yahoo Press

Will the Iran crisis derail the European truck market’s recovery in 2026?

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

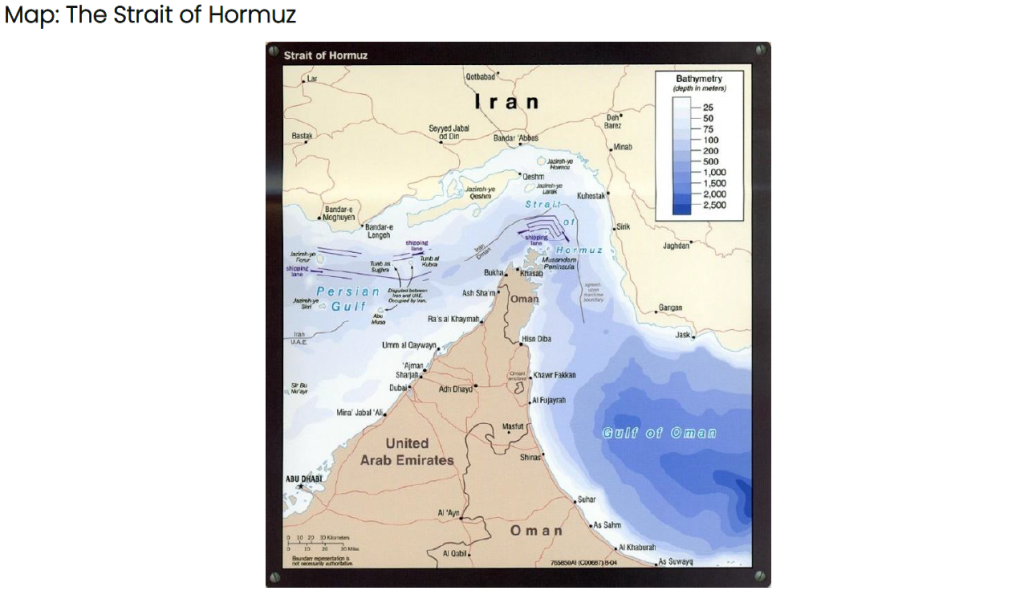

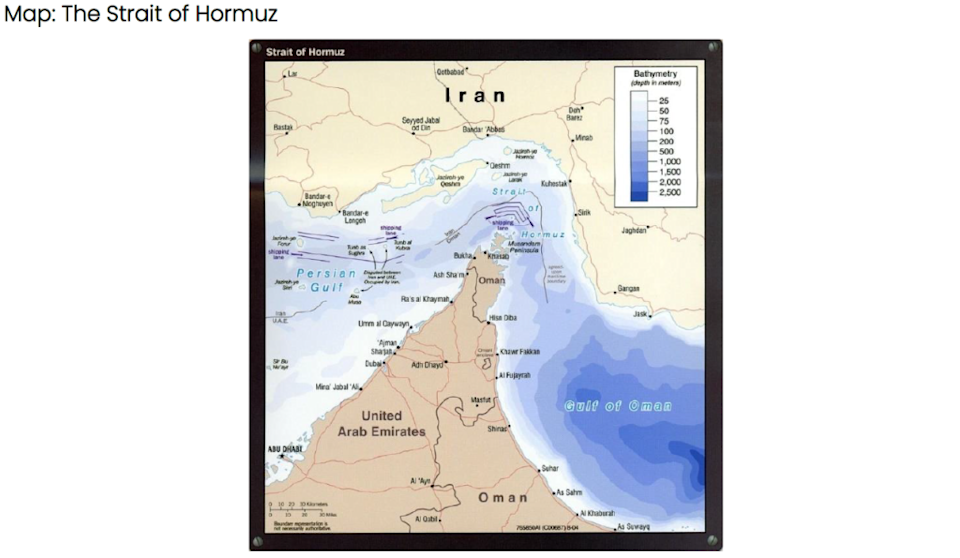

Since Israeli and US missile strikes on Iran began on 28 February, the effective closure of the Strait of Hormuz has jeopardised global oil and gas transport and is resulting in sharply spiking oil prices that are translating into soaring fuel and heating oil prices. More than a quarter of all sea-borne crude oil is transported via the Strait of Hormuz (~20 mn barrels per day in 2025), according to the U.S. Energy Information Administration (EIA). At the time of writing (5 March), the price of Brent Crude has leapt up to USD 83.50 per barrel – compared with USD 60 pb on 1 January (+38%) and USD 73 pb on 27 February (+14%) on the eve of the conflict. To mitigate the escalating crisis, OPEC has announced a production increase to 206,000 bpd from April; however, infrastructure options to bypass the Strait of Hormuz appear to be limited. The combined capacity of Saudi and UAE pipelines is estimated to be less than 10 mn bpd (EIA). In a further move to calm markets, Treasury Secretary Scott Bessent indicated on Wednesday that the United States Navy was set to provide safe passage for oil tankers through the Strait of Hormuz when needed. Quantifying the impact of a potential protracted crisis on regional truck markets is a complex task. A point worth noting is that Asia is the primary destination of oil and LNG transported through the Strait of Hormuz, with China, India, Japan and South Korea being the most exposed to potential supply disruption – concerns about energy security were reflected in stock market turmoil in Asia at the time of writing, whilst European and US stocks appeared to steady after intense volatility at the beginning of the week. A protracted conflict – one lasting several months and materially limiting energy supply – would nonetheless act as a major economic shock beyond Asia, leading to renewed inflationary pressures via the impact on global energy prices, which would drive up inflation both directly, through household bills (reducing disposable income available to spend on goods and services), and indirectly, by raising production costs for businesses (eventually passed on to consumers and contributing further to the inflationary environment). Such a scenario would dampen economic growth and could force central banks to keep interest rates higher for longer than previously expected. At the same time, a sharp increase in fuel prices beyond the short term would also directly increase cost pressures in the road transport industry, which may limit fleets’ ability to invest in equipment if costs cannot be passed on or otherwise absorbed. But, while the overall economic environment might become more uncertain and less supportive of investment in such a scenario, history suggests that a significant negative impact on truck demand is not a given. A look at the relationship between oil price and confidence is helpful in this context. Whilst light vehicle demand tends to respond to consumer confidence, heavy vehicle demand is more highly linked to business confidence – when truckers are optimistic that business will be strong and repay a capital investment, they order equipment. When pessimism prevails, orders drop. For consumers, rising oil prices tend to act like a "tax", reducing disposable income and increasing inflation expectations, which leads to lower sentiment. That means that the correlation between oil prices and consumer confidence is primarily negative, particularly in oil-importing economies. For