yahoo Press

Wall Street Sees 58% Upside in Microsoft (MSFT) After Selloff

Images

1 / 4

2 / 4

3 / 4

4 / 4

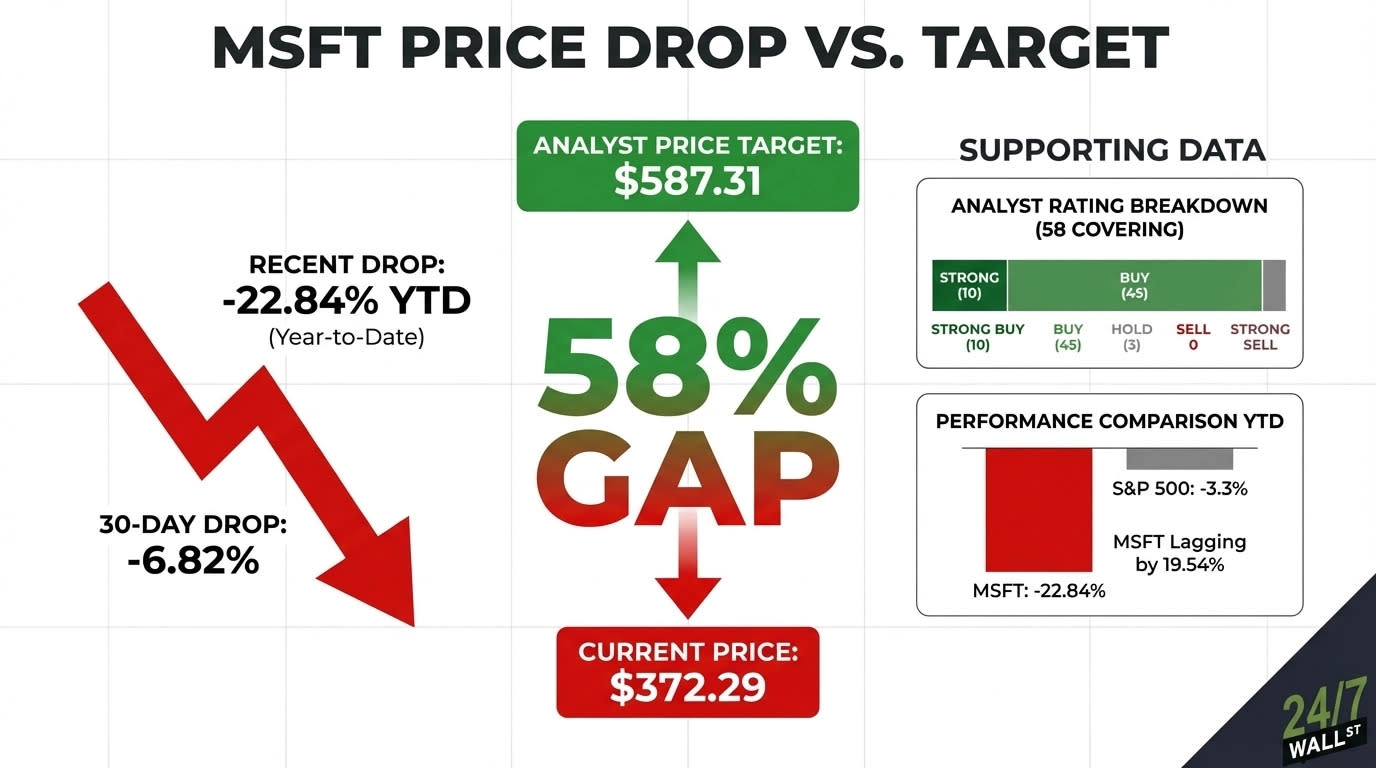

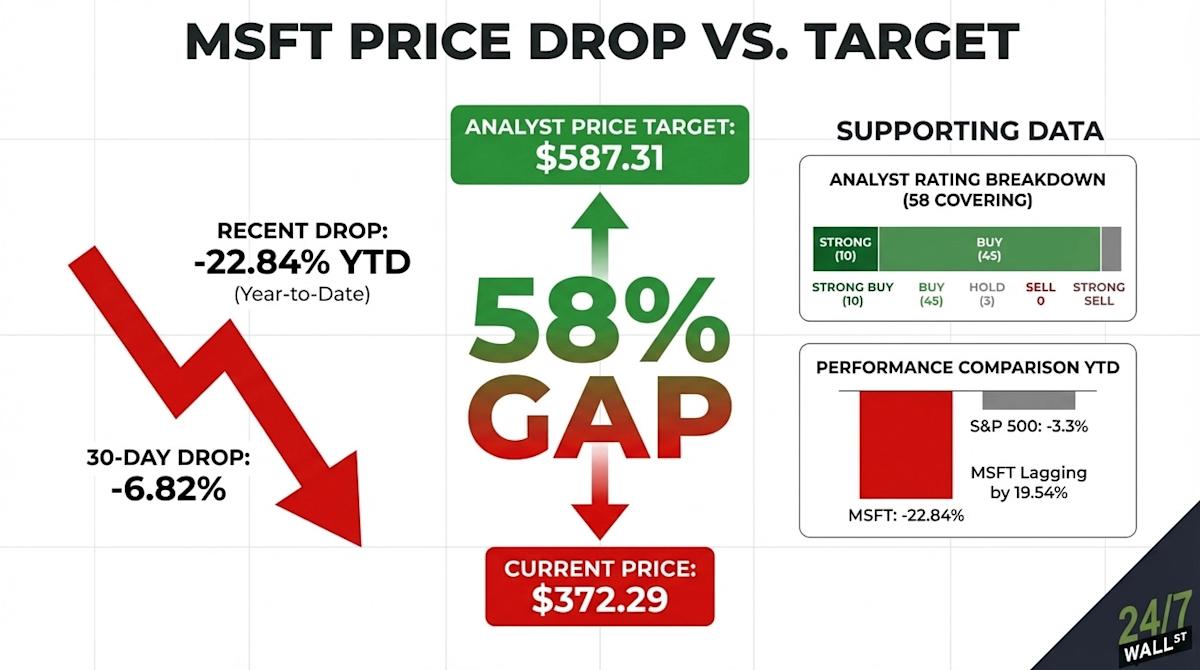

Microsoft (MSFT) reported Q2 revenue of $81.27B, beating estimates by 1.2%, but CapEx nearly doubled year-over-year to $29.88B as Azure growth decelerated from 40% to 39%, with guidance pointing to 37-38% growth next quarter; Microsoft Cloud revenue crossed $51.50B, growing 26% year-over-year, and commercial RPO surged 110% to $625B. Microsoft trades 58% below analyst consensus at $372.29 versus $587.31, down 22.84% year-to-date while the S&P 500 is down only 3.3%, as the market questions whether Azure’s decelerating growth justifies the company’s massive AI infrastructure spending. If you're focused on picking the right stocks and ETFs you may be missing the bigger picture: retirement income. That is exactly what The Definitive Guide to Retirement Income was created to solve, and it's free today. Read more here Microsoft (NASDAQ:MSFT) currently trades at $372.29, while the average analyst price target sits at $587.31, a gap of roughly 58% between where the stock is and where Wall Street thinks it belongs. Microsoft operates three core segments: Productivity and Business Processes (Microsoft 365, LinkedIn, Dynamics 365), Intelligent Cloud (Azure and enterprise services), and More Personal Computing (Windows, Xbox, Surface). CEO Satya Nadella has positioned Azure as the backbone of enterprise AI adoption, a narrative Wall Street rewarded generously until recently. When Microsoft reported Q2 FY2026 results on January 28th, the stock dropped 9.99% on the day despite beating EPS estimates by 7.57% and posting revenue of $81.27 billion against an $80.28 billion estimate. If you're focused on picking the right stocks and ETFs you may be missing the bigger picture: retirement income. That is exactly what The Definitive Guide to Retirement Income was created to solve, and it's free today. Read more here The culprit behind this massive selloff was the company's capital expenditure spending. CapEx nearly doubled year-over-year to $29.88 billion in Q2, a 89% increase, raising a legitimate question: is Azure growing fast enough to justify