced at par or above back at January peaks, as single-Bs and tech credits remain largely sidelined. Seven speculative-grade borrowers launched spread-lowering amendments on May 11, the busiest day for such activity since Jan. 26 — a day that served as the exclamation point to one of the most active repricing months on record. January featured $108 billion in repricing activity before a secondary market selloff brought the market to a virtual standstill for three months. The May 11 activity pushed month-to-date repricing volume to $17.2 billion, already eclipsing the $11.8 billion launched across February, March, and April combined. However, volume is still well short of the heights during the 2024-2025 repricing wave. At its peak, that cycle averaged $52.5 billion per month as 632 borrowers repriced their facilities. For context, that translates to 57% of all borrowers with loans outstanding at year-end 2024, per the Morningstar LSTA US Leveraged Loan Index. A recovery in secondary prices is pulling opportunistic deal flow back into the market, though unevenly — higher-rated borrowers and those with limited AI disruption exposure are leading the way as investors draw sharper distinctions between credits. The LLI weighted average bid reached 95.40 by May 8, recovering to mid-February levels and recouping 123 bps from the early-March low of 94.17. Improving sentiment also drove a sharp recovery in the share of loans priced at par or above, a widely watched gauge of investor demand, with the gains most pronounced among higher-rated issuers. For double-B-minus borrowers, that share surged to 76% by May 11, matching the mid-January peak and up sharply from 59% at the end of April and just 13% at the end of March. B-plus and B-flat borrowers saw meaningful improvement as well, with the par-plus shares rising to 54% and 47%, respectively, from 45% and 39% at the end of April. The recovery was far more muted at the lower end of the credit spectrum, however, with the B-minus cohort edging up to just 18% from 16%, reflecting lingering investor caution. Double-B rated borrowers have dominated repricing activity in May, accounting for 11 of the 15 deals tracked, or 73%. The contrast with January is striking: that month, LCD tracked 17 BB-minus repricings, but they represented just 23% of a far larger overall market. Double-B activity, particularly among corporate borrowers, is running at a January-like pace, as sponsor-backed single-B borrowers remain largely sidelined. Green shoots are starting to appear, though. On May 7, Shermco, a provider of electrical system maintenance, repair, testing, and engineering & design services, launched a repricing of its $550 million covenant-lite first-lien term loan due October 2032. Price talk is S+250-275, versus S+325 on the existing facility issued in October 2025 to back Blackstone’s buyout of the company. Current corporate and facility ratings are B-/B3, with stable outlooks. This is the first sponsor-backed borrower with a B-minus rating by both S&P Global and Moody’s to launch a repricing since late January. Investors are becoming more comfortable taking risk in the primary market, and borrowers are making the most of it. Multiple borrowers either accelerated deals already in the market, upsized them, or tightened pricing last week. $47 billion in play While recovering secondary prices are creating a more permissive backdrop for repricings, the opportunity set is far more constrained than it appeared earlier this year. New-issue spreads remain roughly 50 basis points wide of January levels for both double-Bs and single-Bs, and the deal mix looks meaningfully different, skewing toward corporates from defensive industries. The tech sector has not produced a single spread-lowering amendment since January, a reflection of how sharply risk has been repriced in that space. With softer investor demand for both tech credits and sponsor-backed single-B borrowers, the two segments with the heaviest representation in the leveraged loan market, the pipeline of viable repricing candidates is materially narrower than it was heading into the year. Based on LCD’s analysis, potential repricing targets in the US totaled $47.2 billion as of May 8, as tracked by the Morningstar LSTA US Leveraged Loan Index. This cohort consists of currently outstanding first-lien term loans that (1) are outside of their prepay protection period, which is typically six months, (2) have a bid price of par or higher, and (3) have a current spread at least 25 bps higher than the three-month average for new-issue loans with the same corporate credit rating by S&P Global. Including loans with call protection that expire in the next three months, the repricing target estimate grows by roughly $4 billion. Should secondary prices continue to rise, the pool of potential repricing targets will grow further, assuming new-issue spreads remain near current levels. The index includes another $10.3 billion of loans priced between 99.75 and 99.99 with an expired prepay fee period and higher-than-average spreads for the comparable ratings categories. Another $8.6 billion currently sits between 99.50 and 99.74, so collectively, LCD estimates that about $19 billion of loans are within 50 bps of becoming potential repricing targets. Adding these cohorts together suggests that the repricing opportunity could approach $70 billion, assuming spreads remain at current levels and secondary prices continue to recover. Matching the 2024-2025 repricing wave remains a distant prospect. Until investor appetite for tech credits and sponsor-backed single-Bs recovers in a meaningful way, the market is likely to remain a high-quality, corporate-led affair — active but operating well below its recent highs. Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe Featured image by General_4530/Getty Images This article originally appeared on PitchBook News Featured image by General_4530/Getty Images

Comments

You must be logged in to comment.