yahoo Press

Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

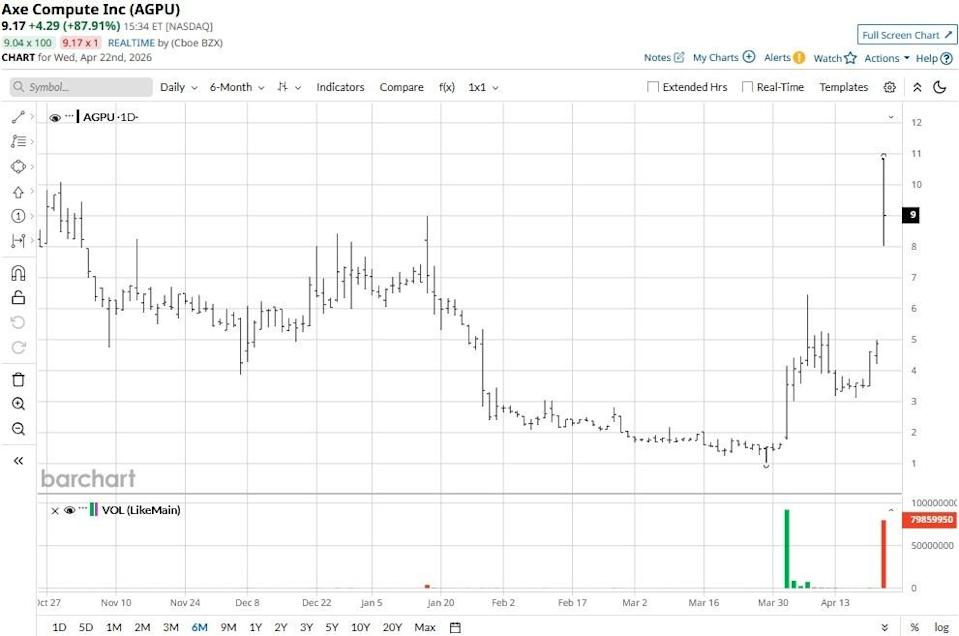

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Axe Compute (AGPU) stock more than doubled on April 22 after the company announced a massive $260 million enterprise infrastructure deal involving 2,304 Nvidia (NVDA) B300 chips. This landmark contract — the largest in AGPU’s history — drove its relative strength index (14-day) into the mid-80s, signaling the stock may be due for a pullback in the near term. Broadcom Breakup: AVGO Stock Slumps as Google Considers Its Rival for a Deal. Should You Buy the Dip? AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here? Sandisk Just Joined the Nasdaq-100. Should You Buy SNDK Stock Here? Tired of missing midday reversals? The FREE Barchart Brief newsletter keeps you in the know. Sign up now! At its intraday peak, Axe Compute shares were seen trading at more than 7x their price last month. The Nvidia deal brings much-needed validation to Axe Compute, which is why investors were sent into a frenzy on Wednesday morning. By securing thousands of Nvidia’s most sophisticated Blackwell GPUs, the Nasdaq-listed firm has positioned itself as a serious contender in the high-stakes artificial intelligence (AI) infrastructure race. The contract, structured as a three-year, take-or-pay agreement, offers a predictable recurring revenue stream, which has historically been a weak spot for Axe Compute. All in all, for the company that’s generated just $130,000 in revenue in the trailing 12 months, the NVDA deal represents a monumental leap in scale. This signals that enterprise clients are increasingly turning to smaller, more agile providers to bypass hyperscaler supply constraints. Despite the euphoria, Axe Compute remains a high-risk play, given its penny stock status that makes it vulnerable to extreme volatility and potential pump-and-dump behavior. At a price-to-sales (P/S) ratio of more than 200x, AGPU shares are egregiously overvalued given the company’s alarming GAAP loss of $13.37 per share in its latest fiscal year. Plus, the $260 million deal doesn’t begin deployment until Q3, which means Axe Compute must survive another quarter or two of high burn before cash flow so much as begins to improve. Meanwhile, execution and dilution risks remain a dark cloud over AGPU’s current rally as well. Another major red flag on Axe Compute is the absence of Wall Street coverage. This means investors have absolutely no professional guidance on valuation and prospects, which often helps a great deal in navigating global financial markets. On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.