yahoo Press

Europe Faces Jet Fuel Price Surge and Supply Shortages

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

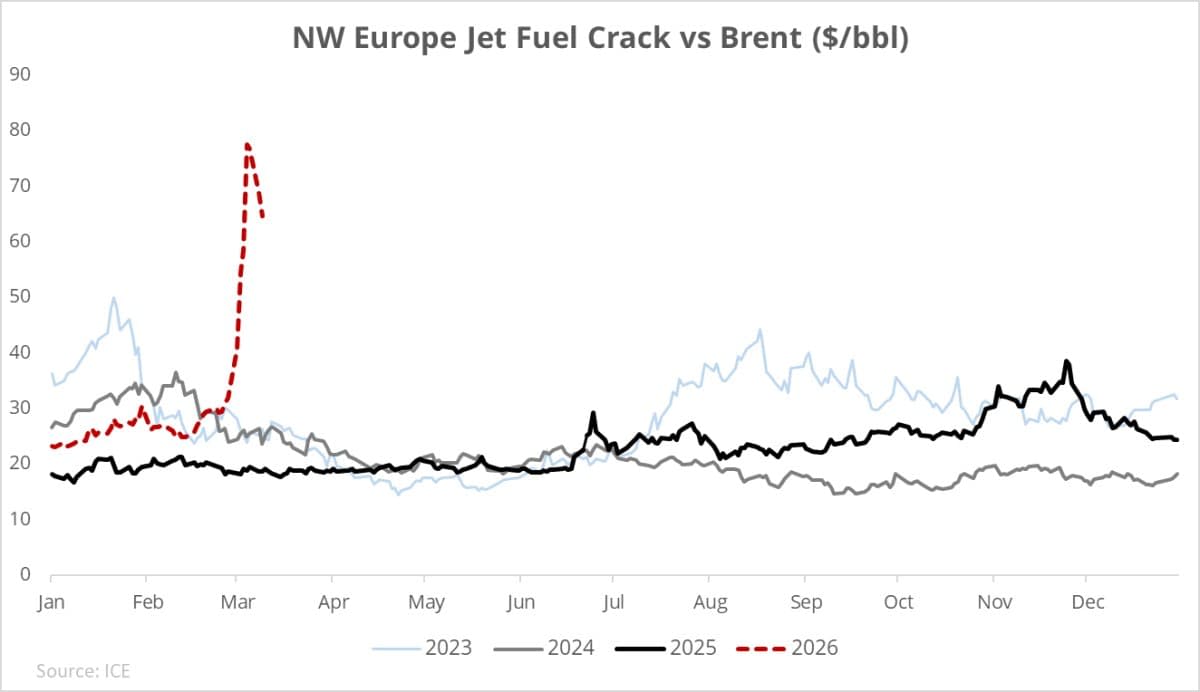

The closure of the Strait of Hormuz since March 1 has triggered an unprecedented distortion in global jet fuel markets, pushing European aviation fuel prices to historic extremes and exposing the continent’s structural dependence on Middle Eastern supply. In a market where diesel has traditionally commanded a premium over jet fuel, the sudden disruption of Gulf exports has inverted long-standing price relationships, leaving Europe desperately searching for alternatives that are either geographically distant, commercially unattractive, or politically constrained. Historically, Europe’s refining system has been structurally tight in middle distillates, reflecting the continent’s diesel-heavy transport system. Diesel, therefore, almost always traded at a premium to jet fuel, with the European jet-diesel regrade typically fluctuating between about –$5 to +$2/bbl during a normal seasonal cycle. That relationship has now collapsed. Since the beginning of the price volatility due to the war in Iran, the regrade has surged to $45-48/bbl, when the ICE jet crack spread has peaked at roughly $78/bbl. While Singapore’s jet crack spread has eventually declined from a shocking last-week peak of $79 to $40/bbl, the European peak is still holding to $65-68/bbl levels, indicating a real structural shortage. The explanation lies primarily in supply disruption. Around 30% of Europe’s jet fuel imports normally arrive from the Gulf region, and with the Strait of Hormuz effectively closed, tankers loaded with aviation fuel remain trapped inside the Gulf. Related: Little-Known US Company Lands Important Pentagon Contract in Rare Earth Race The Gulf has long served as the world’s principal source of jet fuel exports, largely because its crude oil and refinery configuration generate abundant middle distillates. Among those suppliers, Kuwait has emerged as the dominant provider to Europe, at times covering roughly ¼ of European jet imports. In 2026, there were even weeks when European jet imports originated exclusively from Kuwait. Supply had already been temporarily constrained before the conflict escalated: the Al?Zour Refinery (about 610,000 b/d) , Kuwait’s largest, was offline for several months after a fire incident in October 2025.. By mid-February, however, exports from Kuwait had returned to normal volumes and loading activity intensified as tensions between the US/Israel and Iran escalated. Cargoes were increasingly stored in independent terminals in the ARA hub, pushing jet inventories along the Western European coast to roughly 950,000 tonnes (7.5 million barrels) before hostilities began. Kuwait’s presence in Europe extends far beyond cargo trade. Kuwait Petroleum Corporation controls Kuwait Petroleum International, whose Q8 network includes roughly 4,500 retail stations across Italy, Belgium, the Netherlands, Denmark and Sweden, while supplying aviation fuel across much of Western Europe. Kuwait also jointly operates the Milazzo Refinery (around 200,000 b/d) with Eni. Yet the Hormuz closure effectively isolates Kuwait’s export infrastructure inside the Gulf, forcing the country to curb production because crude and refined products cannot be shipped outward. The UAE and Bahrain face similar logistical blockages, as their refining systems are likewise concentrated along the Gulf coast. Related: No Magnets, No Drones: How China Controls the Future of Warfare Among regional Gulf producers, Saudi Arabia is the only major supplier with a partial alternative route via its Red Sea coastline. However, structural bottlenecks limit Riyadh’s ability to redirect volumes westward. Crude would need to move through the East?West Pipeline, whose 5 million b/d capacity represents only about half of Saudi Arabia’s 10-11 million b/d production capability. The Red Sea hub around Yanbu is historically optimized for crude export rather than refined product shipments, while nearby refineries have largely served domestic or intra-regional demand. If Gulf supply is constrained, the theoretical alternatives lie in China, South Korea, the United