yahoo Press

Dangote at Full Throttle as Nigeria Becomes a Net Fuel Exporter

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

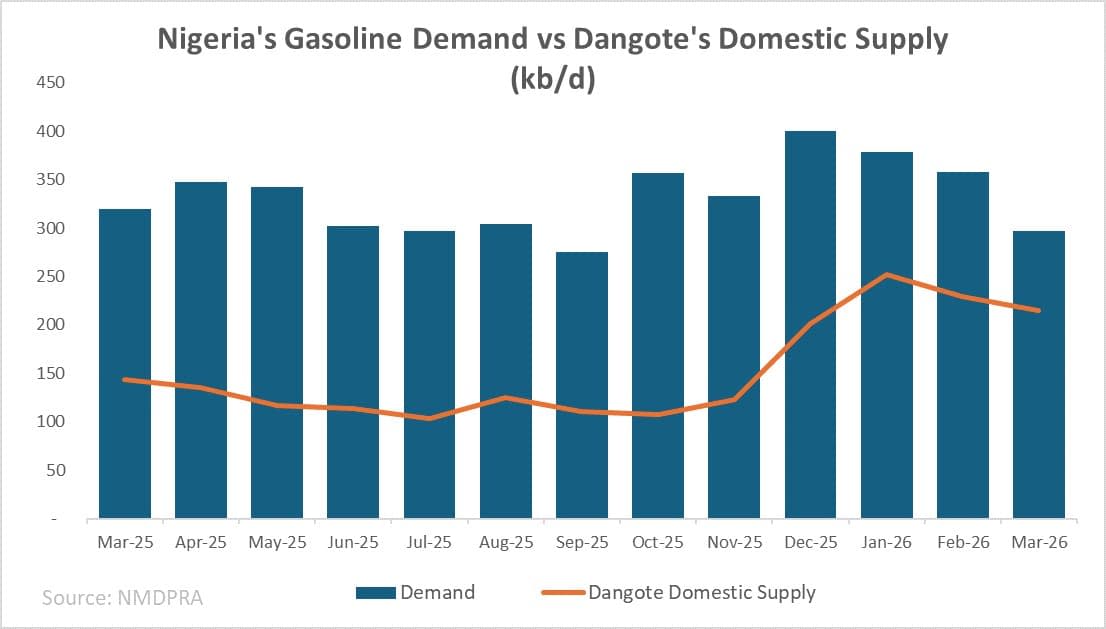

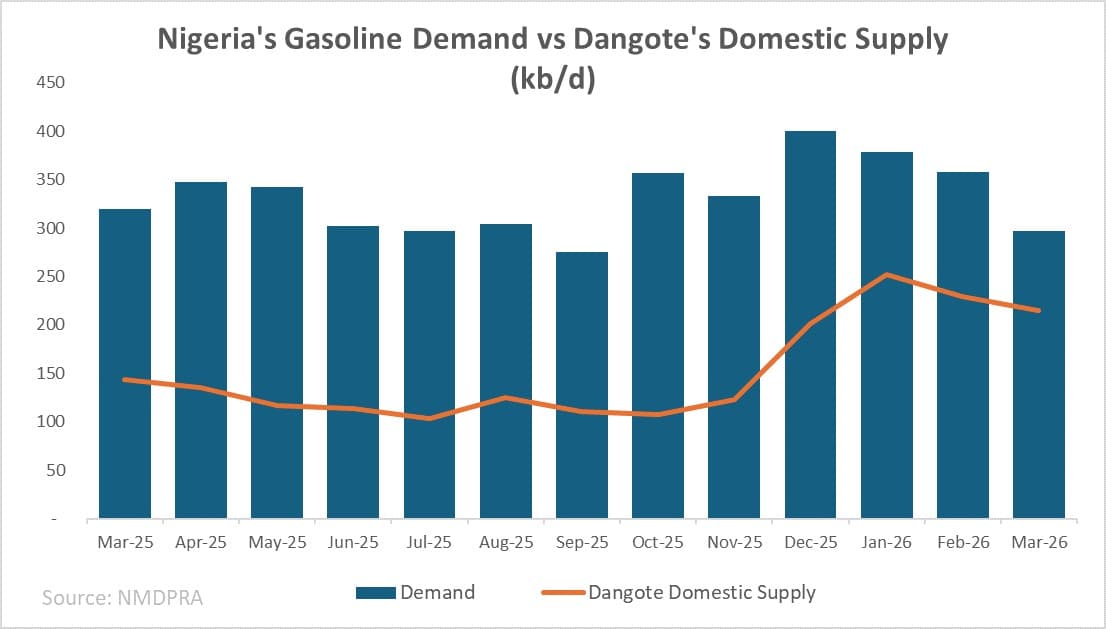

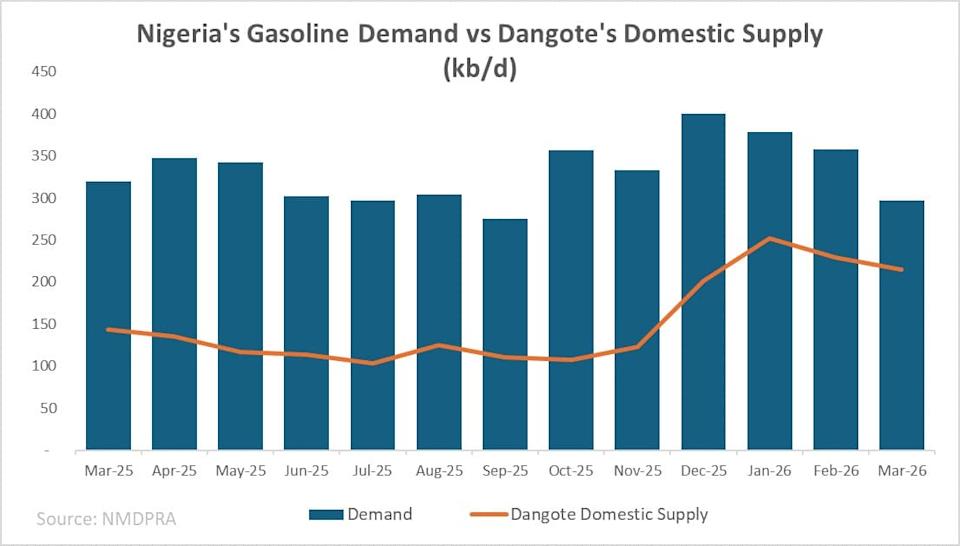

Nigeria is finally starting to fix a long-standing imbalance: a major crude exporter that couldn’t meet its own fuel demand. That shift is now materializing in hard numbers—and it is being driven entirely by the Dangote refinery, which is already running close to full capacity and shows little sign of slowing. In a market starved of refined products, this rising refining giant is quickly emerging as one of the few reliable sources in the current supply squeeze, particularly for Europe. In March, gasoline exports rose to 55,000 b/d while imports fell to around 40,000 b/d—the lowest import level in a decade—effectively flipping the country to a net gasoline exporter for the first time in history. At a moment when global refining margins are soaring, with crack spreads across diesel and jet fuel hovering at record highs, the timing could hardly be more advantageous. The change in Nigeria’s refining system is concentrated in a single asset. Nigeria’s three state-owned refineries remain non-operational, constrained by a familiar mix of weak economics, governance failures, and infrastructure decay. Instead, the entire turnaround story rests on the 650,000 b/d Dangote refinery, which began operations in January 2024 and has rapidly scaled up operations to become the dominant force in the country’s downstream sector. By March, the refinery was running at 94% capacity, producing around 303,000 b/d of gasoline against domestic demand of roughly 300,000 b/d. For the first time, a single facility was sufficient to cover national gasoline consumption. That alone would mark a structural break from the past. However, roughly one-sixth of gasoline output is now exported, with 45,000 b/d shipped in March primarily to neighbouring African markets such as Ivory Coast, the DRC, and Mozambique (for the first time ever). What used to be a regional redistribution model is increasingly turning into a platform for arbitrage. Related: US Oil Drillers Scale Back as Global Supply Crunch Continues Feedstock is based on 1/3 imported crude and 2/3 domestic crude supply. In February and March, Dangote imported an average 215,000 b/d of WTI Midland and WTI grades, reflecting both pricing advantages and compatibility with its configuration. But that flow is already being tested. With WTI increasingly pulled into Asia-Pacific markets amid the disruption of Middle Eastern supply routes and the effective closure of the Strait of Hormuz, availability has become tighter. The result is