yahoo Press

What to Expect From Walt Disney's Next Quarterly Earnings Report

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

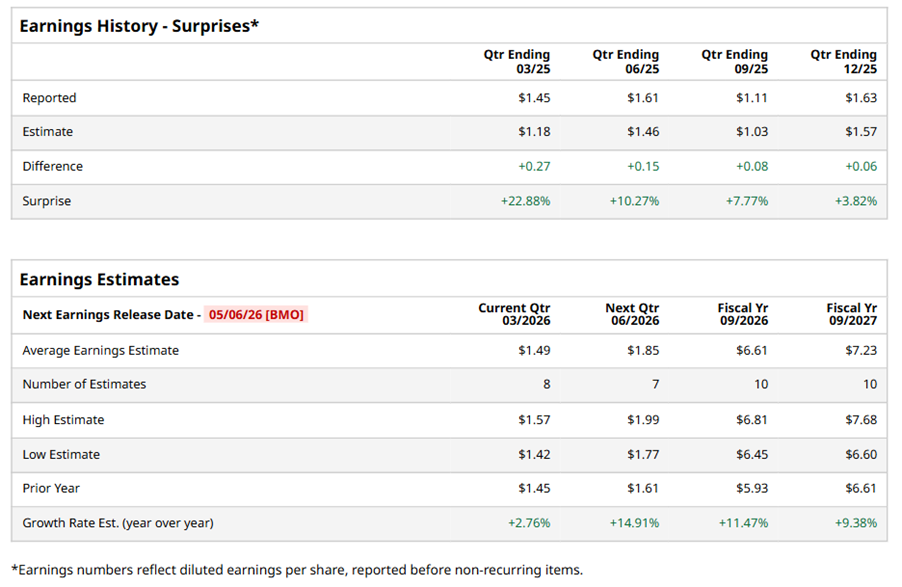

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. Burbank, California-based The Walt Disney Company (DIS) operates as an entertainment company worldwide. Valued at $188.3 billion by market cap, the company's businesses include, media networks, parks and resorts, studio entertainment, consumer products, and interactive media. The entertainment giant is expected to announce its fiscal second-quarter earnings for 2026 before the market opens on Wednesday, May 6. Ahead of the event, analysts expect DIS to report a profit of $1.49 per share on a diluted basis, up 2.8% from $1.45 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports. Tesla Earnings, Hormuz and Other Key Things to Watch this Week Netflix Generates Massive FCF and FCF Margins - NFLX Price Targets Are Higher Profit Jumped 58% at Taiwan Semi. Does That Make TSM Stock a Buy Here? Our exclusive Barchart Brief newsletter is your FREE midday guide to what's moving stocks, sectors, and investor sentiment - delivered right when you need the info most. Subscribe today! For the full year, analysts expect DIS to report EPS of $6.61, up 11.5% from $5.93 in fiscal 2025. Its EPS is expected to rise 9.4% year over year to $7.23 in fiscal 2027. DIS stock has underperformed the S&P 500 Index’s ($SPX) 34.9% gains over the past 52 weeks, with shares up 25.3% during this period. Similarly, it underperformed the State Street Communication Services Select Sector SPDR ETF’s (XLC) 32% gains over the same time frame. DIS lagged as tighter immigration policy cut high-spend international park traffic, while linear TV declines outpaced streaming gains. Its subscriber growth stalled even as Netflix, Inc. (NFLX) added 23 million members last year. Entertainment profits fell on high content/marketing costs, and ESPN slipped due to rights inflation, sub losses, and distribution issues. Furthermore, DIS’ soft Q2 guidance and margin pressure from streaming investments, expansion, and turnarounds further weighed on sentiment. Analysts’ consensus opinion on DIS stock is bullish, with a “Strong Buy” rating overall. Out of 31 analysts covering the stock, 21 advise a “Strong Buy” rating, five suggest a “Moderate Buy,” four give a “Hold,” and one recommends a “Strong Sell.” DIS’ average analyst price target is $131.64, indicating a potential upside of 23.8% from the current levels. On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Comments

You must be logged in to comment.