States, and India – the world’s largest jet fuel exporters outside the Gulf. In practice, each faces significant limitations. China remains geographically distant from Europe, and freight rates have surged since the Hormuz disruption. Transporting jet from Chinese ports to the ARA hub now costs around $8–9/bbl, roughly double the $4–5/bbl seen previously in pre-war times. Chinese exporters also prioritize regional buyers such as Japan, Malaysia and the Philippines, while Australia alone imported roughly 45–50 kb/d of Chinese jet fuel last year. Adding to the constraints, Beijing has imposed an April suspension on most refined-product exports, tightening Asian supply. The measure does not fully prohibit jet fuel shipments (bonded exports for departing aircraft and deliveries to Hong Kong and Macau remain allowed) but it still reduces the availability of export volumes. South Korea, another major exporter, faces little incentive to redirect cargoes to Europe either. The country shipped around 120–130,000 b/d of refined products to California last year, supplying a market with exceptionally tight fuel specifications and strong premiums. Other major buyers – Japan, Australia, New Zealand, China and the Philippines – are located nearby, making long-distance shipments to Europe commercially unattractive. The US offers little relief. Beyond the long freight distance, American refiners prioritize domestic aviation demand and supply much of North and Central America, exporting jet fuel mainly to Mexico, Canada, and Panama – markets structurally dependent on US supply. India also appears to be an unlikely solution. Much of its refinery output is about to be increasingly derived from Russian crude, and the EU’s restrictions on products made from Russian barrels make large-scale imports politically complicated even if they were commercially viable. One possible yet limited supplementary source lies in West Africa. The Dangote Refinery exported occasional jet fuel cargoes to Spain, France and the UK over the past year. The plant completed planned maintenance in January 2026 and could raise output in the coming months. Yet its jet exports averaged only about 70 kb/d last year – far below the volumes required to replace Gulf shipments. For Europe’s aviation sector, the consequences are severe. Fuel normally represents roughly 25 % of an airline ticket price, meaning the current jet crack spreads could translate into ticket costs rising by at least 20% purely through the fuel component. Major carriers such as Lufthansa and Ryanair have hedging programs that may soften the immediate impact, but many smaller airlines face both price spikes and the risk of outright supply shortages. The last comparable shock followed the devastation of hurricanes Katrina and Rita in 2005, when surging jet fuel costs triggered a wave of airline bankruptcies. What makes the current jet fuel crisis in Europe different is that it is not solely about high prices. While market pricing is mostly a psychological game of nerves and expectations, the Hormuz closure raises a fundamental problem of jet fuel’s physical availability. With freight costs surging and most large exporters locked into regional supply chains, Europe faces the prospect of a market where cargoes simply do not arrive. In that context, the shortage of jet fuel (let alone its cost) could become the defining constraint for European aviation in the months ahead. By Natalia Katona for Oilprice.com More Top Reads From Oilprice.com Why $100 Oil Isn’t Going to Spark a New Shale Boom The Chokepoint Economy: What Happens When Everything Breaks at Once Gulf Producers Slash Oil Output by 5 Million Bpd Oilprice Intelligence brings you the signals before they become front-page news. This is the same expert analysis read by veteran traders and political advisors. Get it free, twice a week, and you'll always know why the market is moving before everyone else. You get the geopolitical intelligence, the hidden inventory data, and the market whispers that move billions - and we'll send you $389 in premium energy intelligence, on us, just for subscribing. Join 400,000+ readers today. Get access immediately by clicking here.

Comments

You must be logged in to comment.