yahoo Press

Insiders Are Scooping Up These 2 ‘Strong Buy’ Stocks

Images

1 / 4

2 / 4

3 / 4

4 / 4

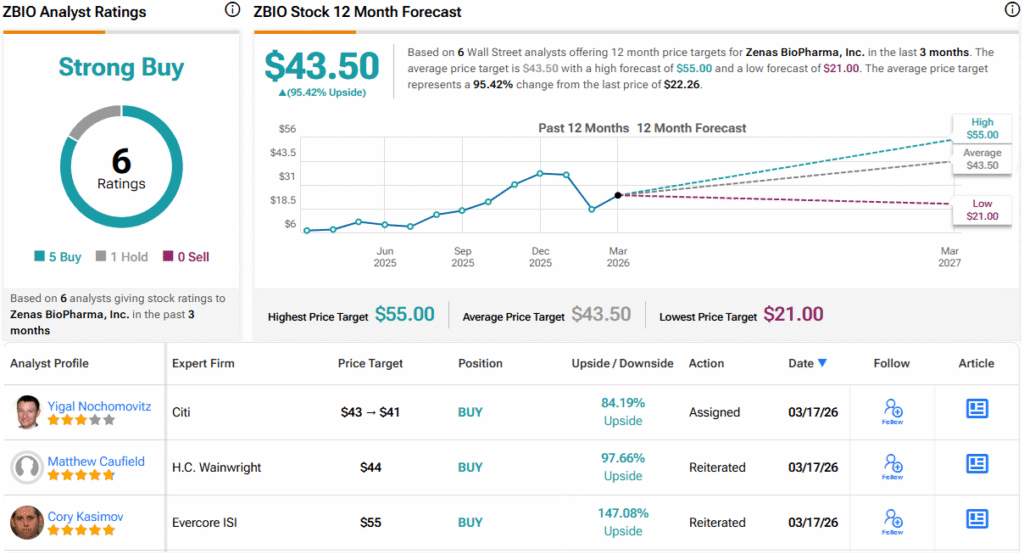

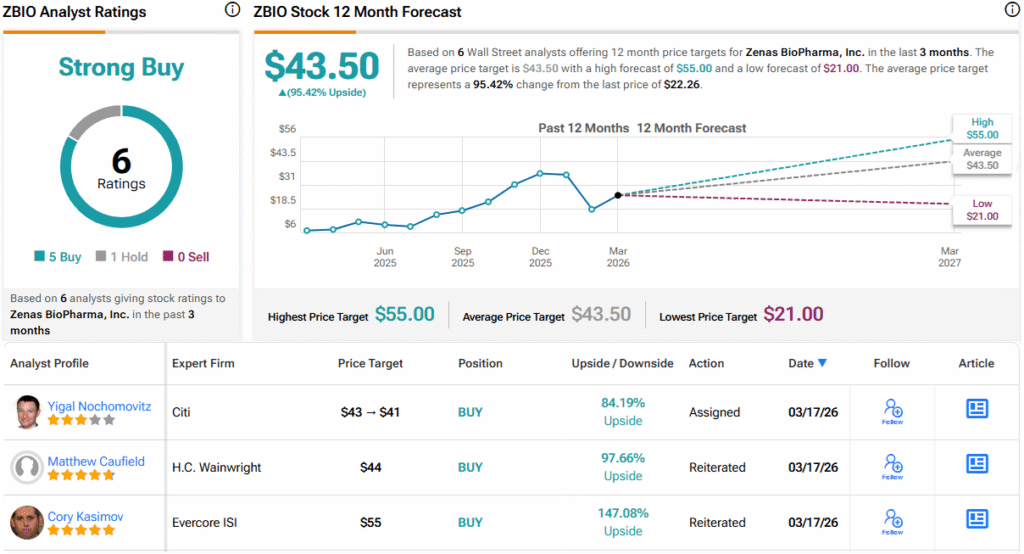

Every investor is looking for an edge, yet the market offers no shortage of strategies, each promising to be the one that finally cracks the code. Some rely on charts, others follow macro trends, while many stick with dividends or lean on analyst opinions. The challenge isn’t finding ideas – it’s figuring out which ones actually hold up when it matters. Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks One approach that has consistently earned its place is tracking insider activity. Executives, board members, and senior leaders aren’t just observing the business from the outside – they are the ones steering it, with a clear view of what’s happening beneath the surface and what could lie ahead. That vantage point makes their trading activity hard to ignore. When insiders start putting serious money to work, it tends to reflect a level of conviction that goes beyond headlines or quarterly noise. And thanks to disclosure rules, those moves don’t stay hidden for long. That’s where the Insiders’ Hot Stocks tool at TipRanks comes into play. It allows investors to follow the money with ease, and right now, it’s highlighting two names where insiders are stepping in aggressively – while Wall Street is backing them up with Strong Buy ratings. Let’s take a closer look. Zenas BioPharma (ZBIO) We’ll start with a clinical-stage biopharmaceutical company, Zenas BioPharma. This firm is working on new treatments and transformative therapies for autoimmune diseases, a class of diseases that is frequently highly resistant to medications. Zenas has developed two drug candidates in this field and brought them to the human trial clinic. The company’s leading candidate, obexelimab, is currently the subject of several late-stage trials. Obexelimab is stated to be a ‘bifunctional monoclonal antibody,’ and it operates by binding CD19 and FcγRIIb. These are surface proteins found on B cells and are broadly present across the B cell lineage. Obexelimab, by binding to these proteins, inhibits the activity of cells that are involved in autoimmune diseases without causing depletion of those cells. This is a unique mode of action, and Zenas believes that it can address the pathogenic role of the B cell lineage in various chronic autoimmune conditions. The drug is designed to be self-administered through a subcutaneous injection. The company’s three leading clinical trials are testing obexelimab against Immunoglobin G4-related Disease (IgG4-RD); Relapsing Multiple Sclerosis (RMS); and Systemic Lupus Erythematosus (SLE). These are involved in both Phase 2 and Phase 3 trials, with the Phase 3 INDIGO study results on the IgG4-RD track expected to support regulatory submission to both the FDA and EMA this year. The Phase 3 study of the drug against primary progressive MS is ongoing, and topline results from the Phase 2 SunStone trial testing obexelimab against SLE are expected for release during the fourth quarter of this year. In addition, Zenas has an active preclinical program, and its drug candidate ZB014, a half-life-extended anti-CD-19 and FcγRIIb mAb, is progressing toward the clinical trial stage. Another preclinical candidate, ZB021, is expected to start a Phase 1 trial in the treatment of rheumatic and/or dermatologic diseases during 2Q26. Zenas is a pre-revenue company, but last month it held a successful public offering of both convertible notes and stock and raised aggregate net proceeds of $287.5 million. The company currently has a market cap valuation of $1.23 billion. This leads us to the insider trade moves. Board of Directors member Lu Hongbo purchased 75,000 shares during that public offering and followed up by purchasing another 3,768 shares shortly afterward. In all, Hongbo spent just over $1.57 million on his recent stock purchases. Concurrently, company CEO Lonnie Moulder spent $1.02 million to pick up 54,000 shares. Moulder’s stake in the company is approximately $47 million; Hongbo’s stands at nearly $9.2 million. For Wedbush analyst Martin Fan, the key point here is the combination of obexelimab’s strength and the deep bench on the preclinical side. He writes of the company and its prospects, “Full results from Ph 3 INDIGO of obexelimab for IgG4-RD should support the case for regulatory approval, and we see the EULAR