the bill? Azure's growth rate has been decelerating, moving from 40% in Q1 FY2026 to 39% in Q2, with guidance pointing to 37% to 38% growth next quarter. Microsoft is down 22.84% year-to-date from a high near $520 in August 2025, a slide driven by valuation compression across high-multiple tech names and specific concern about AI spending trajectory. The Q2 earnings reaction accelerated a decline already underway. Of the 58 analysts covering the stock, 10 rate Microsoft a Strong Buy, 45 rate it a Buy, and 3 rate it a Hold. There are zero Sell or Strong Sell ratings, which speaks to the widely held consensus that the company remains a high-quality, durable compounder despite near-term uncertainties. The bull thesis rests on three pillars: Commercial remaining performance obligation surged 110% year-over-year to $625 billion in Q2. Microsoft Cloud crossed $51.50 billion in a single quarter for the first time, growing 26% year-over-year. The restructuring of the OpenAI partnership locked in an incremental $250 billion Azure services commitment from OpenAI and extended Microsoft's IP rights through 2032. Analysts frame the CapEx concern differently than the market. As CEO Satya Nadella put it, "We are still in the beginning phases of AI diffusion and its broad GDP impact, and already we’ve built an AI business that is larger than some of our biggest franchises that took decades to build." If Azure's growth reaccelerates in the back half of FY2026, the spending narrative shifts from liability to competitive moat. The valuation case also looks different at current prices. The stock trades at a trailing P/E of roughly 23x and a forward P/E of 20x, a meaningful discount to where it has traded for most of the past two years. For a company generating $38.46 billion in net income per quarter and returning $12.7 billion to shareholders in dividends and buybacks, analysts view those multiples as undemanding relative to the underlying growth profile. Microsoft trades at $372.29 against a consensus target of $587.31, implying roughly 58% upside. The 52-week range runs from $350.42 to $552.24, placing the stock near its annual low even as the business posts record revenue. Microsoft is down 22.84% year-to-date while the S&P 500 (as measured by SPY) is down roughly 3.3% over the same period. This represents nearly 20 percentage points of underperformance. The 30-day decline of 6.82% significantly outpaced SPY's 1.98% decline over the same window, confirming MSFT-specific selling pressure is driving the gap. With 55 of 58 analysts rating the stock Buy or Strong Buy and no active downgrades visible, the conviction behind those targets is real, though consensus targets can lag during periods of rapid multiple compression. The bull case requires Azure's growth rate to stabilize at or above 37% over the next two quarters and the contracted RPO backlog to convert into accelerating revenue recognition. In that scenario, the CapEx narrative shifts to infrastructure advantage, the multiple re-rates toward the 28x to 30x range the stock commanded a year ago, and the path toward analyst consensus becomes visible. Four consecutive quarters of earnings beats, a 39% profit margin, and $35.76 billion in quarterly operating cash flow reflect a structurally sound business. The bear case materializes if Azure's growth continues decelerating into the 34% to 35% range while CapEx stays elevated near $30 billion per quarter. That combination would force a rethink of the AI investment return thesis, and a 20x forward multiple could compress further. The insider selling activity, with 31 recent transactions trending net negative, is a contrarian signal worth weighing against analyst consensus. The margin for error is thin. Azure guidance over the next two quarters will be the key variable determining whether the gap between current price and analyst consensus narrows or widens. Most investors spend years learning how to pick good stocks and funds. Far fewer have a clear plan for turning those investments into a reliable retirement paycheck. The truth is, the transition from “building wealth” to “living on wealth” is one of the most overlooked risks facing successful investors in their 50s, 60s and 70s. That is exactly what The Definitive Guide to Retirement Income was created to solve. It’s a free guide that outlines the straightforward math and strategies you need to convert your investments to income. Learn more here.

Comments

You must be logged in to comment.