yahoo Press

Mine restarts support West Africa’s gold recovery in 2026

Images

1 / 4

2 / 4

3 / 4

4 / 4

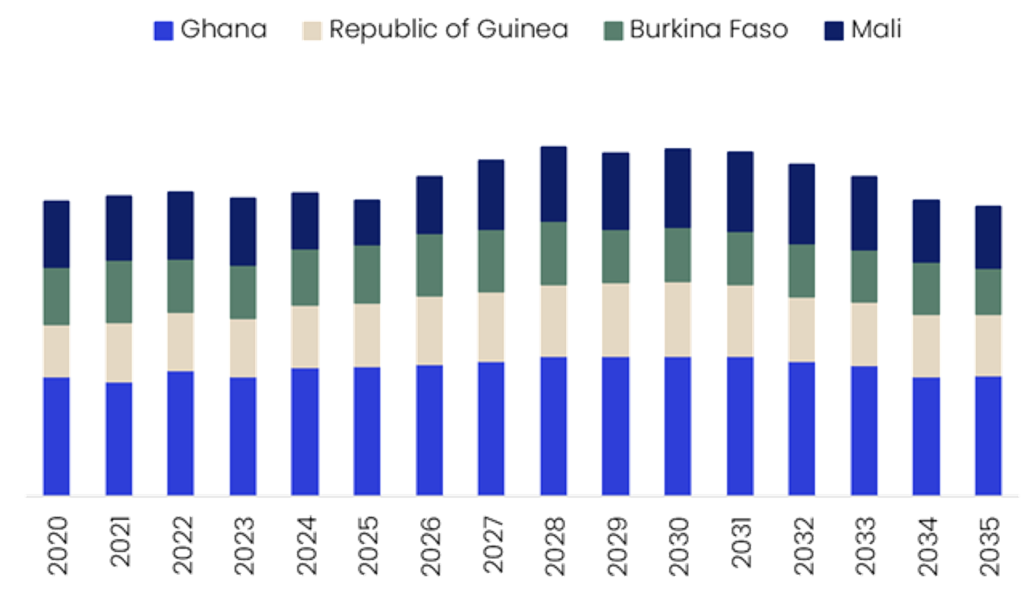

West Africa’s gold sector is entering 2026 with a recovery outlook, but not a uniform growth story. After a weaker 2025, when production across major markets such as Ghana, Mali, Guinea and Burkina Faso declined by 2.4%, output is expected to rebound by 8.0% in 2026. This recovery will be driven mainly by mine restarts, new project ramp-ups and improved operating performance, while risks from security issues, mature mine declines, permitting delays, and policy intervention continue to weigh on the sector. Ghana remains the anchor of West African gold production and continues to be Africa’s largest gold producer in 2025. However, output was broadly flat, up only 0.5% over 2024, as lower grades and operational issues affected key mines such as Ahafo South, Tarkwa and Iduapriem. These pressures were partly offset by stronger output from Obuasi and Akyem, along with the ramp-up of Shandong Gold’s Namdini project. In 2026, Ghana’s production is expected to recover marginally, supported by Newmont’s Ahafo North, which commenced production in October 2025, continued growth from Namdini, higher output from Asante Gold’s Bibiani, and operational improvements at Obuasi. However, Ghana’s outlook is increasingly shaped by policy tightening. The government’s decision in April 2026 not to renew Gold Fields’ Damang lease and to take control of the mine signals a stronger focus on domestic value capture and state oversight. The introduction of a sliding-scale royalty regime also reflects the government’s attempt to benefit more from elevated gold prices. At the same time, Ghana’s move to formalise artisanal and small-scale mining through a centralised gold buying and processing model could improve traceability, reduce illicit trading and strengthen responsible production practices. Despite these reforms, Ghana’s longer-term production outlook remains constrained by declining output from mature assets, including Ahafo South. Mali is expected to be one of the strongest contributors to the region’s 2026 recovery, largely due to the restart and ramp-up of Loulo-Gounkoto. The mine’s disruption in 2025, linked to the dispute over mining conventions and provisional administration, sharply reduced Mali’s output. With operations restarting after the dispute was resolved, Mali’s gold production is forecast to rise significantly by 28% in 2026. Additional support is expected from the Syama Phase I and Fekola Regional projects. However, Mali’s dependence on gold remains a structural risk, as the sector accounts for a major share of GDP, exports and tax revenue. Security risks also remain high, as shown by the January 2026 attack on the Morila gold mine, highlighting the challenges of reviving production in unstable areas. Guinea’s gold sector is also set for a rebound in 2026. Growth will be led by the ramp-up of the Kiniero Gold Mine, which began production in late 2025. Stronger performance at Siguiri will further support the recovery, despite earlier disruptions. Renewed investor interest, including potential partnerships around the Poura Gold Mine project, also points to Guinea’s growing importance in the regional gold landscape. However, scheduled closures at mines such as Lefa, Kiniero, Tri-K and Kouroussa are expected to weaken production after 2030. In Burkina Faso, near-term growth will be driven by the Kiaka project. After commencing production, Kiaka is expected to provide a stronger full-year contribution in 2026 as open-pit mining and processing activities scale up. This will support a rise in Burkina Faso’s gold output by 7%. However, the country’s longer-term outlook is weaker, with planned closures at Essakane, Bomboré, Yaramoko and Boungou expected to drag production lower after 2026. Outside the region’s largest producers, emerging markets such as the Ivory Coast, Niger, Liberia, Senegal and Sierra Leone are becoming more important. Their collective production is expected to grow by 3.8% in 2026. Ivory Coast is expected to become the third-largest gold producer in West Africa by 2026, surpassing Mali, while Senegal’s outlook will benefit from the Makabingui and Diamba Sud projects and underground expansion at Sabodala-Massawa. "Mine restarts support West Africa’s gold recovery in 2026" was originally created and published by Mining Technology, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.

Comments

You must be logged in to comment.