yahoo Press

Tesla Stock Forecast Teeters as Barclays Analyst Dan Levy Warns of a ‘Negative $3 Billion’ Cash Hole

Images

1 / 4

2 / 4

3 / 4

4 / 4

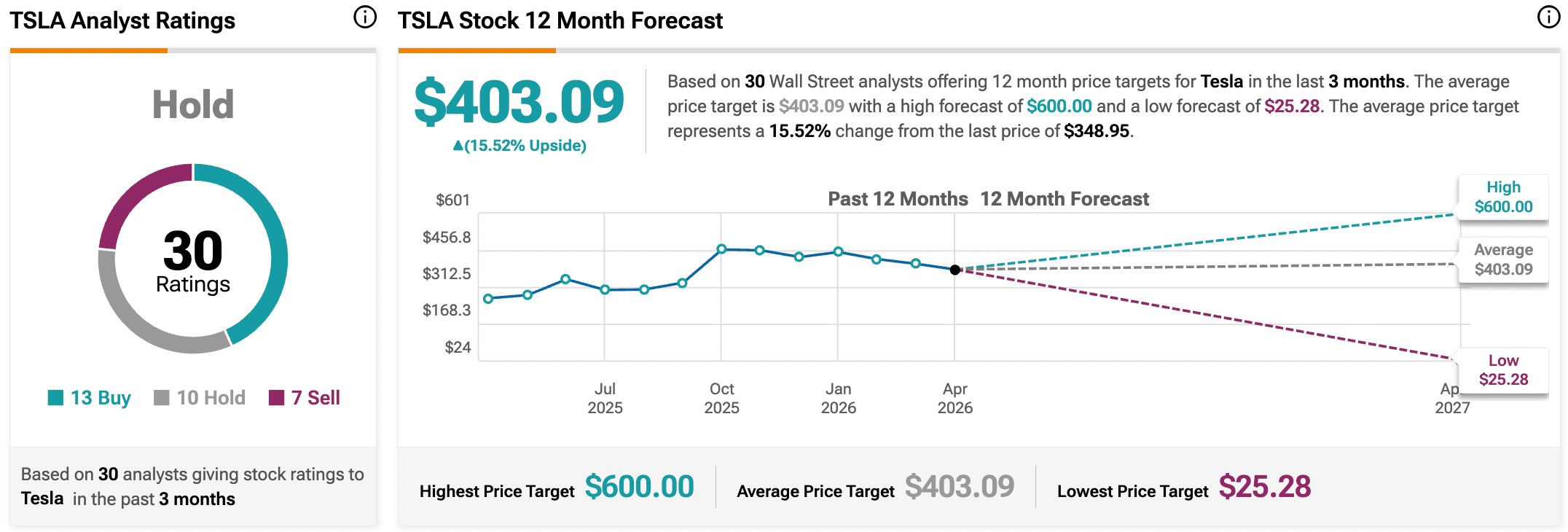

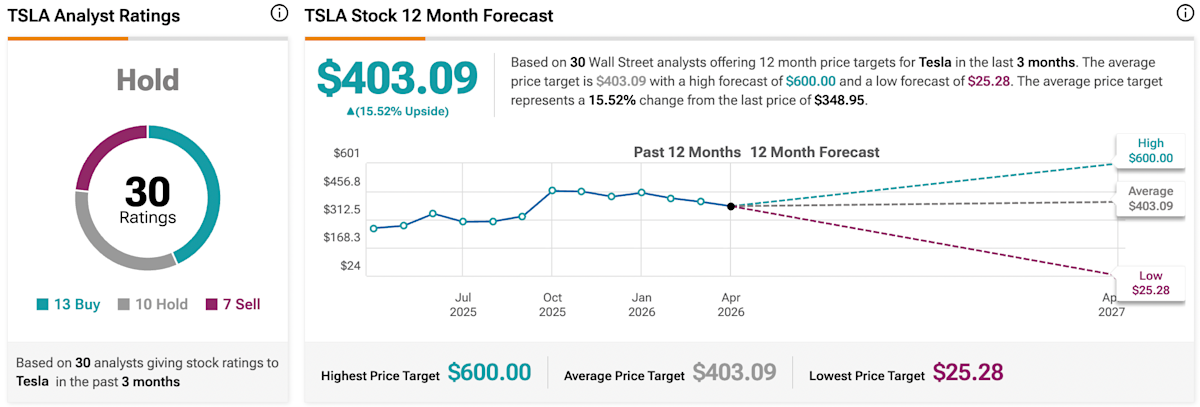

The above button links to Coinbase. Yahoo Finance is not a broker-dealer or investment adviser and does not offer securities or cryptocurrencies for sale or facilitate trading. Coinbase pays us for certain activity generated through this link. Prices displayed are informational. The world’s most famous electric car maker is entering a gambling phase with its new technology. Today, Barclays (BCS) analyst Dan Levy maintained his “Equalweight” rating on Tesla (TSLA), while issuing a stern warning about the company’s massive spending plans. Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks While Tesla fans are excited about the new Terafab chip factory project, Levy is concerned about the actual cost of building Elon Musk’s dream. He kept his price target at $360, even as other analysts have pushed their forecasts much higher. The main takeaway from today’s report is that Tesla might be underestimating how much money it needs to build its future. The company recently revealed plans for the Terafab project, which aims to produce massive amounts of chips for self-driving cars and robots. In today’s report, Levy cautioned that the project could demand expenditures “many multiples” beyond even his most optimistic scenarios. While Tesla is already planning to spend over $20 billion on capital projects this year, Levy warns that the real cost of this new chip initiative will be “likely well more than an order of magnitude higher” than what the company has told the public so far. The high cost of these physical AI projects is starting to show up in the company’s bank account. For years, Tesla was known for its ability to generate cash, but the Terafab era is changing that. Levy highlighted that Barclays projects Tesla’s 2026 free cash flow at “negative $3 billion” even before it starts counting the costs of the new chip factory. This means the company is currently spending more to build its future than it is making from selling cars. Levy noted that while the vision for robots and AI is exciting, a “solid underlying auto business will be required to fund a portion of Tesla’s growth aspirations.” Perhaps the most surprising part of today’s analysis is how little the actual car sales seem to matter to investors right now. Levy pointed out that the usual numbers, like how many cars Tesla delivers each quarter, have taken a back seat to the AI story. He wrote in today’s note that it has become “increasingly evident to us that auto volumes (and broader fundamentals) have increasingly become an afterthought.” At this point, the stock is being moved almost entirely by the narrative of what Tesla could become. Because of this, Barclays is staying on the sidelines, waiting to see if the company can actually afford to turn its massive AI dreams into reality. Analysts remain cautious on Tesla’s long-term outlook. On TipRanks, TSLA has a Hold consensus rating based on 13 Buys, 10 Holds, and seven Sell ratings. The average 12-month Tesla price target of $403.09 implies 15.5% upside potential from current levels. See more TSLA analyst ratings Disclaimer & DisclosureReport an Issue

Comments

You must be logged in to comment.