yahoo Press

Price Prediction: We’re Bullish on Disney as Streaming Surges

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

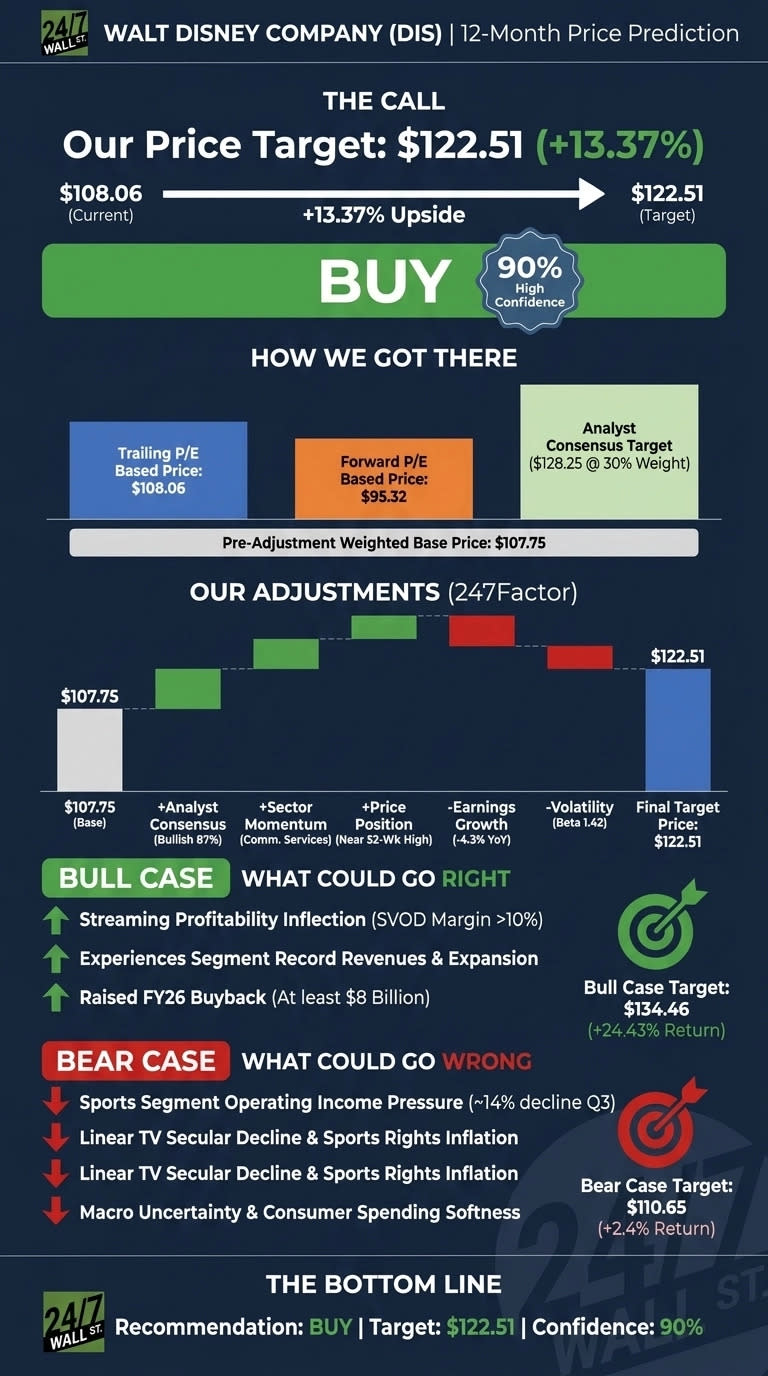

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Disney (DIS) posted fiscal Q2 adjusted EPS of $1.57, beating consensus by 4.98%, with Entertainment SVOD hitting its first 10.6% operating margin and Experiences recording $9.48 billion in revenue with 5% domestic per-capita spending growth. Disney’s streaming margin inflection and Experiences momentum, combined with an $8 billion buyback authorization, support a $122.51 price target implying 13.37% upside as the company shifts from legacy media pressures to growth-driven profitability. The analyst who called NVIDIA in 2010 just named his top 10 stocks and Disney wasn't one of them. Get them here FREE. Our 24/7 Wall St. price target for Disney (NYSE:DIS) is $122.51 over the next 12 months, implying 13.37% upside from the current price of $108.06. We rate Disney a buy with high confidence (90%) following a strong fiscal Q2 earnings report, an inflection in streaming margins, and management's raised buyback. The setup is constructive: shares trade 4% below the 52-week high, sentiment is firming, and FY26 EPS guidance points to double-digit growth. Metric Value Current Price $108.06 24/7 Wall St. Price Target $122.51 Upside 13.37% Recommendation BUY Confidence 90% Disney has rallied 6.67% in the past week and 12.24% in the past month, though shares remain down 5.02% year to date. The analyst who called NVIDIA in 2010 just named his top 10 stocks and Disney wasn't one of them. Get them here FREE. The catalyst was fiscal Q2 2026: adjusted EPS of $1.57 topped consensus by 4.98%, and revenue of $25.16 billion rose 6.55% year over year. Operating income jumped 31.29% to $4.60 billion. Entertainment SVOD posted its first double-digit operating margin (10.6%), with operating income up 88% to $582 million. Experiences delivered record fiscal Q2 revenue of $9.48 billion with domestic per-capita spending up 5%. Bulls focus on three levers. First, streaming: SVOD margin expanded from 8.4% in Q1 2026 to 10.6% in Q2 2026, with 196 million Disney+/Hulu subscribers providing scale. Second, Experiences keeps compounding, with international parks up 11% and capital-light expansions in Abu Dhabi and Japan extending the runway. Third, capital return: management raised the FY26 buyback to at least $8 billion. Wall Street's consensus target of $128.25 reflects 7 Strong Buy and 20 Buy ratings. Our bull-case scenario points to $134.46 within 12 months, a 24.43% total return. Barclays analyst Kannan Venkateshwar raised the firm's price target on Disney to $135 from $130 and keeps an Overweight rating on the shares following the earnings report. Further, Guggenheim analyst Michael Morris raised the firm's price target on Disney to $120 from $115 and keeps a Buy rating on the shares and JPMorgan raised the firm's price target on Disney to $139 from $138 and keeps an Overweight rating on the shares. Net income fell 24.73% year over year in Q2, and Q1 free cash flow swung to -$2.278 billion. Bulls would counter that the cash flow hit reflects deferred California wildfire tax payments, with management reaffirming $19 billion in full-year operating cash flow. Sports remains pressured, with Q3 operating income guided down 14% on higher programming costs, and the NFL deal is $0.03 dilutive to FY26 EPS. Linear TV decline, macro softness, and tariff risk round out the watch list. Our bear case lands at $110.65, essentially flat. The price target of $122.51 backs a buy at 90% confidence. The streaming margin inflection is the factor that tips the scale. The bull thesis strengthens if SVOD margins hold above 10% and Experiences sustains mid-single-digit operating income growth into H2. The thesis weakens if Sports rights inflation widens and consumer spending at parks visibly softens. Year 24/7 Wall St. Price Target 2026 $122.51 2027 $137.04 2028 $149.42 2029 $164.16 2030 $164.97 These projections assume Disney sustains streaming profitability and Experiences momentum. Material upside or downside could come from ESPN DTC scaling and the cadence of sports rights cost inflation. This analyst's 2025 picks are up 106% on average. He just named his top 10 stocks to buy in 2026. Get them here FREE.

Comments

You must be logged in to comment.