yahoo Press

Frenzied pace of high-yield bond issuance continues, fueled by AI

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

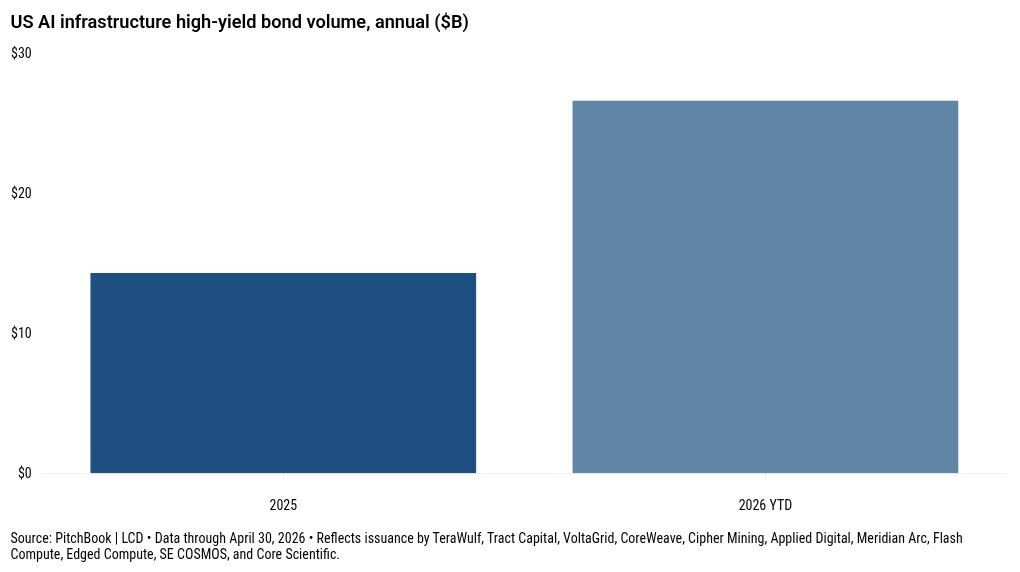

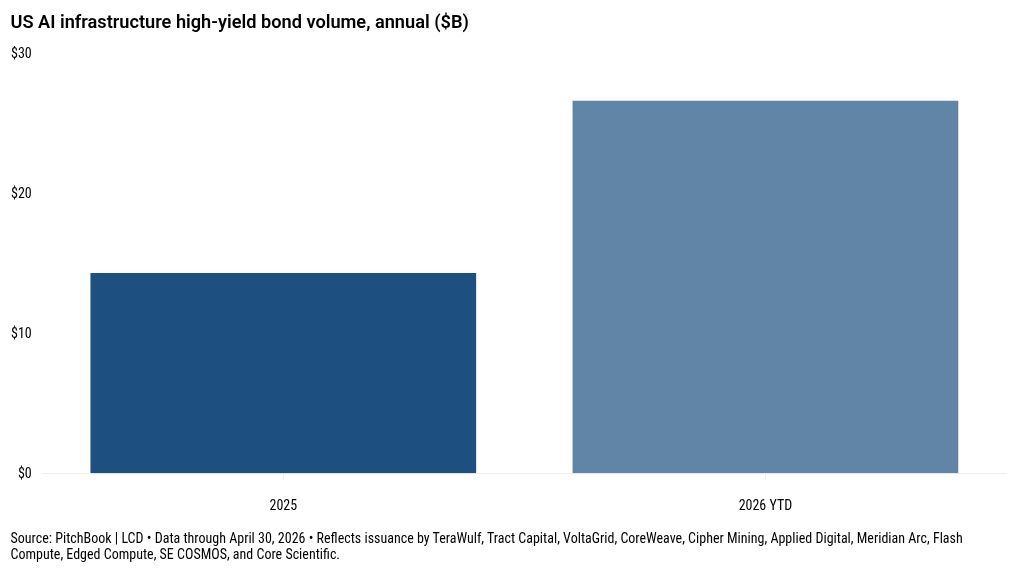

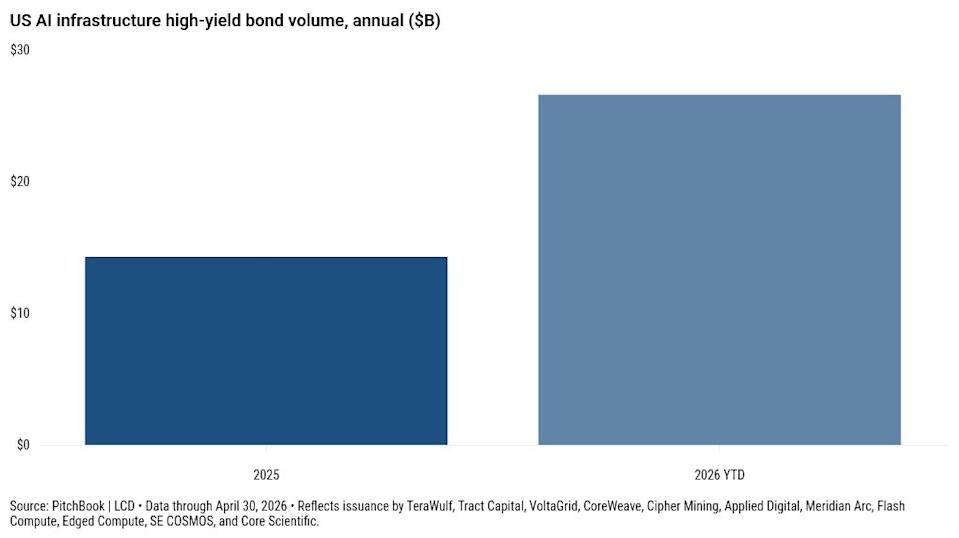

Taps are wide open in the high-yield primary market after an AI-fueled deluge drove $40 billion of April issuance, the most since last September ($55.3 billion) and the second-highest monthly total since the go-go days of 2021. Borrowers are satisfying an array of funding needs, but the AI urgency is palpable. Including April’s jumbo data center deals for Meridian Arc ($5.7 billion), Tract Capital ($4.59 billion), and Core Scientific ($3.3 billion), borrowing on the HY primary for AI infrastructure advanced to $26.6 billion for the year, ahead of most full-year estimates and nearly double the amount issued in all of 2025. At the investment-grade level, the $107 billion of YTD hyperscaler debt already tops last year’s unprecedented $93 billion annual output from the cohort. That’s excluding IG bonds for data centers, including a $4.6 billion deal for QTS Fayetteville on April 6 and a $3.25 billion deal for Hut 8 DC on April 27. For HY, the heady pace continued into early May, even without the announcement of new AI bonds. A big early influx on May 4 included M&A/LBO bonds for First Eagle Holdings ($575 million) and BASF Coatings (€1.95 billion-equivalent across euro- and dollar-denominated tranches), and refinancings for The Venetian Resort Las Vegas ($1.175 billion), Delek Logistics ($800 million), Yahoo ($700 million), Bombardier ($500 million), Owens-Brockway Glass Container ($500 million), and Academy ($500 million). More refinancings surfaced May 5 via deals for Solaris Energy Infrastructure ($1.3 billion), MGM China ($750 million), and Blackstone Mortgage Trust ($450 million). April showers April’s $40 billion monthly contrasts with the tariff-impacted total in April 2025 ($8.6 billion), and it propelled YTD issuance ($119.7 billion) 55% ahead of the January-April total last year ($77.2 billion). That’s the fastest YTD pace since 2021 (a record year for HY issuance), and it’s already more than issuers placed in all of 2022. Deal flow turned spotty after Liberation Day last year, with deal pricings during just 24% of the available business days that month. This year, wartime uncertainties limited deal pricings to an atypically low 36% of March’s sessions. But cease-fire dynamics opened the spigots for pricings during 68% of April’s business days this year, on par with April 2024. While April bond volume nearly doubled March’s $21 billion total, April’s loan volume ($21 billion) slowed from March ($32 billion). Overall, leveraged finance volume (loans and bonds) totaled $61 billion in April, the most since a loan-heavy January. Within the bond category, the skew to secured jumbo data center offerings resulted in secured bonds accounting for 63% of total April