yahoo Press

Do Wall Street Analysts Like TJX Companies Stock?

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

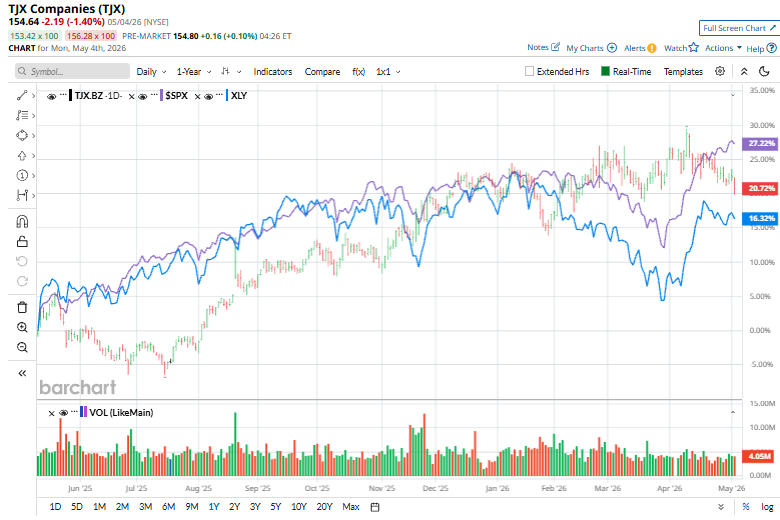

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Framingham, Massachusetts-based The TJX Companies, Inc. (TJX) is a global off-price retailer that sells branded apparel and home goods at significant discounts. Its business model is built on opportunistic buying, sourcing excess inventory, overruns, and end-of-season merchandise from suppliers and offering them at prices typically 20–60% below traditional retail prices. With a market cap of approximately $173.6 billion, TJX Companies operates through Marmaxx, HomeGoods, TJX Canada, and TJX International segments. Shares of the fashion retail giant have gained 19.7% over the past 52 weeks and marginally in 2026, lagging behind the S&P 500 Index’s ($SPX) 26.6% rally over the past year and 5.2% return on a YTD basis. Dear Western Digital Stock Fans, Mark Your Calendars for June 5 Dear CoreWeave Stock Fans, Mark Your Calendars for May 7 CEO Anthony Noto Makes It Clear That SoFi Should Be Valued Like a Software Stock: Q1 Marked 18 Quarters of Rule of 40 Strength Our exclusive Barchart Brief newsletter is your FREE midday guide to what's moving stocks, sectors, and investor sentiment - delivered right when you need the info most. Subscribe today! Narrowing the focus, TJX has outperformed the sector-focused State Street Consumer Discretionary Select Sector SPDR Fund’s (XLY) 16.9% uptick over the past 52 weeks and 1.4% dip this year. TJX Companies has delivered steady performance over the past year, but it hasn’t kept pace with the strong rally in high-growth sectors like technology and AI, which have driven much of the market’s upside. Additionally, TJX’s defensive, value-oriented profile works against it in bullish environments. When investors favor growth and risk-on assets, capital tends to rotate away from stable retail names like TJX. The company also faces margin pressures from freight, wages, and sourcing costs, as well as a limited e-commerce presence, which can make it appear less competitive than omnichannel peers. For the full fiscal 2027, ending in January, analysts expect TJX to deliver an EPS of $5.06, up 7% year-over-year. Moreover, the company has a robust earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters. Among the 21 analysts covering the TJX stock, the consensus rating is a “Strong Buy.” That’s based on 18 “Strong Buys,” one “Moderate Buy,” and two “Holds.” This configuration is slightly more optimistic than three months ago, when 17 analysts gave “Strong Buy” recommendations. On Feb. 26, Barclays analyst Adrienne Yih raised the price target on TJX Companies to $183 from $172, while reiterating an “Overweight” rating. The upward revision reflects continued confidence in the company’s operating momentum and outlook. TJX’s mean price target of $174.78 suggests a 13% upside potential. Meanwhile, the street-high target of $193 represents a notable 24.8% premium to current price levels. On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.