a search of alternatives: Dangote has sourced a Suezmax cargo of Guyanese Golden Arrowhead crude (36 degrees API), around 145,000 tonnes sold by Chevron, marking the first such shipment from Guyana to West Africa. It is a small but telling signal of how flexible sourcing will need to become as Atlantic Basin barrels are getting pricier and less available. Domestic crude still anchors the system. In March, the Nigerian National Petroleum Company (NNPC) supplied around 380,000 b/d to the refinery out of total 580,000 b/d. If gasoline tells the story of import substitution, jet fuel reveals the export opportunity. Domestic demand stands at just 13,000 b/d, yet Dangote exported around 100,000 b/d in March. Europe has emerged as a key destination, absorbing roughly half of these volumes. The pull is obvious: jet crack spreads have been trading in a crisis-inflated range of $86–108/bbl through April, while inventories in the Amsterdam-Rotterdam-Antwerp (ARA) hub have dropped to 597,000 tonnes – the lowest since April 2020. In early April alone, 1.6 million barrels of jet fuel were loaded for Europe (already exceeding March totals) with France, Spain and the UK among the key buyers. This creates a straightforward arbitrage logic: Dangote’s owner may feel tempted to redirect flows from lower-margin African markets toward Europe. In practice, Dangote could shift as much as an additional 40,000 b/d of jet exports away from regional buyers to Europe without straining domestic supply. The constraint is not demand – it is logistics. Freight rates from West Africa to ARA have surged to $8.5/bbl for a 60 kt Aframax cargo and close to $10/bbl for 40 kt cargoes, with voyage times stretching 17–22 days. At current jet margins, the economics are still clear – even with freight prices at $8.5-10/bbl of jet selling to Europe is lucrative enough; for diesel, the picture is tighter. Domestic diesel consumption in Nigeria stood at 90,000 b/d in March, while Dangote produced around 104,000 b/d. Only 15,000 b/d was absorbed locally (as country largely runs on gasoline), leaving roughly 65,000 b/d for export, primarily to South Africa, Cameroon, and Ivory Coast. With European diesel cracks also elevated – trading in the $45–55/bbl range – there is a growing temptation to pivot away from regional markets. The question is whether freight costs continue to cap that shift or whether sustained margin strength forces a reorientation regardless. So far, no diesel cargoes are heading from Nigeria to Europe. The strategy of the company extends beyond fuels. Dangote plans to double refining capacity to 1.4 million b/d by 2028 in partnership with Honeywell, integrating petrochemical production into the complex. The project targets 750,000 