yahoo Press

Are Wall Street Analysts Predicting CenterPoint Energy Stock Will Climb or Sink?

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

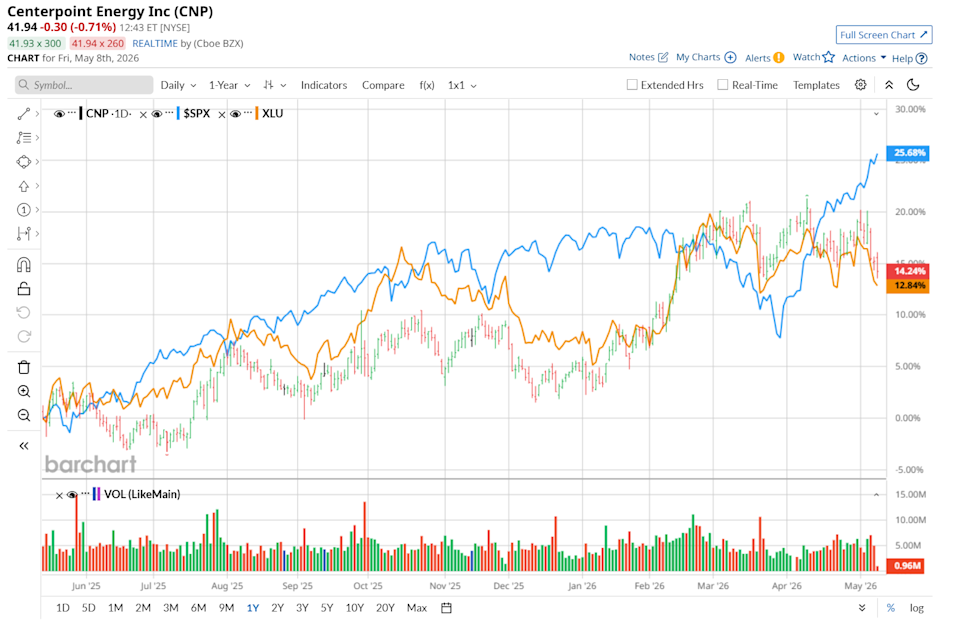

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Houston, Texas-based CenterPoint Energy, Inc. (CNP) provides a comprehensive suite of energy delivery services and infrastructure solutions. Valued at a market cap of $27.6 billion, the company also provides value-added energy management tools like smart thermostats and bill credit programs for grid reliability. This utility company has underperformed the broader market over the past 52 weeks. Shares of CNP have gained 10.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 30.4%. However, on a YTD basis, the stock is up 9.4%, outpacing SPX’s 7.9% rise. As CPUs Steal the Show, AMD Stock Just Got a New Street-High Price Target How Intel Stock Could Be the Biggest Winner from AMD’s Explosive Earnings Win Cathie Wood Dumps More AMD Shares Despite Its Massive 108% Rally. Here's Why. Markets move fast. Keep up by reading our FREE midday Barchart Brief newsletter for exclusive charts, analysis, and headlines. Narrowing the focus, CNP has also lagged the State Street Utilities Select Sector SPDR ETF (XLU), which surged 12.6% over the past 52 weeks. Nonetheless, it has outperformed XLU’s 5.7% YTD uptick. On Apr. 23, shares of CNP surged 2.5% despite posting weaker-than-expected Q1 results. The company posted adjusted EPS of $0.56, up 5.7% year-over-year but below analyst estimates of $0.58. The earnings growth was mainly supported by contributions from business growth and regulatory recovery, which added $0.11 per share compared to the prior-year quarter. However, these gains were partly offset by a $0.02 per share impact from unfavorable weather and usage trends, along with $0.04 per share in higher interest expenses. In addition, a $0.03 unfavorable variance was largely tied to the divestiture of its Louisiana and Mississippi natural gas LDC businesses following the completion of the sale in Q1 2025. For the current fiscal year, ending in December, analysts expect CNP’s EPS to grow 8.5% year over year to $1.91. The company’s earnings surprise history is disappointing. It missed the consensus estimates in three of the last four quarters, while surpassing on another occasion. Among the 18 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on nine “Strong Buy” and nine “Hold” ratings. The configuration is slightly more bullish than a month ago, with eight analysts suggesting a "Strong Buy” rating. On May 4, Evercore Inc. (EVR) maintained an “In Line” rating on CNP and raised its price target to $45, indicating a 7.9% potential upside from the current levels. The mean price target of $46.38 suggests an 11.2% premium to its current price levels, while its Street-high price target of $50 implies a 19.8% potential upside. On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.