yahoo Press

Bloom Energy Fueling Transition to Critical AI Infrastructure Provider

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

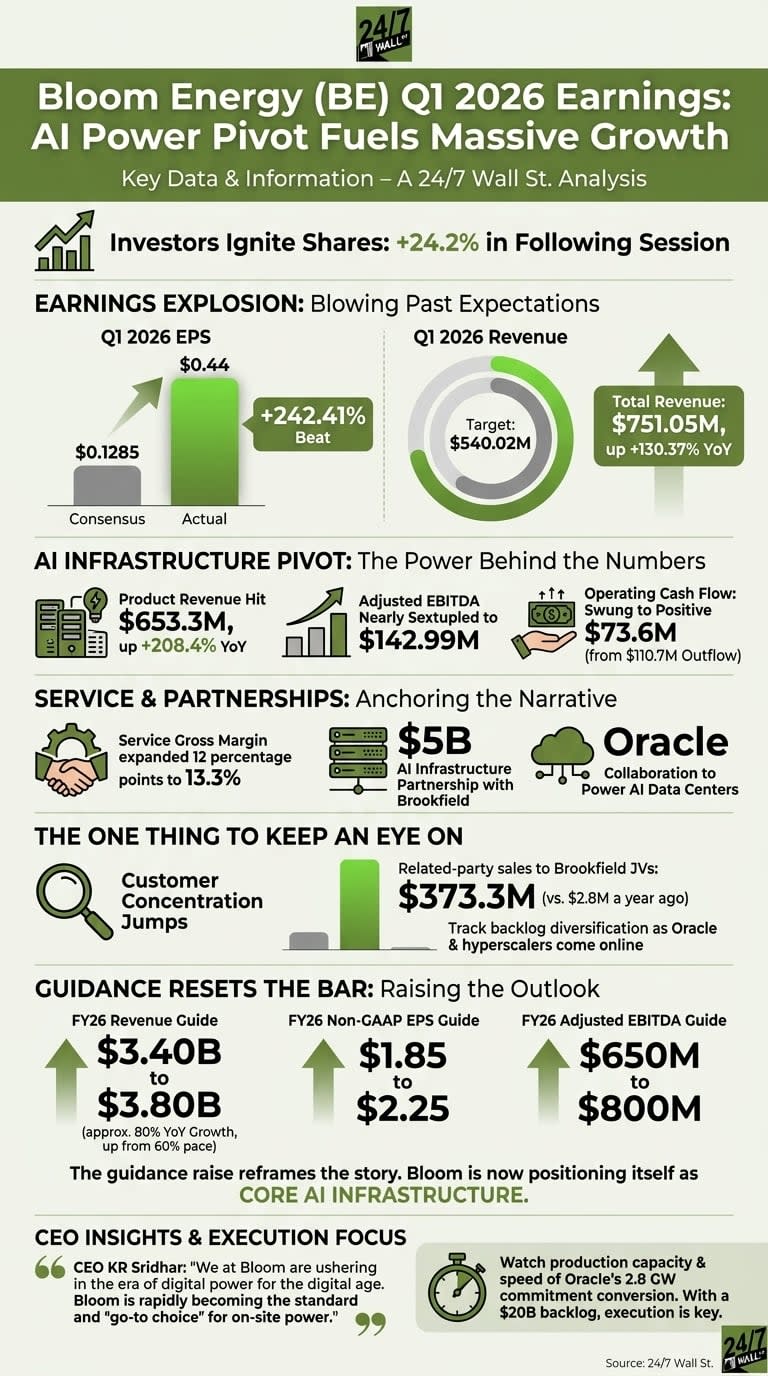

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Bloom Energy (BE) reported Q1 2026 EPS of $0.44, crushing the $0.13 consensus, with product revenue surging 208% to $653.3M and full-year guidance raised to $3.4B-$3.8B revenue. Bloom’s AI infrastructure deals with Brookfield and Oracle are converting into the top-line growth that justifies positioning the company as core AI power infrastructure. The analyst who called NVIDIA in 2010 just named his top 10 stocks and Bloom Energy wasn't one of them. Get them here FREE. Bloom Energy (NYSE:BE) reported Q1 2026 results after the close on April 28, 2026, and the earnings report blew past expectations. EPS came in at $0.44 against a $0.1285 consensus, revenue more than doubled, and management raised full-year guidance well above the prior bar. Investors loved it. Shares jumped 24.2% in the session that followed. The story here is the AI infrastructure pivot finally showing up in the numbers. Product revenue alone hit $653.3 million, up 208.4% year over year, and total revenue grew 130.37%. Adjusted EBITDA nearly sextupled to $142.99 million, and operating cash flow swung to $73.6 million from a $110.7 million outflow a year ago. I liked the service line. Service gross margin expanded 12 percentage points to 13.3% on a GAAP basis, which signals the installed base is finally earning its keep. The $5 billion AI infrastructure partnership with Brookfield Asset Management and the Oracle collaboration to power AI data centers are anchoring the narrative. The analyst who called NVIDIA in 2010 just named his top 10 stocks and Bloom Energy wasn't one of them. Get them here FREE. Customer concentration jumped. Related-party sales to Brookfield JVs were $373.3 million, versus $2.8 million a year ago. That is a feature of the AI deal flow, but you should track how diversified the backlog converts as Oracle and other hyperscalers come online. A 242% earnings beat proves it—the AI power rush is no longer just hype, it's a massive revenue engine. Management raised the full-year outlook materially. Here is the new shape of 2026: Adjusted EPS: $0.44 vs. $0.1285 expected (242.41% beat) Revenue: $751.05M vs. $540.02M expected; up 130.37% GAAP Operating Income: $72.19M vs. a $19.07M loss a year ago Adjusted EBITDA: $142.99M FY26 Revenue Guide: $3.40B to $3.80B (about 80% YoY growth at midpoint, up from a prior 60% pace) FY26 Non-GAAP EPS Guide: $1.85 to $2.25 FY26 Adjusted EBITDA Guide: $650M to $800M The guidance raise is what reframes the story. Bloom is now positioning itself as core AI infrastructure. CEO KR Sridhar kept the message tight, saying "We at Bloom are ushering in the era of digital power for the digital age. Bloom is rapidly becoming the standard and 'go-to choice' for on-site power." I thought the language was deliberate. Sridhar wants Bloom anchored to AI buildouts. You will want to watch production capacity and how fast Oracle's 2.8 GW commitment translates into shipments. With a $20 billion backlog and shipments 800V DC-ready, execution is the only thing standing between Bloom and the AI power story it just sold the market. This analyst's 2025 picks are up 106% on average. He just named his top 10 stocks to buy in 2026. Get them here FREE.

Comments

You must be logged in to comment.