conference in June as a likely platform. Results from a vaccine sub-study could validate further safety differentiation and commercial uptake, with the ACR conference in November a possible venue in our view. Additional data events this year include topline results from a lupus trial in 4Q26, and SAD/MAD validation of ZB021 (oral IL-17 inhibitor) by year-end. A new half-life extended candidate, ZB014, provides further opportunities to grow an obexelimab franchise. ZBIO remains on our Best Ideas List and with recent price action dropping shares below our already conservative valuation for obexelimab in IgG4-RD alone, we would be buyers on weakness.” Putting this stance into quantifiable terms, Fan rates the stock as Outperform (i.e., Buy) and sets a $45 price target that implies a one-year upside potential of 102%. (To watch Fan’s track record, click here) Zenas has picked up 6 recent analyst reviews, with a 5 to 1 split favoring Buy over Hold that supports a Strong Buy consensus rating. The shares are priced at $22.26, and the $43.50 average price target indicates room for a 95% gain in the next 12 months. (See ZBIO stock forecast) Navan (NAVN) Next on our list of insider picks that Wall Street likes is Navan, a Palo Alto tech company that entered the public trading markets in October of last year. Navan offers a business travel management platform, an essential function in high demand by companies in today’s global economy. Navan’s platform allows users to purchase travel tickets, monitor their travel spending and budgets, take care of payments, and reap savings. Navan works with such well-known names as Spotify, Lyft, Heineken, and Thomson Reuters. The company currently has over 12,500 customers and estimates its total addressable market as $185 billion. In its IPO, Navan put a total of 36,924,406 shares on the market, including a set of 6,924,406 shares sold by existing shareholders. Gross proceeds from the IPO came to $923 million; Navan realized $750 million in gross proceeds from the 30 million shares that it put directly on the market. In its last quarterly report, covering fiscal 4Q26, the company had revenues of $178 million, a total that was up 35% year-over-year and beat the forecast by $15.66 million. At the other end of the scale, non-GAAP EPS of $0.02 came in ahead of Street estimates by $0.26. Looking at the insiders, we find that Anre Williams, of Navan’s Board of Directors, recently purchased 100,000 shares for $1.2 million. Williams now holds some $2.6 million worth of Navan’s stock. Goldman analyst Gabriela Borges covers this tech firm, and she starts her analysis of it by looking at its use of AI, writing, “Navan Cognition, the AI layer of the tech stack, is increasingly leveraging internal data and models to provide better, (up to 10x) faster outcomes at a lower cost than a new entrant could by leveraging generic LLMs. Ava, the AI-powered customer service agent, now handles 55% of customer support volume (+1pp q/q) and delivered >80% CSAT during the recent weather-related travel disruptions, allowing Navan to allocate human support resources to more complex cases. Navan Edge, Navan’s new hyper-personalized travel assistant, will allow the company to better serve the large un-managed business travel TAM, much of which is made up of solopreneurs and small SMBs.” Borges goes on to discuss Navan’s prospects and says of the company, “We are especially positive on any features Navan can roll out that make business travel easier, as non-compliance is very common (>50% in some of Navan’s case studies) and converting unmanaged to managed travel is a key way to expand the TAM… We continue to view Navan an under-appreciated software asset with evident technological advantages which are driving business acceleration and a clear path to durable growth at solid unit economics.” The Goldman view on NAVN comes down to a Buy rating, supplemented by a $23 price target that suggests a one-year gain for the stock of 82.5%. (To watch Borges’ track record, click here) Overall, NAVN shares have a Strong Buy consensus rating, backed up by 8 recent analyst reviews that include 7 Buys to 1 Sell. The shares are currently trading for $12.60, and their average target price of $19.86 implies an upside potential of 58% for the one-year horizon. (See NAVN stock forecast) Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment. Disclaimer & DisclosureReport an Issue

Comments

You must be logged in to comment.