t/year of propylene and 400,000 t/year of detergents, effectively pushing the refinery into higher-margin chemical value chains. Upstream integration, while still modest, is also emerging. The Dangote group currently produces around 4,500 b/d from the Kalaekule field, with output expected to rise to 15,000 b/d in the coming months. On its own, this is not transformative, but it signals a broader ambition to control more of the value chain from crude to chemicals. Still, the story is not frictionless. The refinery may be running near full capacity, but the system around it is far less stable. Crude supply is the first issue. Pipeline disruptions and theft continue to affect flows, while Nigeria’s domestic crude is often too light and sweet for optimal runs, pushing Dangote to import crude to balance its feedstock. That immediately exposes it to global price volatility. Then there is the relationship with NNPC, where supply volumes, pricing and payment structures remain inconsistent, adding another layer of uncertainty. On the export side, the constraint is simpler: freight is expensive now and is predicted to stay so even after the blockade of Hormuz is over. Moving products from West Africa to Europe can quickly exhaust the margins, limiting how much can realistically be redirected even in a tight market. And over all of this sits policy risk. Nigeria’s fuel pricing and supply rules can shift quickly, and the pressure to prioritize domestic needs over exports never fully goes away. The result is a refinery that works – but operates in an environment that is highly unpredictable. And yet, even within these constraints, Dangote still stands out. Europe needs barrels, urgently and structurally, and there are not many places left to source them at scale. That leaves Nigeria’s new refining giant one of the more credible answers to Europe’s fuel shortage answers – at least where freight still makes the trade work. By Natalia Katona for Oilprice.com More Top Reads From Oilprice.com Pakistan Turns to Russia and Venezuela as Middle East Oil Supplies Shrink India Pushes Refiners To Boost LPG Output Trump Extends Jones Act Shipping Waiver Through August Oilprice Intelligence brings you the signals before they become front-page news. This is the same expert analysis read by veteran traders and political advisors. Get it free, twice a week, and you'll always know why the market is moving before everyone else. You get the geopolitical intelligence, the hidden inventory data, and the market whispers that move billions - and we'll send you $389 in premium energy intelligence, on us, just for subscribing. Join 400,000+ readers today. Get access immediately by clicking here.

Comments

You must be logged in to comment.