business confidence, on the other hand, the situation isn’t quite as clear-cut – business sentiment and oil price are not particularly highly correlated, either negatively or positively. Research suggests that, in stable times, there is sometimes a weak negative correlation: a rise in oil prices is seen primarily as an input cost. The effect is often insignificant, though, because businesses may be able to hedge costs or pass them on to consumers. In stable times, factors other than the price of oil tend to be much stronger determinants of business sentiment. During unstable times, on the other hand – periods of high volatility known as “volatility regimes” –, the two variables may actually be positively correlated. For example, in a high volatility regime triggered by a major global crisis (such as the GFC or COVID-19), a sharp drop in oil prices may occur alongside a sharp drop in business confidence. Conversely, a prominent example of a high-volatility period when both oil prices and business confidence rose in tandem was the global commodity boom 2003 - 2007. In these periods, oil prices act as a real-time barometer for global economic health and are read as such by businesses. As a result, the link between truck demand / truck sales and oil prices is tenuous, at best. Recent history suggests that the European truck market is likely to ride out the storm, provided the conflict does not trigger a wide-ranging supply crunch along the lines of the 2021-2022 semiconductor shortage/Ukraine invasion supply disruption, which constrained the EU truck market recovery during those years (albeit not nearly to the same extent as it disrupted the light vehicle market). The oil price hike, in and of itself, left selling rates fairly imperturbed – sales were instead primarily limited by availability of parts and raw materials. Supply of parts and good from Turkey (totalling over USD 100 bn a year) will be of particular significance to European industry. An ongoing conflict would threaten Turkish energy security through potential disruptions to the 13% of natural gas imported from Iran. While a total cut-off poses risks to industrial production, Turkey’s enhanced storage capacity, seasonal demand declines, and increased reliance on renewables for electricity generation mitigate a crisis similar to 2021-2022. Direct oil trade is negligible, but raw material and logistics costs for Turkish manufacturing may be inflated through indirect price contagion (because Turkey's gas agreement with Iran is indexed to Brent Crude, any regional instability that drives up oil prices will simultaneously increase the cost of domestic production in Turkey). While transport of goods out of Turkey will still be possible (as Turkey's primary export routes to Europe and the West do not pass through the Strait of Hormuz), European manufacturers can expect increased lead times due to raw material bottlenecks and price surcharges driven by the volatile energy market. Given the still-evolving nature of the crisis, we have, for now, not significantly reduced our forecast expectations for the year ahead. An escalating crisis, combined with high uncertainty, ongoing market jitters, and – crucially – a dip in business confidence caused by supply disruption and/or a material threat to European energy security, would prompt a downward forecast revision. At present, this is not a core assumption. Zita Zigan, Director, Global Commercial Vehicle Forecasts, GlobalData "Will the Iran crisis derail the European truck market’s recovery in 2026?" was originally created and published by Just Auto, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.

Comments

You must be logged in to comment.