volume. Senior bonds now account for a slim 51% majority of YTD bond volume, versus 55% for the first four months last year. High quality, higher yields Those mostly double-B AI bonds are preserving a skew to higher-rated issues in uncertain times. In April, nearly half (46%) of all new bonds carried straight double-B ratings, after similarly lofty readings in February (51%) and March (43%). April was in line with the 2025 annual average (47%), an all-time high. The prior peak, at 37%, was in 2019. Even with the high-quality mix, however, clearing yields increased in April, including 9%-plus yields for data center deals for SE Cosmos and CoreWeave, an EnQuest senior refinancing, and Sealed Air LBO bonds. The average 7.60% clearing yield overall was up 82 bps from March, though still below a 7.80% average last April. Growth targets In terms of uses of proceeds, LCD broadly groups AI/data center bonds under general corporate purposes. Bonds allocated for GCP were 42% of the total, a high since May 2022. Those AI bonds are then grouped under a sub-heading (Expansion/Capex), which, at 40% of the overall total, hit a record high. Refinancing was 44% of the total, up a bit from a shock wartime low at 25% in March, but still indicative of spotty opportunism as rates rise. April tends to be a weathervane for refinancing trends, coming in at 60% of the total in low-cost April 2020 and 71% of volume in 2024 (a record year for refinancing’s share of the market). Conversely, it was less than 15% in April 2022 as the Fed hiked rates, and it was 55% in April 2023. Companies this year have favored fixed rates when refinancing. Issuers allocated proceeds from $10.7 billion of bond offerings to refinance existing institutional loans from January-April, which trails only two YTD periods (in 2013 and 2024) on record, per LCD. Make-up test For bondholders, April was a comeback month after a brutal March. Abetted by a full retracement of the wartime spread expansion late February and through March, S&P’s broad HY index gained 1.65% for the month, erasing a 1.31% loss in March and marking the best monthly performance since a similar gain last June. While higher rates late in the month eroded early gains, the average bid for LCD’s flow-name high-yield bond sample (15 bonds) still ended the month up roughly two points, at 95.8% of par. That’s after it dropped 219 bps from Feb. 26-March 26. As bids recovered, investors put $5.8 billion to work in HY retail funds from April 2-30, after withdrawals of $8.8 billion over the previous four weeks. Flows are negative in 2026 (overall outflows are $3.58 billion), driven by YTD outflows from both ETFs ($2.16 billion) and mutual funds ($1.42 billion). Sign up for The Credit Pitch Weekly coverage of US and European loans, bonds, private credit, and more. Subscribe Alphotographic/Getty Images This article originally appeared on PitchBook News Alphotographic/Getty Images

Comments

You must be logged in to comment.